Some want to build a house, others want to buy a new car. Some need a new washing machine, a new stove or a new dryer. Often everything is needed at once. Then Murphy's Law has struck again: everything that can go wrong, goes wrong. Short-term money is needed. If that money is available, everything is fine. If not, the overdraft helps. It is colloquially also called a "Dispokredit" or even shorter a "Dispo".

When a bank grants an overdraft facility for a current account (Girokonto), the account holder can have access to more money than is actually in the account at the moment. It is therefore a way to "overdraw" the account. The bank account goes into the "negative". The credit institution charges interest for this loan.

Banks introduced this form of credit in 1968. Since then it has enabled both business customers and private customers to bridge short-term financial bottlenecks. This form of loan is the most used of all possible credit types. Millions of account holders use an overdraft daily. Why is that?

Above all, because it is easy to get an overdraft approved. Usually every newly opened current account comes with the option to overdraw. The bank grants the customer this possibility when the account is opened, provided that regular payments are made into the account. The maximum credit line is generally based on the account holder's income. It is thus set initially. Afterwards, every account holder can access this amount at any time. It is at the customer's disposal — hence the name of the credit.

It is not necessary to use the entire credit amount each time. Partial amounts are also possible. Any amount within the established financial margin can be used. The money can also be repaid whenever it suits. An overdraft is therefore also possible for a longer period, although not advisable. Why is that discouraged? The overdraft interest rates that a credit institution charges for the overdraft are the most expensive interest rates in consumer lending.

This is explained by the fact that the bank may have to borrow money on the capital market at short notice. It does not know in advance when the overdraft will be used. Short-term money procurement incurs higher interest than long-term, planned transactions. The credit institutions pass these costs on to customers via debit interest. These interest charges apply for every day the account is in the negative. They are calculated on a daily basis. A bank customer therefore pays interest for the overdraft only for the period in which the overdraft is used - and not a day longer.

Nowadays almost every current account, including online checking accounts, comes with this small credit when the account is opened. Banks often bundle packages that include the overdraft as a component. If a person is of legal age, has a regular income and can show a positive Schufa assessment, this credit option will be set up quickly. After the first incoming payments to a current account, the overdraft limit is determined.

Should the credit limit be changed at a later date? Banks usually allow that informally, quickly and easily. The overdraft limit can be increased or of course decreased afterwards. So if someone definitely does not want to overdraw their account, they can inform the bank accordingly.

At most credit institutions the arrangement of an overdraft is done automatically by the bank. No active request is necessary. The account holder receives a "unilateral declaration of intent" from their bank, in which the credit line is granted and the amount fixed. This is usually sent by post. Sometimes this declaration is also included as additional information on account statements. If an offer to use an overdraft is not provided, that is usually not a problem. Then the customer must be proactive. Anyone who wants an overdraft for their current account contacts their bank directly and personally to agree the conditions.

The height of the overdraft limit is based on the level of income. More precisely: on the net salary that is deposited into the account each month. Most banks offer two to three times this amount as the maximum credit line. Only when money has been regularly deposited into the account over a longer period does a credit institution consider the customer creditworthy. It trusts that the loan will be repaid within a certain time frame, even if that period is not fixed.

An advantage of the overdraft is that it only needs to be set up once and not requested again each time it is used, even after the used amount has been repaid. Whoever uses the overdraft does not have to apply for it anew each time. It is always possible to withdraw more money than is actually available in the account, of course only within the previously set limit. Those who overdraw beyond this limit must expect very, very high debit interest. It is therefore advisable to stay within the overdraft limit. If the amount is still not sufficient, other loan types are cheaper. If the current account has been overdrawn, it should be balanced as quickly as possible. Usually this happens with incoming salary payments. Of course, additional cash deposits or transfers from a savings account to the current account can also cover the negative balance.

What determines the overdraft amount?

How much can it be? In general, everything is negotiable. How far should the account be allowed to be overdrawn? Banks rely on their own experience. What amount can someone with a regular income repay? When will it become tight and the account holder fall into excessive debt? Credit institutions are able to make such assessments. A common value has therefore been established to determine the amount of an overdraft. This guideline is two to three times the monthly income. Those who also own securities or a savings account have a chance of getting a higher overdraft. This credit line can also be increased if, for example, a house can be used as collateral. The amount of the overdraft limit is always an individual agreement between the bank and the account holder.

Requirements for an overdraft

Who can get an overdraft?

As with other types of credit, being of legal age is the basic requirement for being granted an overdraft. Anyone who is 18 years or older can use the overdraft, provided they hold a current account and regular payments are made into it. These can be wages, salary, pension or maintenance payments, but also income from self-employment. The account holder should not have negative entries with Schufa. Negative Schufa entries and a poor Schufa score reduce the chances of this overdraft facility.

Those in vocational training or still studying receive a loan from few banks. It becomes easier with a guarantor. Even easier is the overdraft. Nevertheless, the requirement that regular deposits are made into the current account still applies. For students this can be BAföG or income from a student job. For trainees it is the relevant training allowance. In both cases: no negative Schufa score. No further collateral is necessary to obtain the overdraft. However, many credit institutions stipulate that they can seize assets if the short-term overdraft loan is not repaid. In this case the bank can access the current account or a savings account that may exist. If securities are owned, these can also be used as collateral.

Requirements for setting up an overdraft at a glance:

The borrower ...

- is at least 18 years old.

- has regular income.

- has no negative Schufa entries.

- is the holder of a current account.

Is an overdraft always granted on a current account?

Is there already an account into which salary payments are made? Then a bank will usually send a "unilateral declaration of intent". This normally happens by post. Sometimes the letter is also issued as an additional account statement. With this letter a fixed overdraft limit is granted. The bank simply sets it at twice to three times the monthly incoming income. This declaration is legally an offer by the credit institution. If the overdraft is used for the first time, the offer is considered accepted.

If the bank does not send this declaration, the account holder must contact the credit institution themselves to obtain an overdraft limit. The same applies if the overdraft is to be increased. Then the corresponding conditions are agreed. The credit institution considers whether money is regularly deposited into the account and takes the customer's current payment behavior into account when making the decision. If the overdraft is not approved, the current account must be operated with a positive balance. An overdraft is then not possible.

Is an overdraft possible without fixed income?

Finally 18 — now you can move out of your parents' home, even without a permanent job. First check what you like and where you want to go. But you still want to furnish your own apartment. A new sofa, a small kitchen and of course a modern TV. Wouldn't it be great to use the overdraft for that? Yes, it would. But unfortunately in most cases that is not possible. Without regular income or regular deposits to the current account, a financial institution will rarely grant an overdraft. Sometimes you can rely on the bank's goodwill and ask whether this credit line can be granted without regular income.

Unemployed or undergoing insolvency proceedings? In such cases the chances of getting an overdraft are also poor. Everything is always a matter of agreement with the individual bank. However, banks will not take on uncertain situations. In fact, unemployment or insolvency is a sign of lack of creditworthiness. Banks assume that these people cannot repay the loan. Unemployment benefits are not sufficient for lenders. It is unlikely that a loan can be approved in the foreseeable future on this basis. Those who become unemployed or have to file for insolvency must even expect that existing overdrafts may be terminated by the bank.

Interest on an overdraft

How high is the interest on an overdraft?

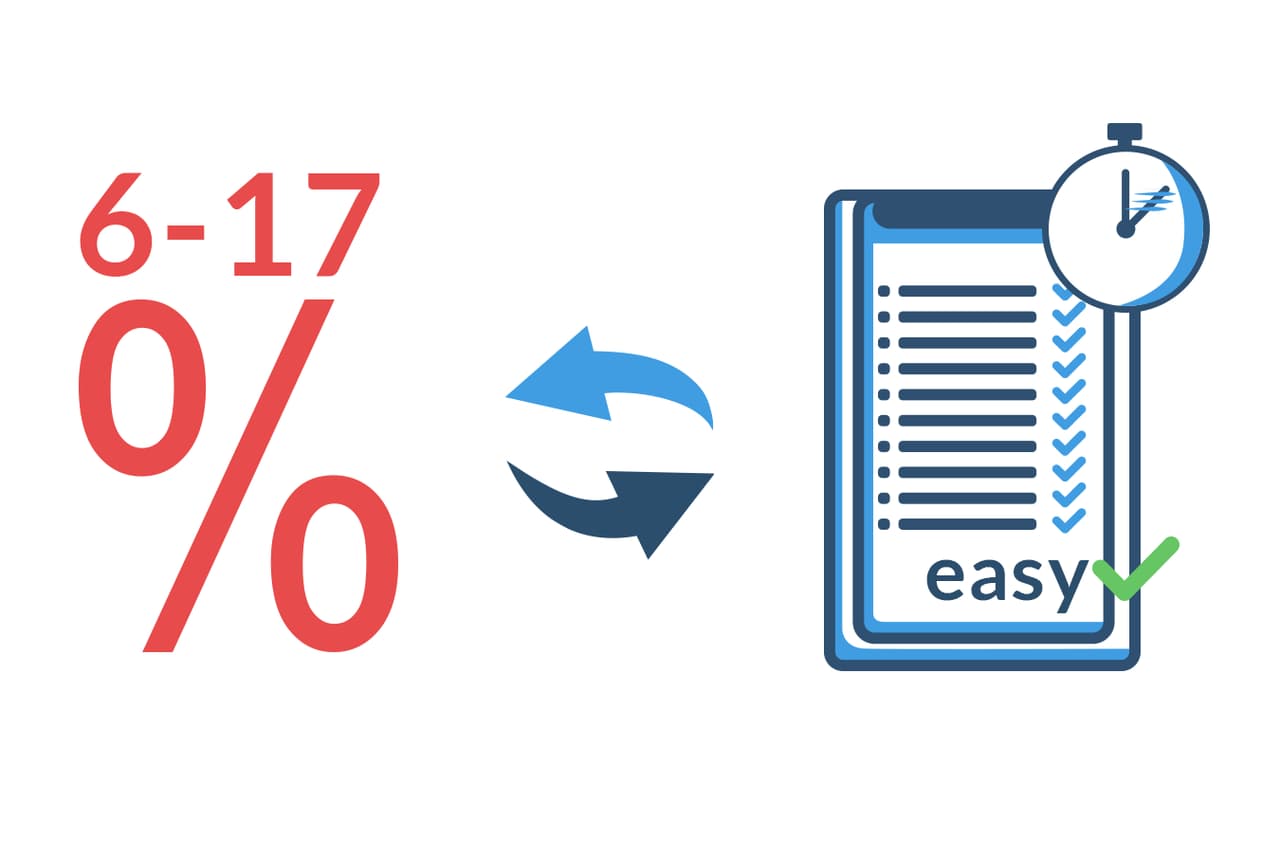

Even if you do not sign a separate contract with a bank: if you overdraw your account, you must pay debit interest. The overdraft is the most expensive option when you want to borrow money. On average savings banks, cooperative banks (Volks- and Raiffeisenbanken) charge 11% debit interest. The actual range is between 6 and 17 percent.

By comparison: on average a borrower pays 4–5% interest for a consumer installment loan. Depending on the credit institution these rates can start below 2%. The highest rate is at most 12%. Online banks score here with particularly favorable conditions.

Is the granted overdraft not sufficient? Those who exceed the credit line are charged heavily. The loan interest in that case is about 5% higher than the already expensive debit interest. Unlike with an installment loan, these are calculated to the exact day. That means interest is charged only for the days the account is "in the red".

How is the interest for the overdraft calculated?

Banks use the following formula here:

interest to be paid = (amount of the loan * interest rate * number of days): (365*100)

For example: the current account is overdrawn by 200 euros. It is 12 days in the negative until the next income brings the account back into the positive. The credit institution charges an interest rate of 12%. The resulting amount is as follows.

interest to be paid = (200*1212): (365100) = 0.79 euros

Banks calculate interest daily. Because of course incoming payments can also balance the account again. The negative amount decreases. Or it becomes larger if more money is taken from the account again than is currently available. Banks therefore calculate the interest incurred daily and automatically total it at the end of a month for that month. They usually invoice these debit interest charges for the overdraft to their customers once per quarter.

Good to know: if a credit institution increases the interest on the current overdraft, the account holder can terminate it within six weeks. There is a special right of termination for this. The higher interest will then not be charged. If the credit has been used and the account is currently overdrawn, that amount must be repaid with the termination.

Are overdraft interest rates the same at every bank?

Comparisons always pay off. Also with overdrafts. You can save a lot of money here. Who does not know it: at the beginning of the month many bills are debited very quickly? At the same time it always takes a little longer for incoming money to be posted to the current account. You quickly slip into the red. It's good to pay the lowest debit interest during these unavoidable times. Are overdraft interest rates the same at all banks? No. There is a wide range of debit interest rates. Online lenders and direct banks usually offer their customers cheaper rates than regional banks. How can this difference be explained?

Savings banks, cooperative banks and other local credit institutions have higher operating costs. Direct banks and online banks usually employ fewer people than regional institutions. Local branches are often available to customers to conduct their banking business and receive advice. The costs for maintaining and staffing these branches are indirectly passed on to customers — also through higher interest rates. Internet banks such as ING-Diba or Comdirect usually advise via chat, telephone or email. The costs for branches are eliminated. Personnel costs are therefore lower. Internet banks thus have a larger margin, which they pass on to customers in the form of more favorable overdraft interest rates.

Both — direct banks and regional banks — must obtain short-term funds on the capital market when a customer suddenly massively overdraws their current account. The credit institution never knows exactly when the overdraft will be used. Banks also pay interest for this short-term financing. It is higher than for planned banking transactions. The credit institutions pass these costs on to customers via the debit interest.

How can I find out how high a bank's overdraft interest rate is?

Everyone must know which debit interest rate they will face if they overdraw their account. Legislation has now made this mandatory. Since March 2016 credit institutions are legally required to clearly state the level of their overdraft interest rates. These must be explained on the banks' websites in a clear and understandable way so that everyone can trace what costs will arise if they use an overdraft. Sounds good. Nevertheless some banks still obscure the concrete costs. Some credit institutions give a reference interest rate and show fees and surcharges, but do not state the debit interest amount concretely. Some determine the interest rate based on the customer's ability to pay and make it dependent on that.

Planning to change banks? Or opening a new current account? Then you should compare in detail and not only look at the overdraft interest rate. Sometimes a bank charges higher interest but then levies high fees. What does issuance and use of the debit card or an additional credit card cost? Are there costs for account management? What are these costs? Can you withdraw cash at ATMs without additional fees? Or at a bank counter? Are there credit interest rates? All of this should be considered when choosing a bank and a current account before switching. If you only want to change bank because of high overdraft interest, you should check whether it might be cheaper to use an installment loan or a line of credit instead of the overdraft.

Termination of the overdraft

Can banks terminate the overdraft?

Banks regulate the termination of an overdraft or tolerated overdraft in their terms and conditions. In most cases the overdraft limit can be reduced or completely removed at any time. If a customer files for insolvency, becomes unemployed or the customer's assets deteriorate significantly, banks can terminate the overdraft immediately — and without notice. If the reasons are significant. Is the borrower threatened with enforcement proceedings? Then termination of the loan is also possible. An ordinary termination takes the notice period into account. This is usually 30 days. If the termination is legally effective, the overdraft already used must be repaid immediately.

Can an overdraft be seized?

An overdraft can be seized if the account holder has made use of the overdraft. That is, for example, if a transfer or cash withdrawal has taken place. It is not the possible amount of the granted credit that can be seized, but only the money that someone actually has at their disposal.

How long does an overdraft remain in place if no income is credited to the account?

If the customer's financial situation worsens, a credit institution can terminate the overdraft at any time. This also applies if no regular income is recorded in the current account. How quickly does termination occur? Whether the account continues to be allowed to overdraw despite lack of deposits depends on the individual bank. Customers who have not been conspicuous so far and have always repaid loans regularly and on time are sometimes granted more leeway than someone who constantly overdraws the already granted overdraft. Sometimes a bank does not get in touch for several months even if no regular incoming payments are recorded. Sometimes it asks after a few days or weeks. Banks are lenient if the missing incoming funds can be justified. Otherwise the overdraft is immediately terminated. Usually you then have four weeks to balance the account. Afterwards it must be operated with a credit balance, i.e. it can no longer be overdrawn.

Repayment of the overdraft

When must an overdraft be repaid? How does repayment of the overdraft work?

Are there fixed monthly installments as you know them from other loans? Is there a set date on which the loan must be paid? What is normal for other types of credit is different for the overdraft. There are no strict conditions for repayment. No repayment installments are agreed with the bank. The account holder determines when they bring their account back from the negative to the positive. When are which amounts paid to settle the overdraft? Usually this happens automatically when the next salary or other deposits are made to the account. Consumer protection organizations warn against exploiting the overdraft for too long. You can quickly fall into a debt trap. You may not be able to get out of the repayments. An overdraft facility can be used year after year without time limit. You should consider that long-term, permanent use is a very expensive loan. Even if base interest rates are particularly low in a year, overdraft interest rates always turn out to be the highest in lending. It is advantageous to repay as quickly as possible because the interest burden then drops quickly and significantly. How high the paid interest rate actually is therefore also depends on your own behavior. For those who repay the overdraft quickly and disciplinedly, an overdraft is not expensive.

Can you overdraw an overdraft?

While payments are fixed in amount and time for other types of loans, an overdraft can be repaid at will. It is therefore possible to use the limit over a longer period. However, overdraft interest rates are expensive. In this case a refinancing — i.e. using another form of credit — should be considered.

Not only is the period flexible, but also the amount of repayments. Because of these wide-ranging options it can easily happen that the overdraft limit is reached. What then happens? At first nothing. It is quite possible to exceed the credit line and not only overdraw the current account but also exceed the overdraft. However, one should avoid exceeding this limit. The interest rates for exceeding the overdraft limit are significantly more expensive than the original debit interest. Often they are five percent and more. In this case it is better to speak with the bank. Even if the credit institution tolerates the overdraft of the credit line, it can refuse or return debits or direct debits at any time if the account is not sufficiently covered.

Talk to the bank advisor

If you reach the limit of the overdraft, you should speak to your bank advisor as soon as possible. This can avoid chargebacks and a lot of trouble. If it is clear that the overdraft is very short-term and sufficient money will be deposited again, you can agree on an overdraft protection loan. Here too the interest rate is higher than for the overdraft. For a fixed period the overdraft is extended once more. It is better, however, to increase the overdraft in principle. Whether this is approved depends on the bank and the customer's ability to pay.

Installment loan as an alternative

Another alternative is refinancing. The debts from the overdraft are essentially converted into an installment loan. They are restructured. Fixed terms and installment amounts are agreed for this installment loan. This has advantages for both bank and borrower: the credit institution can be sure that the debt will be repaid. Its risk decreases. The borrower reduces their debt continuously and at a lower interest rate than the extremely high rate for exceeding the overdraft.

Which banks grant overdrafts?

Whether internet banks, direct banks, private banks or branch banks — nowadays almost all banks offer the option of setting up an overdraft for a current account. This applies at savings banks as well as cooperative banks. Millions of people use an overdraft at Dresdner Bank, Deutsche Bank or Commerzbank. In addition to the larger banks, many of the roughly 2,000 smaller banks in Germany also offer the option of setting up an overdraft limit for a current account. It's worth searching the internet for comparisons. That way you get a lot of information at a glance about the conditions a bank imposes when setting up and enabling an overdraft.

Direct banks and internet banks

Internet banks and direct banks offer particularly favorable conditions for overdrafts. The advantage of online banks is obvious: they employ fewer staff and have lower premises costs because they do without local branches. They pass these savings on to their customers. Often account management for a current account is free and the interest rates charged for using an overdraft are significantly lower than at other credit institutions. The requirements for being granted an overdraft are the same as at branch banks. Creditworthiness must of course be demonstrated. Direct banks also check the Schufa score and require a payslip or other proof of income. All of this is necessary so that the customer can be assessed as creditworthy.

Overdraft from foreign banks

Looking beyond the familiar can be worthwhile. Whether in Switzerland, Liechtenstein or Austria — foreign banks also offer German customers the option of opening a current account alongside branch banks and direct banks from Germany. It is therefore also possible here to obtain an overdraft. In some cases this is possible without requests to Schufa. Within the eurozone it is easy to use a current account with a foreign bank. The account is also kept in euros.

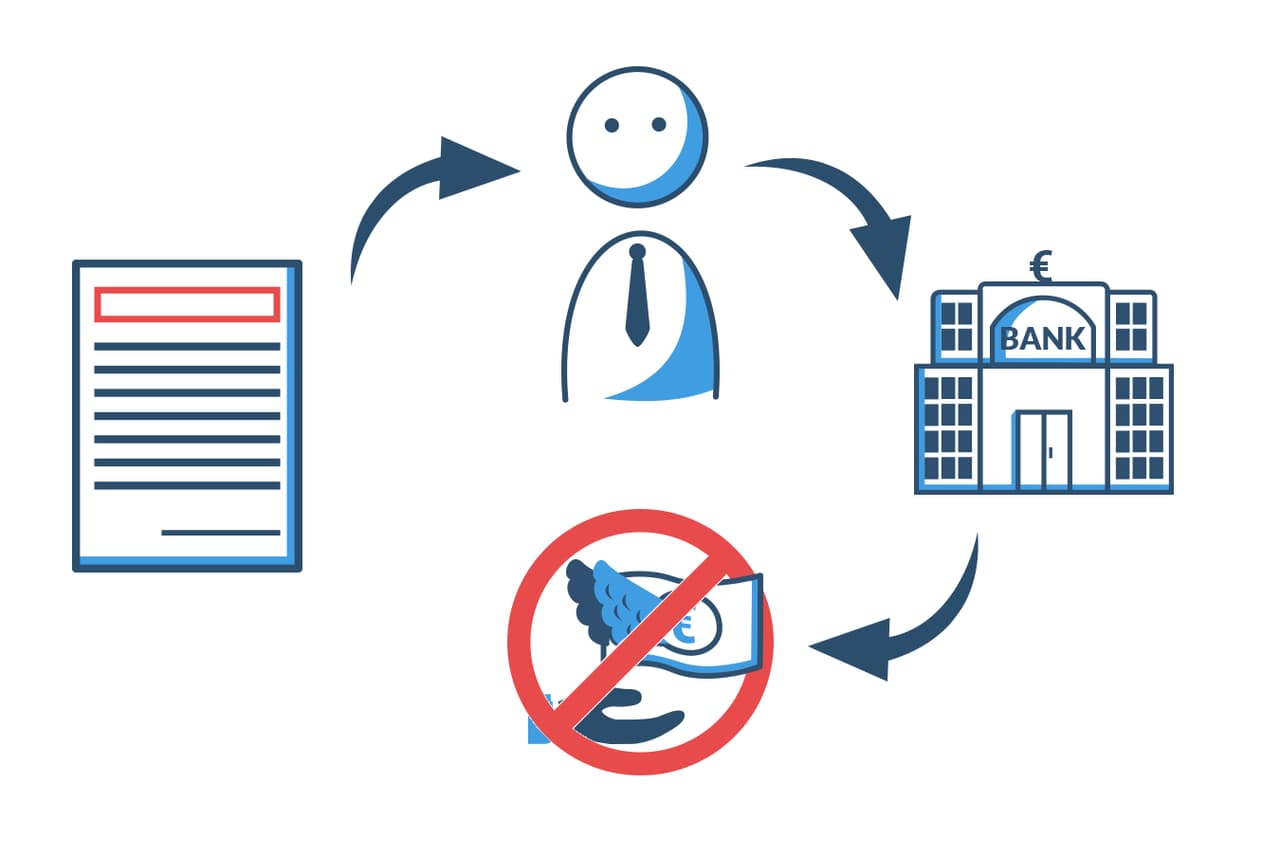

Is an overdraft possible without Schufa?

Who does not know it? A bill and reminder got lost and somehow you failed to pay the due amounts on time. Suddenly you have a negative Schufa entry. To be sure that it will get its money back a credit institution asks Schufa before granting a loan. Is the future account holder or borrower creditworthy? Are they solvent? Can they really pay their bills and interest? Without Schufa information, an overdraft is generally not approved in Germany. But: it is still possible to obtain this flexible credit line even with a negative Schufa score. Credit institutions decide on a case-by-case basis. It is decisive how long the negative Schufa entry has existed. If it will be deleted soon, that is viewed positively. Are there savings or fixed-term deposit accounts? These are considered collateral for the overdraft. Does the applicant have regular salary payments? Is there even an unterminable employment contract? The account holder's current behavior is also considered. Have bills always been paid on time? All of this influences the decision whether the overdraft will be granted despite a negative Schufa entry. In the end it is always the individual decision of the respective bank whether to grant the overdraft despite a negative Schufa score.

Advantages and disadvantages of the overdraft

Advantages of the overdraft

The overdraft is particularly flexible. This loan does not have to be repaid in fixed monthly installments. It is repaid when possible. No fixed term is specified. The amount of repayments is freely determined each time. In most cases the next incoming income will balance the account. It is also conceivable to transfer an amount from a savings account to the current account. That also brings the account back into the black. The overdraft usually does not have to be approved each time, it is immediately available. Interest is only charged for the days the credit was actually used.

Advantages at a glance:

- Interest charged only for the period used

- High flexibility

- Repayment possible at any time

- Repayment in any amount possible

- No special collateral required

Disadvantages of the overdraft

Overdraft interest rates are expensive. That is probably the most significant disadvantage of this credit. This makes it suitable only for short-term financing. Constantly using the credit line over years is costly. If you exploit it extensively, you must expect that the bank will terminate the overdraft — and immediately. Also, the credit line is usually limited to two to three times the monthly net income; more is usually difficult. If you exceed this credit line and overdraw the overdraft, you must pay even higher loan interest.

Disadvantages at a glance:

- High interest rates

- Unsuitable for long-term use (bank can terminate at any time)

- Credit line is limited

Are there alternatives to an overdraft?

Due to the high interest rates, the overdraft should only be used if there is no other option and if it is clear that the negative balance can be balanced again in the very short term. Constant or long-term overdrawing of the current account is not advisable. If short-term bottlenecks have occurred in the current account, you should check whether you can transfer money from other accounts. Is there a savings account or a call money account? Is fixed-term deposit available at short notice? Before taking out the overdraft for larger amounts and for a longer period, you should check whether the account can be supplemented via these alternatives.

Line of credit or call loan

If you need a larger sum over a longer period, it is better to negotiate a line of credit. It is also known as a call loan. It is cheaper than the overdraft, but more expensive than a standard installment loan. With a line of credit you can also borrow money at short notice at any time.

As with the overdraft, an account is opened at a bank for the line of credit. Then the limit is set. For example, it can be agreed with the bank that this limit amounts to 4,000 euros. This credit amount can be drawn as a one-off payment or in several smaller amounts. Here too interest is only charged on the amount actually used. The interest rate on a line of credit is based on a reference rate, for example from the European Central Bank (ECB). If it falls, the loan interest falls. If it rises, the loan interest and personal interest burden rise. Consumers are also flexible with regard to repayment terms for lines of credit. There are no fixed terms and no fixed monthly installments. The customer determines when which amount is repaid. Often, however, a minimum monthly repayment amount is agreed between the bank and borrower. This is between one and two percent of the agreed credit limit.

The line of credit must be applied for from the bank like an installment loan. The bank checks whether the applicant is liquid and reliable. Payslips are usually required. The current account is also given, for example, as the reference account. The amount requested as a call loan is then transferred to the current account.

If you know that you will permanently have to overdraw your account, the call loan is a good alternative because interest is significantly lower. Those who need a loan for a short period, for example less than a year, are also well advised with a line of credit. For a longer period, an installment loan is more appropriate.

Installment loan

Installment loans usually have even lower interest rates than a line of credit. The term is fixed in advance as is the interest rate. However, if you keep your current account overdrawn for longer or even permanently over the years, it is worth restructuring this debt into an installment loan. The pre-agreed installment rate continuously reduces the debt. The longer an installment loan runs, the more expensive it becomes. If you stretch the repayment over a long period, you can expect lower monthly installments. At the same time, very long terms increase the interest. Some banks also charge interest surcharges for terms longer than 60 months. The consumer must therefore expect regular monthly payments for several years. In return, the loan is truly repaid after a fixed period. Balancing the current account for short-term bottlenecks also restores financial leeway. An installment loan can also be reduced by occasional higher payments. However, attention should be paid to agreeing on penalty-free special repayments. Otherwise you will incur additional costs for premature repayment outside the monthly agreed installments. It is advisable to compare the different conditions of various banks before taking out a loan.

Avoiding indebtedness

The cheapest alternative is to avoid a large overdraft of the current account in the first place. Debts often build up when you lose track of your financial situation. It is good then to get an overview. All income and expenses are set against each other. This quickly shows how liquid you are and whether or what financial leeway you have. Bottlenecks will sometimes occur. Who does not know that? If you recognize them, you can consider where to save. Or increase incoming payments to the current account. Those who, for example, build up reserves in a call money account are on the safe side. These help when you unexpectedly find yourself in a very tight financial situation. Sometimes this happens faster than you think. Either technical devices such as TVs, washing machines, dryers or refrigerators all break down at once or you suddenly face considerable medical additional costs because some expenses are not covered by health insurance. If you have then built up reserves, you do not have to overdraw the overdraft.

Overdraft credit and current account credit - what is the difference?

Some call it a current account credit (Kontokorrentkredit), others an overdraft credit. What is what? And how do they differ? These credit forms are very similar. In both cases a specific financial margin is set up for an account. The account holder can overdraw it up to a previously agreed amount, in other words borrow money from the bank. The bank or credit institution charges interest for this. The amount of money the customer borrows by overdrawing is variable each time. The entire credit sum can be used at once or in smaller partial amounts. These are repaid as the account holder wishes. Up to the agreed credit line new sums can always be borrowed.

Up to this point overdraft and current account credit are the same. The difference lies in the use of the loan. Private customers receive an overdraft; it is thus a form of personal credit. An overdraft is usually set up on a current account used as a payroll account.

Current account credits are made available for business accounts. Companies, self-employed persons and enterprises can use them to pay invoices, wages and salaries or other financial obligations before, on the other side, payments from customers are deposited into the account. Banks thoroughly check companies for creditworthiness before granting current account credits. This is not the case with an overdraft.