This can’t be true. “I’m not creditworthy.” Have you heard that sentence from your local bank? Especially now, when you urgently need a loan because your car suddenly and without warning stopped working? Or did your daughter excitedly tell you she wants to get married this year? In a fancy venue? Everyone should be there, the whole extended family, to share this wonderfully unique event with her and you. And now?

There you sit at your bank, a loyal customer for years, and sweat breaks out. Once you failed to pay a bill in the past and suddenly a boulder is placed in your path. A Schufa entry that immediately worsened your scoring value. But you really don’t want to disappoint your daughter. You simply can’t manage without a car. And the person opposite you says coolly and curtly: “Unfortunately we can’t help you with that.”

If you’re wondering how a loan without a Schufa entry can help you here, just ask us.

Make your daughter’s dream come true. Do you see her beaming smile? Buy a new car, get your child safely to school. Settle an existing loan with us, restructure your debts. No matter what you use the MAXDA loan without Schufa for, this instant loan does not worsen your existing Schufa rating.

What does a loan without Schufa mean?

You know how it is. Prejudices form quickly and stick stubbornly. “A loan without Schufa only comes from usurers. With high interest rates. From loan sharks. Who only want one thing — your money. No matter what. Keep your hands off it.”

Don’t worry, the world moves on. A loan without Schufa is anything but dubious. On the contrary. We take you as a borrower and your individual situation seriously. We do check carefully whether you can repay the loan. We check quickly and discreetly. We also obtain information about you from Schufa. But not only that. We take a personal approach to you, your circumstances and your conditions.

How now? I thought there were loans without Schufa involvement, you ask? Not quite. “Loan without Schufa” means you receive a loan from us that is not recorded with Schufa. Negative entries in Schufa occur quickly. Have you overdrawn your current account? Missed and not paid a mobile phone bill? Zap. Already happened. These negative entries are, however, deleted after a certain time and your Schufa scoring value recovers. If, for example, you plan to build a house and need a larger loan, Schufa information is usually requested. With a loan without Schufa you therefore relieve your Schufa record.

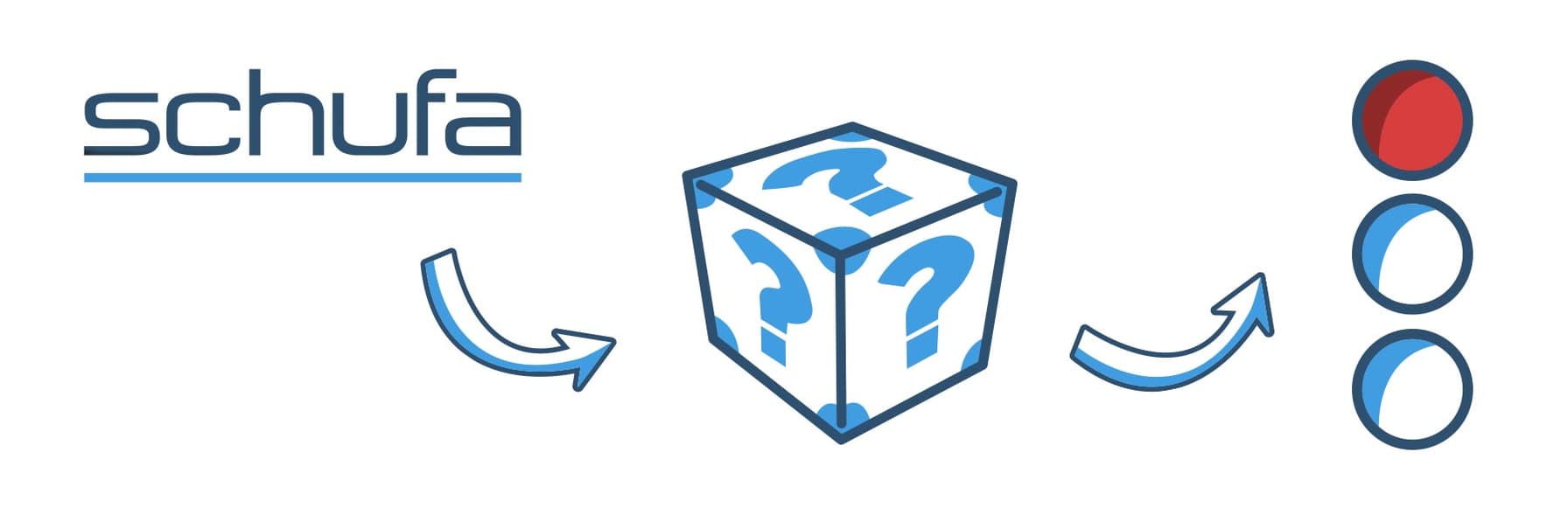

What exactly is the Schufa?

What exactly does Schufa do?

Why does Schufa exist at all? And why is it allowed to collect so much information about me? Do they sell my data? What does Schufa know about me? How long is the information stored there? Don’t we have data protection? A thousand questions buzzing through your head? Do you feel trapped in the (data)net? Like a spider sits there—the Schufa—and suddenly springs in between? Messing up your purchase? Your plans?

Even if it may seem that way, Schufa is not your enemy. It even helps you. You and those who rely on the fact that you can pay something.

Schufa stands for Schutzgemeinschaft für allgemeine Kreditsicherung. This institution is not governmental, as is often assumed. It is a private credit bureau that collects and stores data about private individuals and companies. Data about payment behavior. The collected information is evaluated using a specific system and then passed on to credit institutions when they want to know whether you are able to repay requested loans.

Schufa receives information, for example, when you open an account at a bank. Have you ever ordered something and agreed to installment payments? Bought a mobile phone and concluded a contract? This is also listed in your Schufa entry. As are details from electricity providers, online retailers, telecommunications companies and insurers.

Around 9,000 contractual partners provide data to Schufa. You must always consent to this data transfer and storage in advance. Information is not simply collected and passed on behind your back. Often you can’t avoid signing the consent form, though.

What data does Schufa collect?

Do you feel watched? Do you think you’ve become “transparent” because of a Schufa entry? Does it make you uneasy? Is Schufa omniscient? Don’t worry. Schufa does not know what you do for a living or how much you earn. Or earned. Schufa does not know your religious or political views. Which clubs you belong to is and remains your own business. Whether you are married, separated, divorced, single, a single parent with one child, father of five — that is none of Schufa’s concern.

You probably won’t receive a bouquet of flowers on your birthday, but Schufa knows it. And in addition to your birthplace, your name, your address, it also knows where you used to live.

Contractual partners provide Schufa with information about bank accounts, credit cards, leasing contracts, installment payments, loans and guarantees, accounts and contracts in mail-order and telecommunications. The information in these areas is transmitted automatically. That means, when you open a new current account, Schufa learns about it and records when and where.

Sometimes it happens faster than you think. Separation, divorce, suddenly tight finances. Only personal insolvency helps out of the misery. Such things do not remain secret; on the contrary, they become public. Among the information Schufa automatically receives from its contractual partners, the bureau also collects and processes data from public sources. You therefore also receive a negative Schufa entry if you are listed in a debtor register at the local court or have submitted a sworn statement of assets.

Why does Schufa help me?

Schufa determines your ability to pay from the collected data. Companies that enter into contracts with you, where you pay in installments, want to know how your financial situation is. They query Schufa. By the way, tax authorities, police and enforcement officers also do. Have you always repaid your loans reliably? Paid your electricity bills? Always transferred lease installments on time? Great! Then your score value is top and you are a preferred borrower. Or do you know this situation? Due to a special circumstance like a move or personal problems like a separation, a bill was overlooked? You intended to pay the reminder immediately, but somehow you forgot? That also goes into Schufa’s list and changes your score value. Your “score” is your “game score” at Schufa. This value is passed on by Schufa to companies. It indicates how likely it is that you will repay a loan on time.

What is the score value?

How does the score value work?

It’s quite simple: the higher your score value, the better your creditworthiness. In other words, the easier it is for you to get an instant loan approved. This value is composed of all entries in Schufa as well as general statistical surveys and empirical values. The scoring procedure is intended to enable a reliable forecast of the future based on generally collected past experiences. How exactly the score is calculated, Schufa does not reveal.

That’s good for credit brokers, banks and lenders. They should be protected from the risk that you might not be able to repay the loan in the worst case.

That’s bad for you as a borrower. Because Schufa not only evaluates your personal data, but also factors in general data — industry-specific. It can therefore be that you receive a different score for a loan request to finance a car than for building a house.

Schufa only provides the information, though. It is not the authority that approves or denies your loan. Did you think that? That’s wrong. Based on the Schufa report, banks, lenders and brokers then decide on the amount and disbursement of your loan.

When is an entry made in Schufa?

Have you received a first reminder threatening a Schufa entry?

Debt collection agencies and some mobile phone companies can be quite pushy.

Don’t be unsettled!

If you pay your invoice within the payment period, Schufa does not find out. That also applies if the amount is still outstanding after the first reminder. Have you still not paid after the second written reminder? That leads to an entry — provided there are at least four weeks between the first and second reminder. However, a notification to Schufa may only be made if you were informed about this in one of the two reminders.

Do you believe the invoice is not lawful and have you filed an objection? Good! In that case an entry is not possible.

Beware of statements!

Did you admit that you overlooked the invoice? And assured that you would pay it shortly or by a certain date? Did you agree on installment payments? If you then still don’t pay, Schufa will be notified.

The same applies if your contract was terminated without notice because you could not pay. Again, you must be informed in advance about the consequences. Have you received a court payment order? As soon as the creditor involves a court, that triggers the negative Schufa entry.

What influences your Schufa score value?

There it stands. Your Schufa score value. And you just shake your head? How can it be that the value is much lower than you thought? Do two late payments make that much difference? Don’t worry. Not every small reminder pushes your value down. Have you leased a car? Great. The existence of leasing contracts, loans and current accounts shows that banks trust you. If the bank has terminated your loan or initiated collection proceedings, that is negative for your score.

Sometimes life takes a wrong turn. Know the feeling? Didn’t pay attention, missed a bill and eventually a writ of execution arrives in the mailbox. If these become legally binding, they affect your future creditworthiness as a borrower. Entries in public debtor registers and personal insolvency also reduce the Schufa value. For the scoring calculation, information that initially has nothing to do with your creditworthiness is also used. It seems so. How often have you moved? That negatively affects the calculation. Schufa denies that it matters whether you live in a “good” or “bad” area. In individual cases, if the bureau has no further information about you, this may be checked on request.

You just wanted to get information and made credit inquiries at several institutions? Very bad! Each individual inquiry is stored at Schufa and reduces your score value. Our tip: ask for the credit conditions. These pure information inquiries do not affect your creditworthiness.

By the way: of all Schufa entries described — only about ten percent contain negative information; more than 90% are positive.

How does Schufa help you now?

Schufa keeps an overview for you. It stops you before you slide into over-indebtedness with another loan. Whoever has a lot to pay can sometimes lose clear sight of things. Or overestimate themselves. “I can manage that.” Haven’t you thought that before and then something didn’t work out? For banks and lenders only one thing counts: facts. They calculate whether, based on your income and past payment obligations, you can repay a loan.

Why is there a Schufa inquiry at all?

Why do banks carry out a Schufa inquiry?

Have you ever lent your car to a friend? Admittedly: you were a little relieved when the vehicle was returned to you intact, without scratches or dents. Right? Banks and lenders feel the same. They want to be sure the lent money comes back.

Banks are also legally obligated to check whether you can and will repay a loan. The advantage of lending your car: you know the person you gave it to for a certain time. You know they can drive and often how they drive — calm, relaxed, safe. Banks don’t have this information. They don’t know who you are or how you’ve handled money so far.

Before you sign a contract that requires monthly payments, such as a mobile phone contract or a loan contract, your creditworthiness is checked. Almost always.

A Schufa report is one way to get an impression of your creditworthiness. One way. Don’t worry. Reputable providers will always obtain further information. They also want to know what you regularly earn and receive. As well as how high your expenses are.

Criticism of Schufa?

You applied for an instant loan at your bank and it was rejected? Ask for the reasons. It’s not uncommon to find incorrect Schufa entries. The basis for the bank’s decision to grant you a loan can therefore be wrong. The way Schufa operates is increasingly criticized — not only by consumer protection associations, lawyers and data protection advocates. How exactly an individual score value is composed and determined remains Schufa’s secret. Whether the data Schufa receives about you from contractual partners is correct is not checked. Only when you draw attention to incorrect entries yourself will Schufa inquire and correct them.

How creditworthy am I?

Did you know you can find out once a year for free what Schufa stores about you? This is legally required. Use it! Clarify inconsistencies and have them corrected. Now! Why now? If you want to apply for a loan, time is precious and unnecessarily wasted. Don’t let unnecessary delays give you gray hairs. And use the knowledge of your score value in discussions about the desired loan.

What happens to Schufa entries then?

Can my Schufa entries be deleted?

Made a mistake once and paying for it for the rest of your life. Feeling like that? Don’t worry! It’s not that bad. Your Schufa score value changes continuously. When new data is stored, a new calculation is made. If Schufa’s calculation models no longer deliver reliable forecasts, they are revised. Then Schufa recalculates your value again. When old data is deleted, an adjustment also takes place.

When are entries deleted? Can I influence that? Speed it up? Which data may be stored for how long is regulated by law. Credit inquiries remain on record for one year after the inquiry. Have you repaid your loan? Great! Three years later this entry will be deleted. This also applies to your customer account data at online and mail-order retailers, your data from debtor registers and information if you entered into reminder or collection procedures or did not settle claims. Did you name a guarantor to obtain a loan? Once that loan is repaid, the entry is deleted. Has your current account been closed? Your credit card returned? This information is changed at Schufa immediately.

It should be. Sometimes old entries are overlooked and not deleted. Or information listed there is incorrect. Check your history and data at Schufa. Have your data corrected, deleted or blocked. That possible? you ask? Yes! It is possible. Correct entries, however, cannot be removed before the statutory periods expire.

Why get a loan without Schufa at all?

Know the feeling? Murphy’s Law usually strikes when you least need it. Things tend to break multiple times — often in quick succession. First the washing machine, then the fridge and suddenly the TV shows only a pink screen instead of colorful images. Car repair is much more expensive than expected. And then your daughter wants to get married. Too much at once. Or can you refinance a more expensive loan? Do you want to consolidate?

There are three reasons why a loan without a Schufa entry is necessary:

- You are denied a loan by your local bank due to an already existing negative score value.

- A smaller loan amount should not affect your score value because you plan to apply for another, larger loan in the foreseeable future.

- You are self-employed or work as a freelancer. Even if your creditworthiness is excellent, the local bank often balks when you apply for a loan. The risk that you might suddenly be unable to pay is too great for the bank.

How do I get a loan without Schufa?

“Keep your hands off it!”, “Those are loan sharks”, “They only want your money and won’t help you.” Have friends ever slammed such warnings into your face like a splash of cold water? Yes, be skeptical. Compare different offers. Don’t decide under pressure and at short notice. Even if it’s tight: take your time. Use comparison portals, read reviews and recommendations. That way you can form your own impression of various providers and brokers for a loan without Schufa.

Find out about the respective requirements. If you meet them, in most cases you can submit your loan application online. Nice and relaxed. Are you afraid? “What if I do something wrong? Enter something incorrectly?” Don’t worry.

The process is very simple:

You enter your personal data as the borrower, state the loan amount you need and your desired loan term. Add contact details and your current residence. Then indicate your occupation, where and since when. How high is your monthly income? Lenders and brokers also want information about your partner. Send the information and after a few days the credit broker will contact you. We do that. And we also offer you a free consultation. Together we find the best solution for you. You will then receive the loan application from us by email and by post. Fill it out, sign, add a copy of your latest payslip and send everything back to us. That simple. Once the documents and your information have been checked and the application is approved, we promptly arrange the disbursement and you receive your loan.

Why a loan without Schufa from MAXDA?

Which loan without Schufa is reputable?

We want you to feel secure. That only works if we are also secure. We won’t promise you the moon or astonishingly low interest rates. We do not hide our costs.

• Yes, we charge a brokerage fee. It applies when you conclude a contract with us. Only then!

• Are you asked to pay something upfront to even receive an offer? Walk away. If the provider also wants to charge you cash-on-delivery postage for sending documents, that’s a clear sign of an unscrupulous offer.

• Excessive hotline charges for telephone advice? Our hotline can be reached via a standard local area telephone number.

• “Wow! Only 2% interest. This is exactly what I was looking for.” Be careful with very cheap interest offers! Admittedly, such offers sound tempting and are exactly what you need right now. Often the seemingly cheap instant loan offer turns out to be an expensive affair. Dishonest providers like to hide advisory and administration fees behind low interest rates and omit the effective annual rate. Only the latter shows you the total annual cost of the loan in percent.

• You should also be cautious if the opposite is true: very high interest rates are a sign that the provider wants to protect itself against your potential inability to pay.

• Just the loan—pure and simple: with us a loan without Schufa is not necessarily tied to the sale of insurance contracts. If such a product is pushed on you unconditionally in addition, be alert.

Safety first

Don’t be lured by nicely packaged offers and glossy words, especially if you are pressured that the offer is only valid if you decide immediately. In the end you may receive an invoice rather than a loan. And if you don’t pay, a collection agency is quickly involved. Costs skyrocket. So beware of dubious offers.

Be confident: we always present the terms of our MAXDA loan without Schufa openly — transparent and comprehensible.

Loan without Schufa from MAXDA

“You can certainly get a loan without Schufa from us. You will understand that we charge you higher interest because we take on a higher risk.” Did you receive such an offer? Hands off! Even with a loan, interest rates fall within a certain range similar to loans with a Schufa entry. We mediate an instant loan with the lowest possible interest rates adjusted for you. This interest rate does not change during the term. MAXDA loans are available from an effective annual interest rate of 3.99%. The individual interest rate depends on our assessment of how solvent and willing to pay you are.

Do you break out in a sweat thinking about how long it takes to get a loan approved? Your car has a transmission failure, nothing works and you need a new vehicle as quickly as possible? Now? Immediately? Because you live in the countryside and your child has to attend a distant school? Because you have to drive your mother-in-law, who has trouble walking, to the doctor every day? Don’t wait long; we will help you quickly. You will find out just a few days after the check whether the requested loan can be approved. And if it’s really urgent — contact us! We will find a solution.

Your satisfaction is our capital. Being tied to oppressive interest agreements and payments until the end of the term? Not with us. You are not stuck with fixed interest and payments. Variable special repayments are, of course, possible without fees. Are you on sick leave longer than expected and temporarily receiving less money? Talk to us. Together we will find a way; temporary suspension of instalment payments is also conceivable.

Can I also get a loan without Schufa?

What requirements must I meet for a loan without Schufa?

Anyone who wants to apply for a loan must be of legal age. That is a basic requirement for borrowers. As a rule, you should also live in Germany, i.e. be registered here with your primary residence. Do you have a current account? Great. Next requirement met. The current account is necessary so we can transfer the loan amount to you if the loan is approved. Your repayment instalments are also debited from this account. These are the general prerequisites for a loan. Some providers or brokers also want to be sure that you are generally healthy and can fully repay your instalments. Sometimes proof that you are not seriously ill is therefore required.

Have you been employed, a worker or civil servant for at least one year? Is your regular monthly income at least €1,520? Are you between 30 and 65 years old? Then you meet the additional requirements to apply for a loan without Schufa at MAXDA. If you earn less or are younger than 30 or older than 65, a loan without Schufa is conceivable if someone can act as a guarantor. We examine each application individually and find a solution with you.

You trust us, we trust you. Nevertheless, we are obliged to check your information. Incorrect information will not get you to your goal.

What documents do I need?

To apply for a loan without Schufa, you don’t need much. Make a copy of your latest payslip. It must be legible. Attach this to your loan request.

It is sensible to have a breakdown of your monthly fixed costs ready. So think ahead and list what you spend monthly on rent, electricity, gas, insurance and other payment obligations such as maintenance payments. However, this is not always required.

How does a loan without Schufa work?

Where does the money come from?

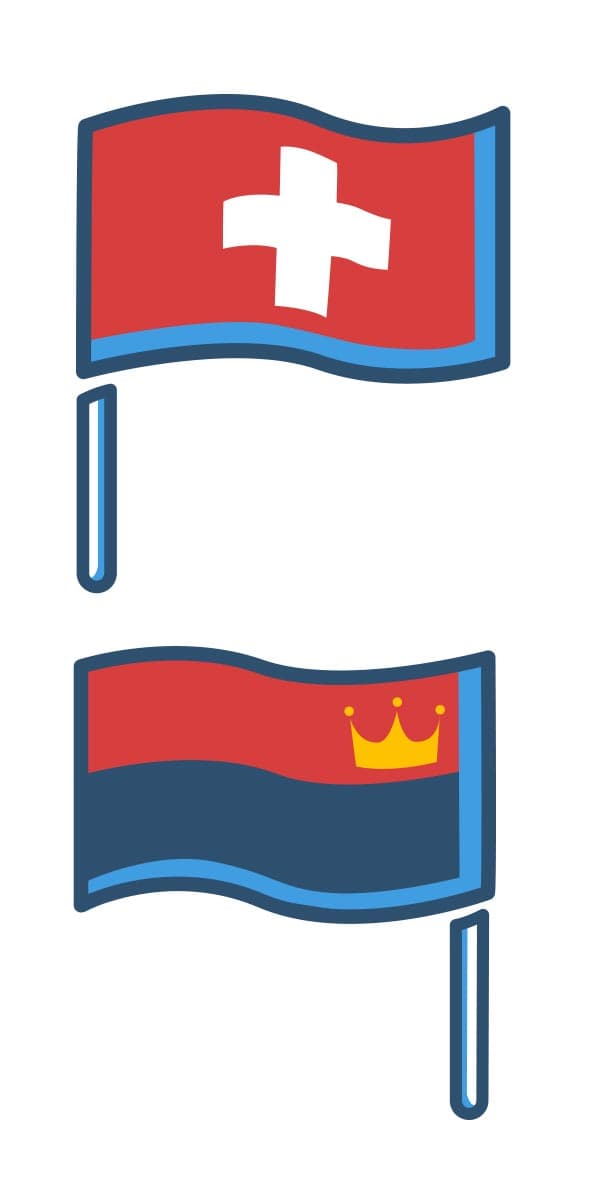

We are open and honest about this: from abroad. As a rule. The loan without Schufa is also known as a “Swiss loan.” In Switzerland there is no institution like Schufa. German banks do not grant loans without taking into account information from Schufa and other credit bureaus. For your loan without Schufa we work with foreign banks. These are usually located in Switzerland and Liechtenstein. Even if they waive inspection of the Schufa file, they still check your creditworthiness.

How much credit can I get without Schufa?

We also protect ourselves and limit our risk. We check your conditions and rely on you to pay the instalments on time until the agreed loan term expires. Sometimes life plays a trick. Imagine this: your company suddenly goes bankrupt. You lose your job. Or you fall ill. Not severely, but your doctor suspects a long-term issue. You then fall out of work and regular payments have to be suspended. Yes, these are worst-case scenarios and we certainly don’t wish them on you. We must, however, take them into account. Therefore we limit the amount for our loan without Schufa to a maximum of €7,500. In return we also waive certain securities. You do not have to assign a life insurance policy to the lender or deposit a vehicle title. What you use the money for is entirely your business. You receive the agreed loan amount from us. We don’t want to know what it’s intended for.

How is repayment handled?

How do you want to pay? Usually we agree on a monthly amount that is debited from your account. This remains the same for the agreed repayment period. How long? You propose a term; we check whether it fits the loan amount and your repayment capacity. The instalment amount consists of the repayment portion and the interest due.

Did you inherit money and want to repay your loan immediately? Right away? No problem! Special repayments are, of course, possible. The same applies to early repayment. Just talk to us.

When will I receive the loan approval?

You need the loan quickly. We process your request promptly. We promise to review your documents immediately. If these are complete, legible and the online form has been filled in correctly, we usually need 2–4 days to review your loan request. We send you the offer before we forward your loan application to the lender. The quicker you review it and send it back to us, the faster the disbursement and the sooner you receive your money.

How do I apply for a loan without Schufa?

How do you get the MAXDA loan without Schufa? Simply click the online form, fill it out and submit it to us with one click. We then check with our domestic and foreign banking partners which is the most favorable offer for you as a borrower. Next step? We send you this offer and you check whether it suits you.