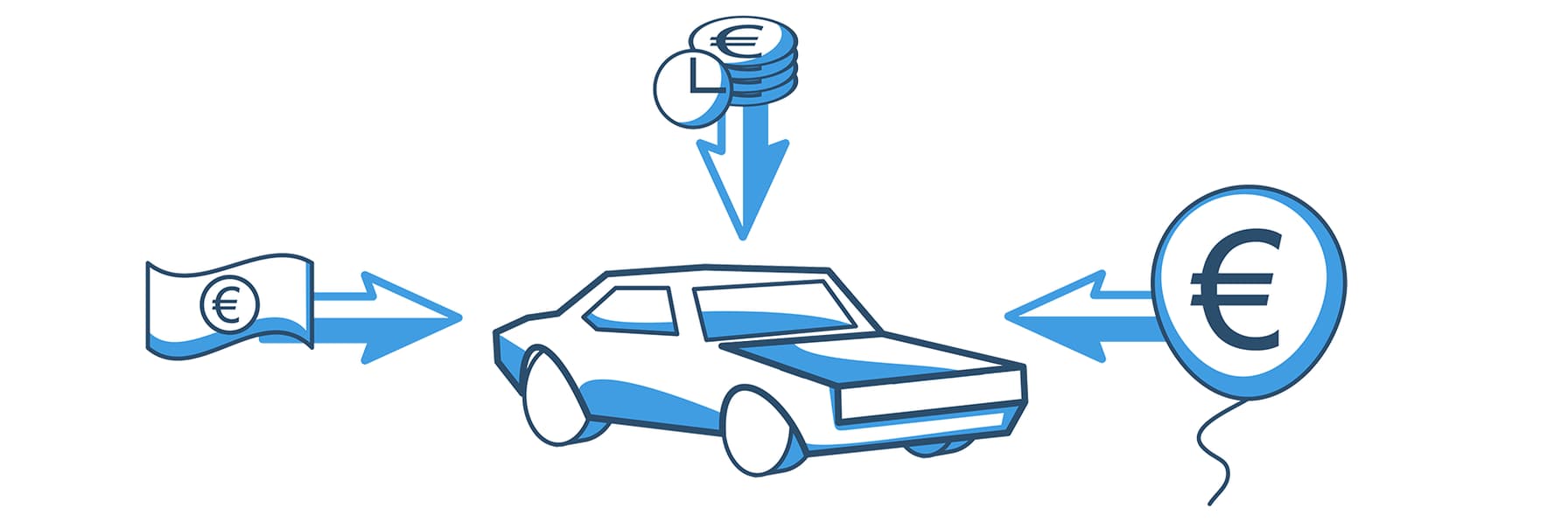

Balloon financing — Using a vehicle loan to get a new car

Mobility is one of the most important achievements of modern times. Especially in rural areas, people can be stuck without a vehicle. Even if there are small shops, petrol stations and kiosks in towns, a car becomes necessary at the latest when you need to reach work, a hospital or other more distant destinations. But how do you buy a car if the necessary capital is not available? One of the most popular forms of credit is balloon financing. In this guide we will explain in detail how it is used, how it is calculated and when it is applied.

What is balloon financing?

Basically, balloon financing, also called final installment financing, is a widespread form of vehicle financing. The principle is very similar to leasing or hire purchase. Loans granted in the form of balloon financing are built on a basic principle:

- Small monthly installments

- Little or no down payment

- Very large redemption amount or final installment (balloon)

The reasons for the popularity of balloon loans for car financing are obvious.

Dealer advantages: Dealers have a very good sales argument for their customers. Attractive marketing offers promise a low-rate installment loan and thus create a real boom in balloon financings.

Customer advantages: Car buyers benefit from the favorable terms of car loans under the balloon method. Even without capital contribution, a new or used vehicle can be financed easily. Only the monthly installments of the financing must be paid.

Unfortunately, many customers lose sight of the very large final installment, the so-called balloon, when buying a car. In principle, they only cover the car’s depreciation each month. As a result, the monthly burden can be kept relatively low depending on the vehicle type and value, which encourages customers to buy.

The very high final installment can be settled by a follow-up financing. Alternatively, the vehicle can be returned to the dealer after the balloon financing, or the car can be sold on the open market. All three options have advantages and disadvantages, which we will look into in more detail later in this guide.

What is a balloon payment?

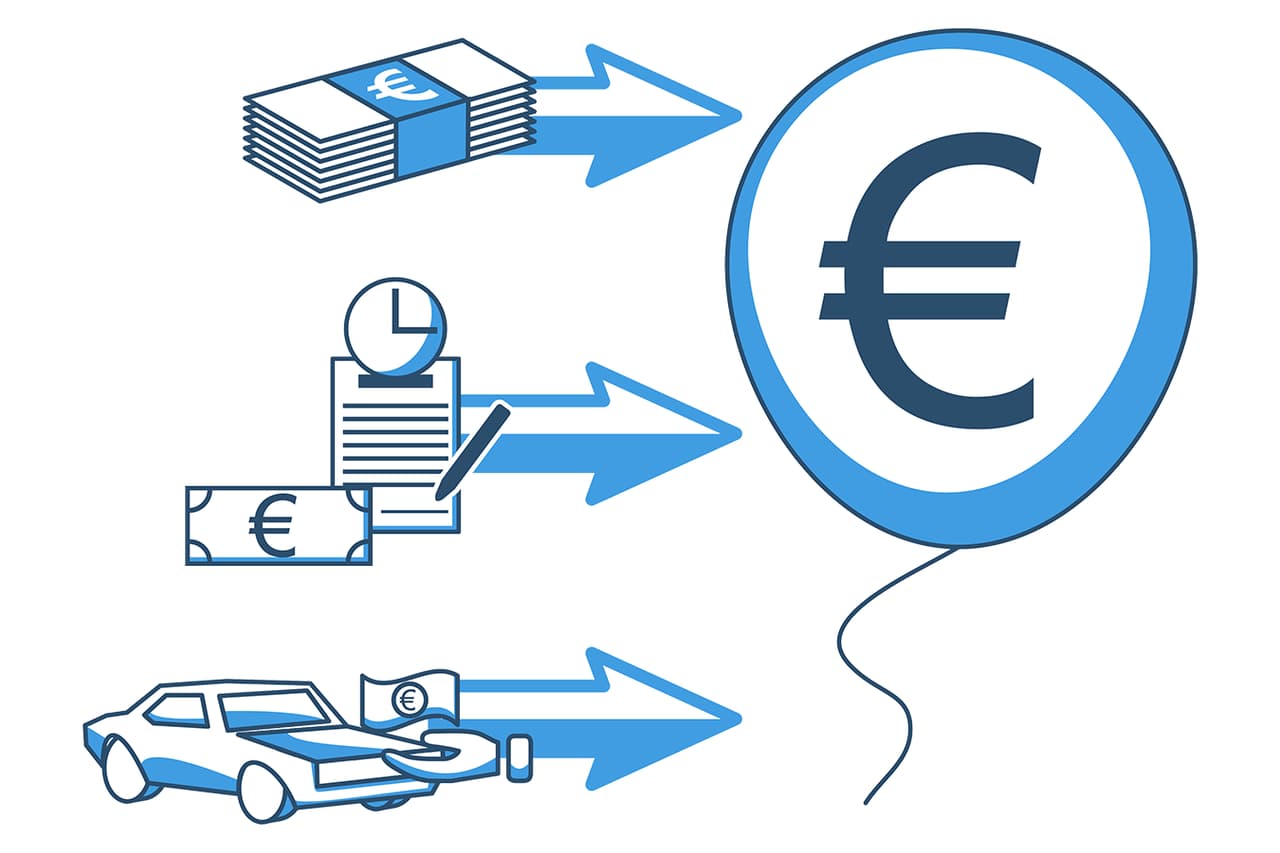

The balloon payment is the amount that remains after paying the agreed installments and at the end of the balloon financing, and which in the best case can be covered by the vehicle’s residual value. In a balloon loan the balloon payment is always very high, because the main feature of this financing type is the small monthly installments. Whoever pays less earlier must expect a correspondingly higher final installment later.

The balloon payment can be settled in several ways:

- In cash

- With a follow-up financing

- By selling the car

- By returning the vehicle to the dealer

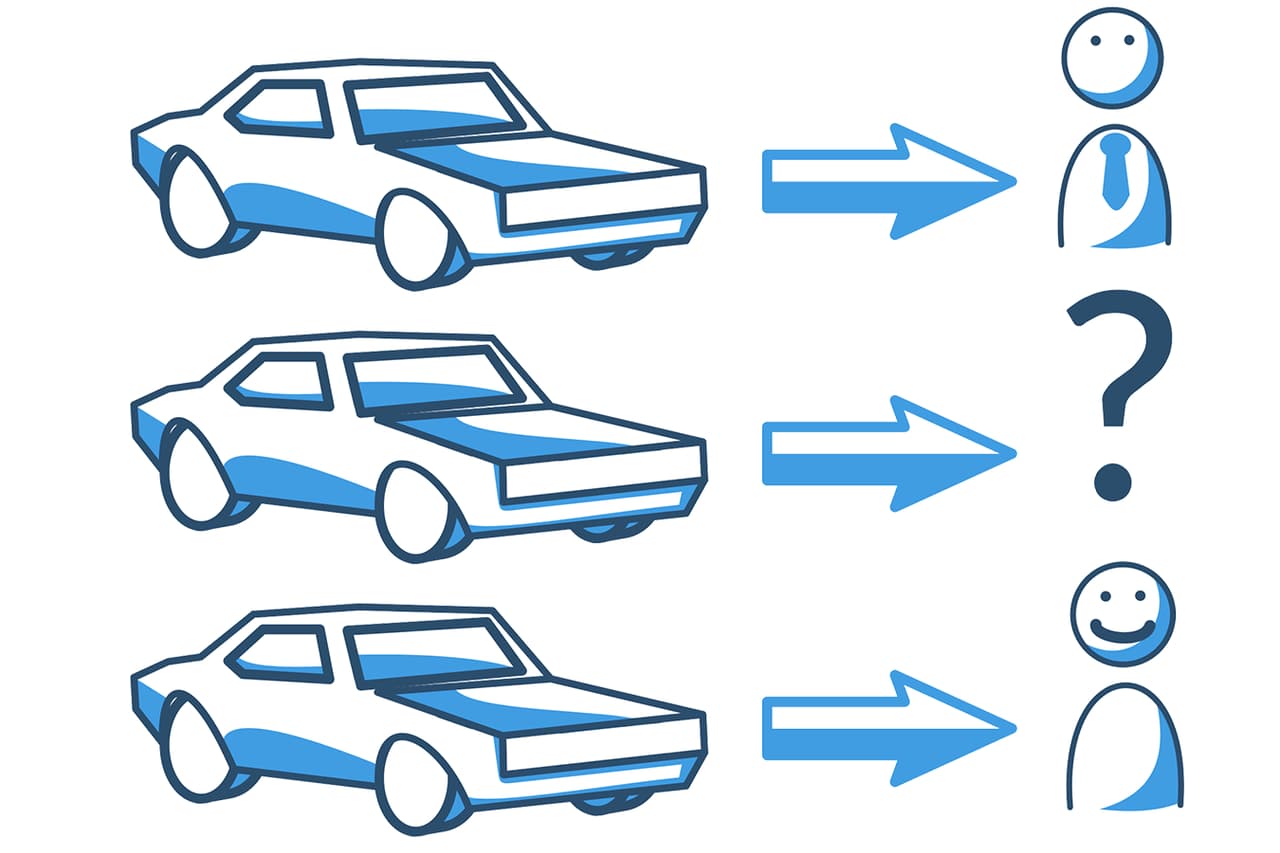

Why is balloon financing also called three-way financing?

Balloon financing is also known as "three-way financing". This is due to the fact that at the end of the term the borrower must decide between one of three possible ways to deal with the vehicle.

Return to the dealer: One option is to return the vehicle to the dealer. When the balloon loan term is over, the car can be returned to the dealer. The dealer will of course inspect the condition of the vehicle and determine its actual market value. If, for example, a final installment of €12,000 was agreed at contract signing and the car is only worth €8,500, the borrower must make up the difference.

Sale on the open market: Of course the borrower can also sell the vehicle on the open market. The chances of achieving a suitable sale price may even be significantly better here than with a dealer. This depends on the model, equipment and condition of the vehicle. Certain brands and models offer advantages here because they are easier to sell than cars from other manufacturers. Vehicles with exotic equipment also often struggle to find a new owner later.

Retention of the car: The third option is to keep the car. In this case the borrower must pay the final installment previously agreed in the contract. If the necessary funds are not available at that time, the balloon payment can be settled with a follow-up financing. This may then incur additional or higher costs and interest than during the balloon financing.

Who is a balloon loan suitable for?

This question cannot be answered universally. It depends entirely on the circumstances. Balloon financings (also called balloon loans) were developed to make it easier for end customers to buy a vehicle. Credit institutions continually come up with new products to persuade customers to conclude a loan contract. Nevertheless, we want to mention some examples in which a balloon financing may be particularly suitable.

Students

Students all face the same problem. Important universities are often out of reach. Sometimes a move to a larger city is worthwhile, but in many cases a car removes the greatest mobility obstacles. Unfortunately, most students also cannot afford a car. Besides university, there is often only room for a part-time job, whose income is almost entirely used for living expenses.

Balloon financing is therefore very suitable for students because the small monthly payments fit their financial situation. After concluding a vehicle financing, the car is available and can be paid for with small installments. Here too the large final installment and possibly another loan to cover it are issues, but only at the end of the term.

Families

Families also like to use balloon financing for car purchases. If both parents work, a conventional financing with higher repayments should also be possible. If the family grows and one parent cares for the children, income may fall after parental allowance expires. Without a car, family life is hard to manage. Children must go to the doctor, attend sports, repeatedly need school materials and naturally depend on their parents. A balloon loan helps families finance a car even in financially difficult times, with small monthly payments.

Young people

Young people who have just moved into their first apartment often do not have a lot of capital. On the one hand they have to pay for furnishing the apartment, utilities and of course the rent, and on the other hand earnings at the start of a career are often not yet high enough to buy a car. Balloon financing is the perfect product for young people who want to be mobile but can only afford a small monthly amount for a vehicle.

Self-employed

Especially at the beginning of self-employment, balloon financing is a very good way to drive a presentable company car without being burdened by a very large monthly amount as is often the case with leasing or classic car financing. The self-employed person initially only pays the vehicle’s depreciation and only after the term the relatively high balloon payment.

In principle, the car loan in the form of balloon financing is suitable for people who:

- want to drive a car only for a certain period of time

- are currently in a financially difficult situation (but not in case of: over-indebtedness, collection processes, negative Schufa score)

- do not want to spend a lot on mobility each month

- are not sure whether they want to keep the car

- accept the risk of repaying the car later with a more expensive follow-up financing

- accept the risk of selling the car later for a lower price than the balloon payment would require

Is balloon financing purpose-bound? For what use should a final-installment financing be taken out?

The lending bank stipulates that a final-installment financing may only be used to purchase a vehicle. Because the car serves as collateral, special terms can be offered. For this purpose the bank retains the vehicle registration document. The borrower must prove the vehicle purchase with a copy of the purchase contract.

What is the usual term of balloon financing?

All financings have something in common. They are concluded for a certain term. During this time the loan amount is either repaid in full or settled with a final installment. The same applies to balloon financing. The dealer provides a car loan through the participating bank that is concluded with low installments and a large final payment.

Balloon financing is usually agreed for a period of 12 to 60 months. Important criteria for calculating the term are the following.

Follow-up financing: If no follow-up financing is desired, the car must either be paid for in cash, returned or sold on the open market. In the case of a sale, the sale proceeds should definitely cover the final installment. Thus, the calculation of the balloon financing is based on the expected residual value of the vehicle. If calculated incorrectly or if a term that is too long is chosen, the residual value can be significantly lower than the final installment. The resulting difference must then be balanced with another financing.

Vehicle type: Depending on the vehicle type, a higher or lower residual value must be assumed. Some cars sell better than others, even if age, equipment and condition are very similar. Popular vehicles sell more easily and at better conditions.

Manufacturer’s warranty: Since a vehicle’s value drops rapidly when the manufacturer’s warranty expires, this must of course be included in the term calculation. Some manufacturers provide a warranty of 2 years, others up to 5 years or more. In some cases it even makes sense to extend the manufacturer’s warranty by an additional payment in order to sell the car later at a significantly higher price.

How large may the loan amount be in balloon financing?

The size of the loan amount is mainly determined by the vehicle to be financed. Nevertheless, many banks set upper limits when granting loans. These mostly range between €50,000 and €100,000. Exceptions confirm the rule here as well, but require individual agreements with the financing bank.

Typically, however, the loan amount in balloon financing is well below the amounts mentioned and only in a few cases are particularly expensive vehicles financed.

Costs of balloon financing

How high are the interest rates in balloon financing?

Car financings typically come with particularly favorable loan conditions. Anyone who wants to finance a vehicle should, in principle, do so only via dedicated vehicle loans. The financed vehicle serves as collateral for the lender. If the borrower no longer pays the monthly installment, the vehicle can be repossessed and sold to settle the outstanding debt. For this reason, the vehicle registration document is handed over to the bank until the loan is paid off. This gives the bank decision-making power and prevents an unwanted intermediate sale of the car, or it must first approve such a sale. If the sale proceeds are insufficient to cover the outstanding debt, the borrower only has to pay the difference.

This is an important reason for the low interest rates associated with balloon financing. Since the vehicle also serves as collateral for the car loan here, interest rates can be kept particularly low, also independently of the borrower’s credit rating. Nevertheless, a positive Schufa report must be available to actually apply for balloon financing.

The actual repayment of the vehicle loan is almost entirely deferred to the final installment. Even so, this portion must of course be charged interest. For this reason the monthly installment is divided into depreciation and interest. To account for inflation or interest rate developments over the term, these costs are included in the interest rate.

What fees are charged for balloon financing?

Of course fees are also charged for balloon financing. These additional expenses vary depending on the bank. Normally customers can expect processing fees between 2 and 5 percent of the loan amount. To offset these costs, they are calculated in advance and then included in the total loan amount.

If the customer repays a loan faster than expected, these fees are not refunded. Sometimes quite the opposite happens: for early repayment many banks charge a so-called prepayment penalty. It is therefore important to examine the terms of the balloon financing carefully.

Additionally, it should be mentioned that there are many providers who completely waive fees for a balloon loan.

What collateral is required for balloon financing?

In most cases the vehicle itself is sufficient as collateral. For this reason the bank requires a legible copy of the purchase contract as well as the vehicle registration document. At the same time many banks require a security transfer. In this the buyer agrees that the bank may sell the vehicle in the event of non-payment of monthly installments and use the proceeds to repay the loan.

Despite the collateral in the form of the car, creditworthiness must of course be positive. The bank obtains a report from Schufa or another scoring agency when applying and decides based on the score whether financing is possible. The main reason is not the actual term of the balloon financing but rather the follow-up financing of the relatively high balloon payment. The bank already assesses at the time of loan approval whether the buyer will probably be able to pay this loan with his or her current creditworthiness. A secure and regular income, as well as a positive payment history, are therefore essential.

Is there an interest rate fixation with balloon loans?

In most cases balloon financings are issued with an interest rate fixation. This is valid for the entire financing period and only ceases to apply with the final installment. If a follow-up financing is concluded after the loan term, the current market interest rate applies and no longer the rate from the balloon financing.

Termination and special payments for balloon financing

Many customers naturally wonder whether they can simply exit a balloon financing. In principle this is possible, but subject to certain conditions:

- The entire outstanding debt must be settled.

- The bank may demand prepayment penalties.

- The bank may charge compensation fees of up to 1% of the outstanding debt.

Borrowers whose term is less than 12 months left are somewhat lucky in misfortune. Here the fees are limited to a maximum of 0.5% of the outstanding debt. Many banks, however, simply levy other fees in this case to offset the loss. It is best to carry out a thorough comparison of the available balloon financings and choose a lender that allows free special repayments and otherwise charges only low fees. If fees apply, they are usually very high because the large final installment constitutes a large part of the loan debt.

For which financings do balloon loans make sense?

Balloon loans are primarily intended for the purchase of a vehicle. They make sense whenever the buyer is not sure whether he wants to keep and drive the car in the long term, is in a financially difficult situation, or simply does not want to spend much money on mobility each month. Whether a balloon loan actually pays off in the long run depends on several factors. The vehicle type, the expected residual value and any additional bank fees should definitely be considered. The balloon loan is inexpensive over the term. However, repayment of the large final installment can be costly depending on the interest rate level and fees.

Comparing balloon financings

Which provider should you choose for a loan with a final installment?

In general, almost all banks and credit institutions offer balloon financings. In addition, there are now numerous vehicle financiers and manufacturers that cooperate with subsidiaries of well-known banks or have even founded their own in-house bank to be able to offer attractive financing options to customers. In most cases the subsidiaries are exclusively responsible for vehicle financing.

To find the best provider for a final-installment financing, the car buyer should first carry out a comprehensive comparison. Afterwards the individual offers and their terms can be compared.

What should you look for when comparing different balloon loans?

Since fees in most cases are similar or are not charged by banks at all, the comparison of balloon financing should initially take place on another level. The question is: "How does the balloon loan differ from a leasing contract or an ordinary installment loan?" In addition to the designation, required collateral and of course the terms, different types of financing can best be assessed by determining the present value. This is quite simple and provides immediate information about the expected costs.

The present value is the amount a borrower would have to pay now in order to cover all costs arising from the balloon loan. The different repayment times are already taken into account in the present value, so it gives an accurate insight into the actual costs incurred. The lower the present value, the cheaper the overall financing.

The effective interest rate can also be used for further comparison. The bank must state the effective interest rate for the financing. This includes the interest but also the additional fees and how they effectively affect the entire term. If a provider waives the processing fee for the balloon financing, this is already a positive sign that should be included in the comparison.

When should you take out a balloon loan?

The right time for a balloon loan is not determined by external influences. Whenever someone needs a car and cannot afford the rate of a conventional loan or a cash purchase, a balloon loan is the best solution. A vehicle is very expensive to acquire. Balloon financing creates room for manoeuvre here because it brings very low installments and only a large final payment. By the time the final payment becomes due, the borrower’s financial situation may have already improved. To weigh up this risk, banks always obtain a creditworthiness report.

If the buyer is not sure whether they want to keep the car permanently, balloon financing can be the perfect alternative to leasing. In car leasing the installments are significantly higher so that the final installment does not become so high and a large part of the loan amount is repaid as quickly as possible.

Is the balloon loan a cheap financing option?

This question is also difficult to answer in general. Too many influencing factors play a role in calculating the actual costs incurred by the borrower in balloon financing. On the one hand, of course, there are the interest rates that partly determine the level of costs, and on the other hand some banks charge additional fees for prepayment or processing of the loan application.

When assessing whether a financing is inexpensive, a current snapshot should definitely be taken. The following questions can help:

- Is the relatively small monthly rate of the balloon financing currently favourable for me? Does this form of financing relieve my household budget?

- Am I able to pay the large final installment after the balloon financing ends?

- Do I accept that the interest rates and fees for follow-up financing will be significantly higher than for the balloon loan?

- Do I accept the risk that my car will be worth less after the balloon financing term than the final installment to be paid?

All car buyers who can answer the above questions with "yes" should examine the terms and conditions of balloon financings more closely.

Balloon financing compared to other loan types

Car loan: Classic financing or balloon financing

Anyone who wants to buy a car but does not currently have the necessary funds can finance the vehicle with a loan. The classic financing model is the consumer loan or installment loan. The aim of the consumer loan is to repay a certain amount to the bank within an agreed period.

Classic financing

The amount of the installments depends on the term and on the loan amount.

- After payment of the last installment the loan is fully repaid

- The car becomes the property of the borrower after repayment of the loan

- For the duration of the financing the vehicle registration document remains in the possession of the bank

Most people are familiar with the classic loan in one form or another.

With balloon financing different rules apply, which make this type of financing particularly attractive for the groups mentioned above. Although monthly payments are also due here, they contribute less to amortising the loan amount and more to compensating for depreciation. In addition a large part of the installments consists of interest.

Balloon financing

- The installment amount depends on the term and on the calculated residual value of the vehicle

- After payment of the final installment the buyer must decide what happens to the vehicle. If it is returned to the dealer and the residual value is lower than the final installment, the difference must be paid. If the borrower sells the vehicle on the open market and the sale proceeds are lower than the final installment, the difference must also be paid. If the customer wants to keep the car and settle the final installment with a follow-up financing, additional costs in the form of higher interest may apply

- The vehicle does not automatically become the property of the borrower at the end of the term

- For the duration of the financing the vehicle registration document remains in the possession of the bank

When deciding between a classic loan and a balloon financing, it always depends somewhat on the borrower and which option best suits their financial situation. The starting situation is an important factor.

Vehicle financing: Leasing or balloon financing?

Leasing is familiar to most people. Many also see it as "renting" because the leased item is not bought but only leased. The lessee thus pays a monthly leasing rate that combines depreciation of the vehicle, interest, the lessor’s profit and any additional costs. If a leasing contract is concluded for a period of 3 years, you pay a constant monthly rate. After the period, the customer can decide whether to keep the car, sell it or return it to the leasing company, which then disposes of it as a lease return. Leasing rates are relatively high compared to balloon financing installments. This is partly due to the lessor’s profit, but also interest, the vehicle’s original price and the term. Returning the vehicle in leasing is not as straightforward as with a balloon loan.

The lessor, for example, agrees an annual mileage with the lessee. If this is exceeded, the leasing company can charge a fixed fee per excess kilometer. If €0.75 per excess kilometer was agreed and the lessee returns the vehicle with 3000 excess kilometres, they must expect a bill of €2,250. But that is not all. The dealer subjects the car to a thorough inspection.

- Has it been well cared for?

- Does the interior smell of cigarettes or nicotine?

- Were damages reported immediately and repaired by a specialist workshop?

These and other aspects can lead to a drastic reduction in the car’s value. The difference between the actual and the contractually agreed market value must be paid by the lessee. Leasing is primarily suitable for companies for vehicle financing. Vehicle fleets that are used daily often consist of leased vehicles. The best example is Deutsche Post. In addition, companies can deduct monthly leasing rates as expenses and thus claim them for tax purposes.

Balloon financing, in contrast to leasing, is considerably simpler and also pursues a different intention. It is designed to encourage the purchase of a car and advertises low interest rates and small monthly installments. Although there are some overlaps with leasing, these two financing variants fundamentally differ in approach.

As already mentioned, the monthly installment is significantly lower than in a leasing contract or in a classic financing of an identical vehicle with the same equipment.

Advantages and disadvantages of balloon financing

Advantages of balloon financing

The final-installment loan basically has similar advantages to other loan types. Primarily, financing allows you to buy something you could not have afforded without a loan. The bank goes into "advance" and charges interest and fees for its service.

Nevertheless, balloon financing has one unique advantage over other financing models:

The monthly burden is significantly lower than with a conventional consumer loan.

If the financing offer waives a down payment, borrowers can finance a vehicle even if their household budget would not normally allow it. The reason is the capital tie-up that affects the entire balloon loan. Because the capital or value is tied up in the vehicle and is still present after the term ends, the value does not need to be financed during the balloon financing term.

Another advantage is the very short terms that are possible with a balloon loan. Depending on the bank, terms between 12 and 60 months can be agreed. So anyone who wants to change vehicles frequently should consider balloon financings.

What should be taken into account when concluding a final-installment loan?

Borrowers should always read all important contract details before signing. Are the personal details correct? Have all variable factors been correctly included in the loan contract? Only if these details are complete and truthful should the loan be taken out.

In addition, there is an important note about the business practices of some banks:

It often happens that banks include a residual debt insurance in the loan contract. This insurance steps in when the borrower can no longer pay their monthly amount. The insurance then covers the outstanding debt, but of course charges a high price for this service. Residual debt insurance can significantly increase the effective interest rate and thus the present value of a loan. This clause should definitely be removed.

If a bank does, however, offer favorable insurance and maintenance contracts for the financed vehicle, these conditions should definitely be compared with the market offers of other insurers. In many cases the conditions of manufacturers’ banks are considerably cheaper, which is why many offers are made as a package. The vehicle, insurance and maintenance intervals are included in the package. This can save money.

Disadvantages of balloon financing

Everything that has advantages also has disadvantages. This adage also applies to balloon financing.

Repayment burden: A large part of the repayment burden is shifted to the final installment in a balloon loan. This can be a risk because the actual sale proceeds of the vehicle can be significantly lower than the contractually agreed residual value. The buyer must pay the difference out of pocket.

Interest rate level: If a follow-up financing is required at the end of the term, the interest rates and other fees charged by the respective bank can be significantly higher than those of the original balloon financing. If the interest rate level is very high at the time the balloon loan ends, more and longer payments will be necessary for the vehicle than planned. This risk cannot be calculated when buying the vehicle.

Interest: Interest during the balloon loan term is on the whole somewhat higher than for an installment loan. This is because the final installment is so high and a large part of the monthly payments must consist of interest to compensate for the deferred repayment and to produce the lender’s profit.

Can the final installment always be refinanced?

That is of course possible. When the term of the balloon financing has ended, the car can become the borrower’s final property by paying the final installment. However, they must then pay the final installment. If the borrower cannot raise the money immediately, a follow-up financing is required. While the balloon loan was issued with an interest rate fixation, the follow-up financing will be subject to the interest rate level prevailing at that time. The second loan for the car may therefore be significantly more expensive than the original financing in the worst case.

Balloon financing without Schufa

How do you get a car loan without Schufa and with a final installment?

Many refer to balloon financing as a car loan without Schufa and with a final installment. This is of course not quite correct, because a customer will not get a car loan from any reputable credit institution without a positive Schufa report. Nevertheless, there are caveats that probably led to this misunderstanding.

Creditworthiness is a decisive factor for the level of interest in any car financing. Banks and car dealers generally orient themselves to the current interest rate level and design their offers accordingly. If a borrower’s creditworthiness is not flawless, a risk arises for the bank. The lending company offsets this risk with a higher interest rate.

This does not work the same way with a balloon loan. Since the car is the actual collateral for the bank and it therefore retains the vehicle registration document until the final installment is paid, no Schufa check is used in calculating the interest. To be granted the actual car loan, however, a very good to good Schufa score without significant entries must also be present in balloon financing.

Thus the idea of a car loan without Schufa and with a final installment is more wishful thinking than reality. The creditworthiness check is carried out both as protection against losses for the bank and to protect the borrower from over-indebtedness.

Concluding a balloon financing contract

To avoid waking up to an unpleasant surprise when signing the contract, all important aspects of the financing must be truthfully and correctly included in the contractual documents. Especially the small print often requires close attention, because banks like to include the so-called residual debt insurance here.

Anyone who simply overlooks this section may later face significantly higher monthly installments. To avoid unnecessary costs, this clause should be removed from any loan contract before signing. To speed up the entire process, the borrower can prepare the required documents and provide them to the bank on request. These include identity documents, proof of earnings, employment contract, purchase contract and of course the vehicle registration document. Communication between the bank and the dealership is very important here. The bank grants the loan only if it also receives the vehicle registration document, while the dealer only releases the document if they have loan confirmation. This situation is in most cases the reason for a delay in processing the balloon financing application.

Do banks offer additional services with balloon financing?

Manufacturer-owned banks in particular offer attractive packages to customers that usually consist of a complete package. This package already includes insurance, the monthly rate, interest and the costs for regular maintenance. If a consumer opts for such a contract, they generally need do nothing else apart from registering the vehicle at the licensing authority. Most dealers even take care of that task for a small additional charge.

Before concluding a combined package, the terms of other insurers should nevertheless be compared with the dealer’s conditions. The following questions can help:

- What is the deductible in the event of damage?

- Am I fully comprehensive insured?

- Which additional services are included in the policy? (Roadside assistance, ADAC, replacement vehicle, hotel, etc.)

- Can I switch back to an independent insurance at any time?

Once these questions are clarified, nothing stands in the way of concluding a balloon loan contract.

How can you apply for a balloon loan?

While borrowers previously had to appear in person at the bank branch, today the application can be made by phone or via the internet. Of course visiting a branch is still possible, but internet banks generally offer more favourable conditions because they save on branch and personnel costs.

To apply for a balloon loan, the car dealer initially needs a few key data:

- What is the gross salary?

- How much is the rent including utilities?

- Own property or rental apartment?

- How many people live in the household?

- What is the household’s total income?

He then submits a non-binding request to the lending bank, which is answered online within a few minutes. If information is still missing, it can subsequently be conveniently submitted by phone or post. The application for balloon financing is then processed within a short time.