The acceptance credit

The acceptance credit belongs to the category of special loans and is primarily concluded between a credit institution and its business customers. This credit is a corporate loan and is therefore excluded for private individuals and should not be confused with the concept of the private discount. It is often referred to as a discount credit in economic dictionaries. An acceptance credit exists when a bank accepts a bill of exchange issued by a customer. The acceptance credit is therefore a bill-of-exchange loan where, due to the issued and accepted bill, credit is granted without an actual cash loan. This bill of exchange is also called a "tratte." The acceptance credit is a short-term loan, with a term limited to at most three months. The name of the credit comes from the Latin word "accipere," which means to receive or accept. The acceptance credit is also considered a short-term instant loan without a credit check.

A special form of the acceptance credit in the past was the private discount. The economic lexicon defines a private discount as a bill of exchange bearing an acceptance (bank acceptance) that was discounted by the Privatdiskont-AG. The private discount is a defunct financial concept that was discontinued in 1992.

How an acceptance credit works

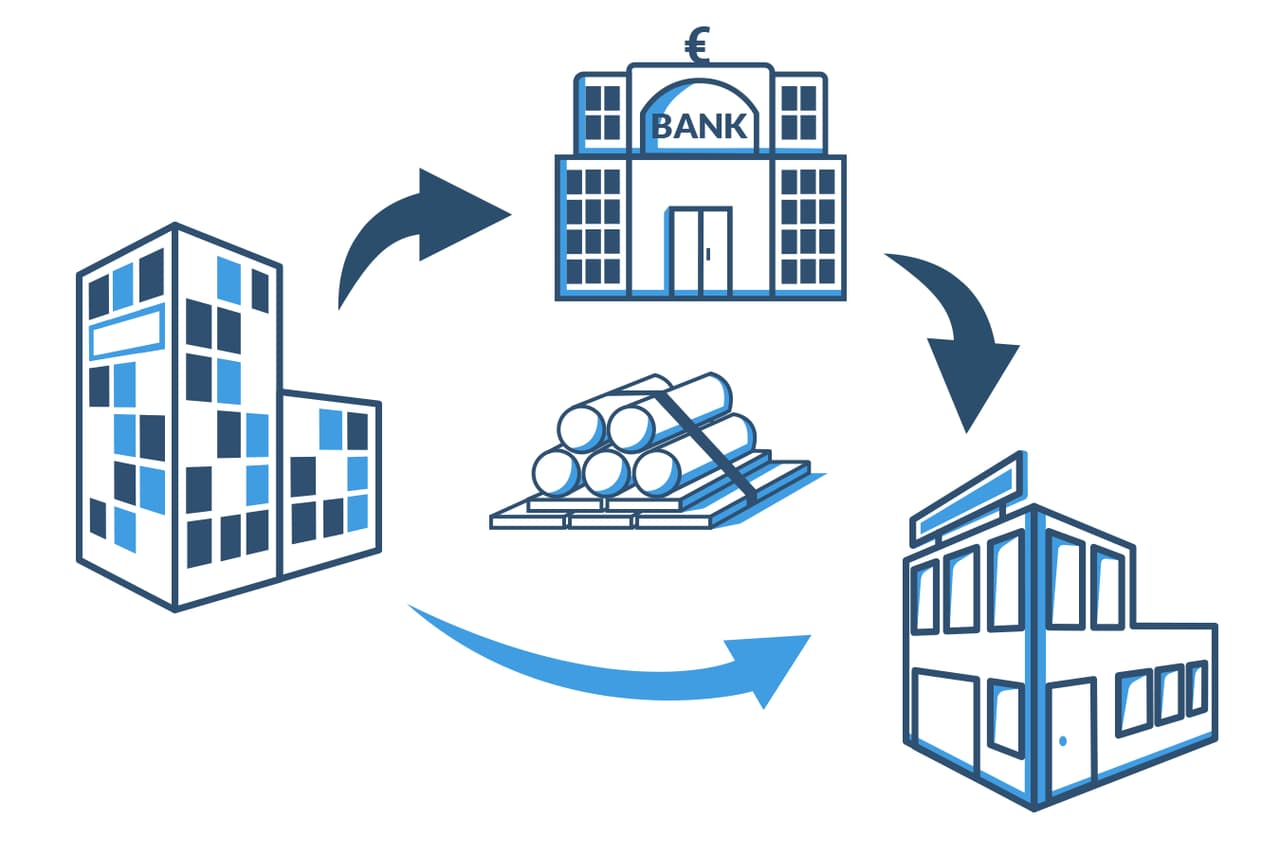

In this loan transaction the bank accepts a bill of exchange from its customer. In this context it is also referred to as a bank acceptance. The bank undertakes to honour the bill on its due date regardless of the customer's solvency and thus assumes full liability under bill-of-exchange law for the payment of the bill. Internally, a claim by the credit institution against the borrower therefore arises. The issuer of the bill, i.e. the original borrower, can have the bank acceptance handed over to them or have it discounted at the accepting bank or another bank. Otherwise, the bank pays the holder of the bill the bill amount on the day of maturity. Although the accepting bank is the principal debtor under bill-of-exchange law, economically the acceptance credit represents only a contingent liability, because the borrower is obliged under the loan agreements to provide the equivalent value of the bank acceptance at the latest on the last business day before maturity. With an acceptance credit, the credit institution transfers its good and proven creditworthiness to the bill. Therefore, the bank’s funds are not actually used in an acceptance credit; instead, the bank simply lends its creditworthiness and good name. In this context one therefore speaks of conferred creditworthiness, since there is no pure cash flow. For this reason, an acceptance credit is not recorded on the balance sheet, as it is shown as a contingent liability. In the event that the bill is not paid on time, the customer's current account is debited. If this is not possible—which is however very unlikely—the bank steps in as the principal debtor towards the creditor. An acceptance credit can be illustrated as follows: A company has the opportunity to procure goods worth EUR 200,000 at short notice. However, it can only sell these goods to its own customer in four weeks. The company therefore draws a bill of exchange for EUR 200,000 at its bank with a term of four weeks. The bank accepts the bill and charges the customer a commission of EUR 1,200 for its services. After the company has to pay the EUR 200,000, it gives the bill to its supplier. After the four weeks have passed, the supplier turns to the bank, which in turn demands the due amount from its corporate customer.

Significance of the acceptance credit

The acceptance credit is of great importance, especially in foreign trade. Foreign partners (companies) often find it difficult to assess the creditworthiness of a German trading partner, but a bank acceptance can significantly improve this assessment. Since the customer is not obliged to pay for the goods immediately, the bill gives the supplier a certain security over the agreed payment period. The payment of the owed amount to the supplier is thus ensured. This is not the case with a conventional loan, since there could be significant payment defaults. A bank acceptance is rated higher than the signature on a bill of an unknown or little-known foreign debtor. In this context, this is also referred to as a rembourse credit. According to economic lexicons, a rembourse credit denotes this special form of the acceptance credit that is based on cross-border trade in goods.

The acceptance credit is usually used for large but short-term goods transactions where the payment period corresponds to the term of the bank acceptance. The bill is then redeemed from the proceeds of the financed goods' sale. For the supplier, the fact that the bank grants the customer an acceptance credit is an important indication that the customer (i.e. the company) is trustworthy, which provides a good basis for a long-term business relationship. But an acceptance credit can be used not only in foreign trade, but also in domestic commercial transactions. The acceptance credit is an effective means of payment for settling liabilities. This is particularly important for suppliers in goods trading. For the recipient of the invoice, an acceptance credit is a favorable credit; for the payee it is a secure and first-class means of payment. The customer can, for example, pass the accepted bill on to one of its creditors to settle its own liabilities. In addition, an acceptance credit is often used as a financial bill to obtain liquid funds. A condition usually imposed by the accepting bank is that the bill be discounted at that bank so that the bank also earns the discount itself. This credit is often cheaper for the customer than another form of credit.

Conditions for an acceptance credit

As a rule, the acceptance credit or discount credit is granted only to first-class customers whose ability to pay is secured. The bank acceptance is an easily marketable credit or means of payment for them. Only companies whose liquidity and payment morale are beyond doubt are accepted. An acceptance credit is handled according to the principles and rules of the Bills of Exchange Act and is legally assessed in this way. Acceptance credits naturally involve costs. These consist of the acceptance commission, processing fees and, if discounted, the discount. The acceptance commission is usually 2–3% p.a. and processing fees around 0.5–0.7%. The discount rate is normally 1–3% and depends on various factors such as the amount of the individual tranche, competitive conditions and the business relationship between the customer and the bank. For the bank, an acceptance credit mainly means additional income through the acceptance commission without using its own funds. In the case of a discount transaction it additionally receives interest income. The advantages of an acceptance credit generally include low financing costs, high flexibility and rapid capital procurement. In addition, no further collateral is necessary. A disadvantage, however, is the strict and swift liability in the event of a payment default.