What is the effective annual interest rate?

The effective annual interest rate is generally also referred to as the effective interest rate. It is an indicator of the total cost of the loan in relation to the loan amount and the entire term. The borrower should be able to determine the costs that arise when taking out the loan and the expected annual burden. Of course, the effective annual interest rate should also make it easier to compare different loan offers. As a rule of thumb: "Effective annual interest rate = total loan costs."

What does the effective annual interest rate consist of?

Interest is the most important evaluation factor when applying for a loan. For this reason, it is very important to be able to compare the total costs with one another. The effective annual interest rate is calculated from the nominal interest rate, processing fees and any other costs that may be incurred.

What is an initial effective annual interest rate?

Sometimes there are offers on the market that refer to an initial effective annual interest rate. This is always the case when the effective annual interest rate can change during the term of the loan. The applications are calculated with the same formula as the effective interest rate. The only difference is that the determination of the interest rate must be observed. If the term is 10 years and the interest rate is fixed for 5 years, this is called the initial effective annual interest rate. After 5 years, negotiations will take place again with the bank.

Calculation of the effective annual interest rate

How is the effective annual interest rate calculated?

The bank employee only needs to enter the relevant basic data into his computer and after a few seconds the effective annual interest rate will be displayed. However, anyone who wants to apply for a loan should not always rely on this. Sometimes it is very helpful to be able to calculate the effective interest rate independently. For easier understanding, we have illustrated the calculation of the effective annual interest rate here with an example.

To be able to calculate the effective interest rate, some information is required. Here is an example:

- Loan amount: 20,000 euros

- Bank processing fees: 200 euros

- Interest rate: 4.95% per year

- Monthly installment: 325 euros

- Payment method: monthly

- Total term: 6 years

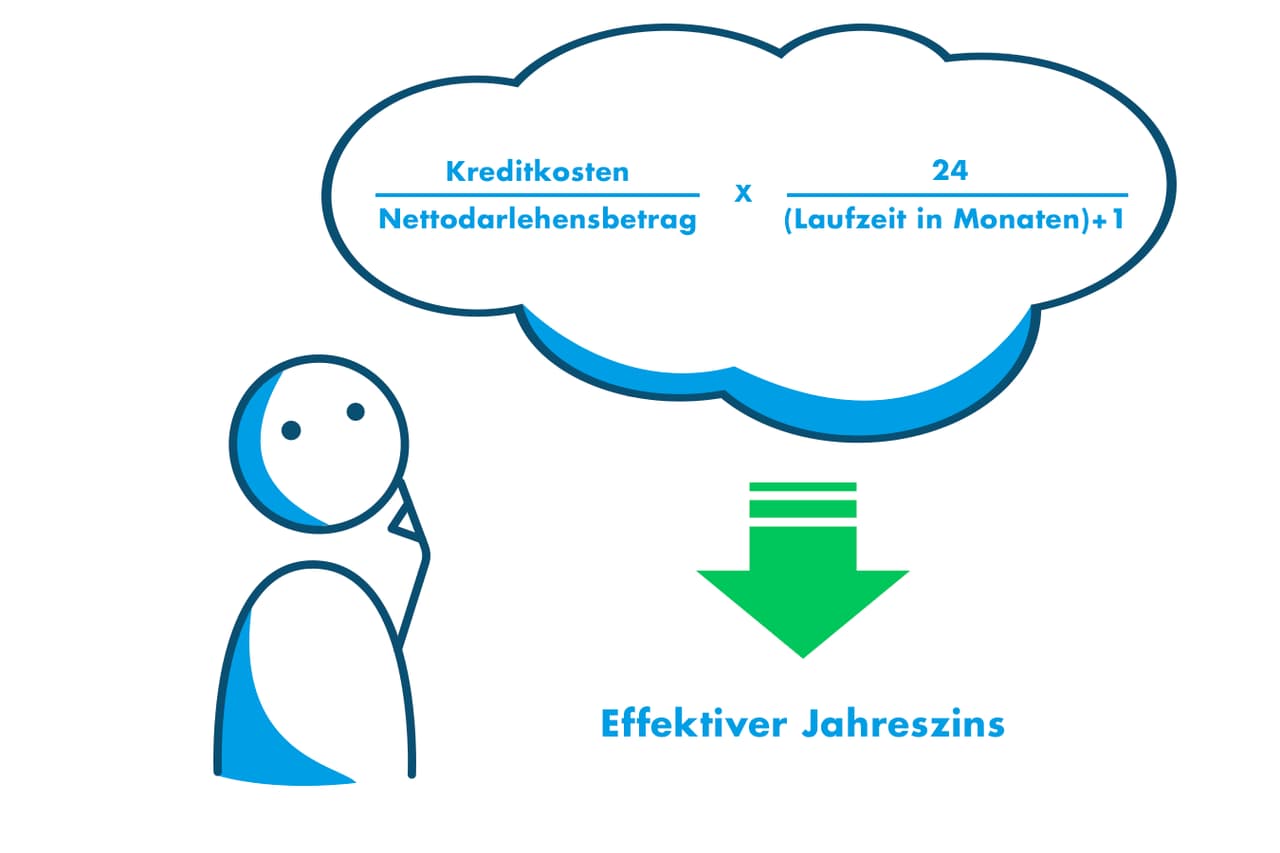

If we now look at the calculation of the effective annual interest rate, we come across the following formula:

Effective annual interest rate = (loan costs / net loan amount) x [24 / (term in months + 1)]

From our example calculation, this would result in an effective annual interest rate of 5.43%.

To clarify the individual elements of the formula, we have explained the terms again below:

Loan costs: The loan costs are the portion that the borrower has to repay in addition to the actual borrowed money. They can be calculated by subtracting the disbursed amount from the total repayment. Alternatively, the loan costs can also be calculated by multiplying the installment amount by the number of months in the term and then subtracting the disbursed amount. The loan costs include the processing fee, the interest and - if desired - also the residual debt insurance.

Net loan amount: The net loan amount is the sum that remains when the total loan amount is reduced by the loan costs.

Term in months: This refers to the term of the loan. For 6 years, the term is 72 months.

How high is the effective annual interest rate?

Even though this is the most important question before calculating a loan, it cannot be answered in general terms. As already mentioned above, the effective annual interest rate depends on numerous factors that vary for each borrower. Both the processing fees and the interest rate and any insurance taken out contribute to the amount of the effective annual interest rate. To get a good overview of the expected costs in advance, it is advisable to compare with a professional comparison calculator or to speak with an independent financial advisor.

Applications of the effective annual interest rate

The effective interest rate of the loan is used whenever the total costs of a loan should be apparent at first glance. Banks repeatedly create offers with particularly favorable loan conditions. However, these are not accessible to every borrower because there are restrictions imposed by the bank and regarding creditworthiness.

The banks' attractive offers are in most cases intended only for customers who can present a flawless Schufa report. Here the risk for the lending bank is particularly low and therefore favorable interest rates can be offered.

If creditworthiness is not very good, the borrower must expect additional costs to compensate the bank's risk. If creditworthiness is too poor, a loan will, in most cases, even be refused. The effective annual interest rate is therefore an effective marketing instrument when it comes to acquiring new customers for a bank and makes a transparent comparison of different loans possible.

Overview of the different interest rates in finance

Nominal interest rate, effective interest rate and nominal rate: What do they mean? What are the differences?

Consumers are sometimes overwhelmed when they have to distinguish the different terms used in finance. Many terms are very similar, such as:

- interest rate

- interest

- debit interest

- annual interest

- effective interest

- effective annual interest rate

- nominal interest rate

and many more. In principle, it is not that difficult to remember the individual terms. For easier understanding, we have explained the terms individually here:

Annual interest rate: Annual interest rates indicate how much interest the borrower has to pay per year when taking out a loan from a bank. If the customer knows the annual interest rate of different offers, this can be a factor for comparison. Nevertheless, of course, the other costs of the loan also belong to the comparison.

Interest rate / interest: This is the percentage indication of the pure cost of the loan. In order for the bank to lend 100,000 euros, the borrowers must repay the money with interest, which is calculated using the interest rate.

Nominal interest rate: This is simply another term for the interest rate.

Effective interest / effective annual interest rate: This figure helps to compare different loan offers. The effective interest rate indicates the total cost of a loan. This also includes the bank's processing fees and any insurance.

What is the difference between the debit interest rate and the effective annual interest rate?

The debit interest rate is an indicator of the expected costs that can arise with an installment loan. For example, if a borrower borrows 10,000 euros at an interest rate of 5% and repays the amount after one year, he must reimburse the bank 10,500 euros. However, these are only the interest charges. To determine the total cost of the loan, other items such as processing fees and additional insurances must also be included.

This task is handled by the effective annual interest rate. As mentioned above, it includes all costs in the calculation and can therefore be used as a comparison factor for different loan offers. The debit interest rate alone cannot reveal the total costs of a loan if other fees have not also been taken into account.

What are the differences between the nominal interest rate and the effective annual interest rate?

Since the nominal interest rate only represents the bank's pure compensation for granting the loan and is also merely a synonym for the interest rate or the debit interest rate, the differences to the effective annual interest rate can be explained in a few words.

Anyone who has already taken out several installment loans knows the procedure. The first question is always about the interest. The bank employee then quotes a number like 4.5 percent. The borrower can use this to calculate how much interest he will have to pay for the entire term. Unfortunately, the important indicators for additional bank fees and residual debt insurances that may have been taken out are missing here.

The effective annual interest rate includes these costs and provides very accurate information on the total cost of the loan.

Why are there at least two different interest rates in the loan agreement?

Anyone who wants to take out an installment loan from a bank should definitely find out about the costs in advance. A professional loan agreement always contains two different indicators or interest rates. On the one hand, there is the debit interest rate and on the other hand the effective annual interest rate.

The debit interest rate indicates the basic compensation the bank requires for granting the loan. From an amount of 10,000 euros and an interest rate of 5%, debit interest of 500 euros would accrue after a term of 12 months.

The effective annual interest rate is much more precise here for comparing the different loan offers. In addition to repayment and debit interest, there are, for example, bank processing fees and possible costs for default insurances.

The loan agreement always contains both values in order, on the one hand, to recognize the difference between the debit interest rate and the effective interest rate and, on the other hand, to allow the borrower to accurately assess and calculate the costs.

Which interest rate is relevant for the interest calculation of my loan?

In a financing arrangement it is important that the interest is precisely determined in advance. The debit interest rate is used to perform the interest calculation. Only with it can the interest per year, per month or for the entire term be calculated.

Is the interest rate fixed for the entire term of the loan?

This entirely depends on the lending bank. Sometimes loan agreements are offered with fixed interest rates, but sometimes also with temporary interest arrangements. If a loan is to be paid off over 30 years, it often happens that the interest is fixed, for example, only for 10 years and then adjusted to the current market situation.

The borrower should therefore carefully consider which decision to make beforehand, because the determination can have both positive and negative effects. If the interest rate is fixed for the entire term and interest rates become significantly cheaper after 10 years, the higher interest would still have to be paid. If the interest rate prevailing at the respective time is cheaper than at the start of the contract, the borrower saves money from that moment on, which can, for example, be invested in higher repayment.

Advantages and disadvantages of the effective annual interest rate

Advantages and disadvantages are hard to identify for the effective annual interest rate. Nevertheless, we want to try to explain the positive and negative aspects clearly.

Advantages:

- The total costs of the loan can be seen immediately.

- Different loan offers can be compared with one another.

- Household budget planning is significantly easier.

Disadvantages:

- The effective annual interest rate only indicates the total costs.

- Individual items cannot be broken down by it.

- Attractive effective interest rates and thus cheap loans can lead to unintended expenses.

Who determines the effective annual interest rate in a financing?

With the numerous pieces of information from our article, the borrower can surely recognise that the annual interest rate is not simply set arbitrarily. Fundamentally, it results from the following costs:

- interest

- processing fees

- residual debt insurance (possibly)

The interest rate is, in turn, dependent on many different factors. It is oriented towards the key interest rate issued by the central banks. All banking institutions that belong to the central bank orient themselves to the key interest rate to calculate their own financial products accordingly. If the key interest rate rises, the rates for the end consumer also become more expensive. This leads to more expensive loans and, in the long term, probably to fewer investments.

The key interest rate has always been a good instrument to stimulate the economy. If investments decline and customers literally hold onto their money, a low key interest rate can help make loans cheaper and therefore more frequently used again.

The processing fees primarily depend on the business policy of the respective bank. Here too there are significant differences. Especially with internet banks, fees are often much lower than with a traditional house bank. This is due, on the one hand, to the significantly smaller personnel base that an internet bank has and, on the other hand, to the absence of costs for ATMs and other things. Since the customer performs most tasks online at an internet bank, the company can attract customers with favorable terms.

If a residual debt insurance is taken out, these costs are added to the effective annual interest rate. This is always advisable when an employment contract is at risk or was limited. It is also certainly a good decision to take out residual debt insurance in particularly risky professions. If a case of inability to pay occurs, the residual debt insurance takes over the subsequent installments or the entire loan.