Civil-servant loan

Sometimes it feels like a nightmare. Everything happens at once. The washing machine breaks down, the refrigerator only hums, and the car struggles to start. Then there’s the loan whose repayment becomes harder year by year. Monthly payments increase. How is all of this to be paid? And actually, this year the long-awaited family trip to the Caribbean is planned.

Everyone knows situations like this. Suddenly an entirely unexpected problem occurs. Maybe not everything comes crashing down at once. But often several things happen that you did not anticipate. One thing is followed by another and another. Sometimes you can only shake your head in despair. What to do? How can all of this be paid at once? A personal loan helps to bridge bottlenecks.

Civil servants are fortunate even in such situations. With a civil-servant loan they receive a loan that features particularly favorable terms. That provides immediate relief. Some things are secure — for some it’s pensions, for a civil-servant loan it’s the installments. The installments on a civil-servant loan are reliably low and remain so. Likewise, interest rates remain low throughout the entire loan period. Loan terms are between twelve and 20 years. Everything stays stable and manageable.

A working washing machine, a modern energy-efficient refrigerator, a new car, loan consolidation and the dream Caribbean holiday are therefore no problem. Every difficulty can be solved. Every new purchase can be paid for. Many civil servants will surely feel a weight — or even a boulder — lifted from their shoulders. But what exactly is meant by a civil-servant loan?

What is a civil-servant loan?

Civil servants and employees in the public service enjoy an advantage over other workers: their jobs are very secure. The chance of losing the job and becoming unemployed is virtually zero. Lenders are therefore on the safe side regarding the repayment of the money lent. For this reason they grant this particular group of professions special conditions. However, this applies under certain conditions and exclusively to civil servants and to certain public-sector employees.

A civil-servant loan must be repaid by a specified cut-off date. Possible terms until then range between twelve and 20 years. These personal loans are therefore often taken out for the long term. As a result, the monthly installments remain low. This applies for the entire payment period. The interest charged is also not as high as with other debt instruments.

Civil-servant loan — what is it? In short:

- A loan for civil servants and certain public-sector employees,

- combined with a whole life insurance policy or a pension insurance,

- with particularly favorable conditions for interest rates and monthly installments, and

- long terms.

Is there a difference between civil-servant credit and civil-servant loan?

The terms civil-servant credit (Beamtenkredit) and civil-servant loan (Beamtendarlehen) are often used interchangeably in everyday language. That is not entirely correct. Different banks and lenders use the two expressions differently.

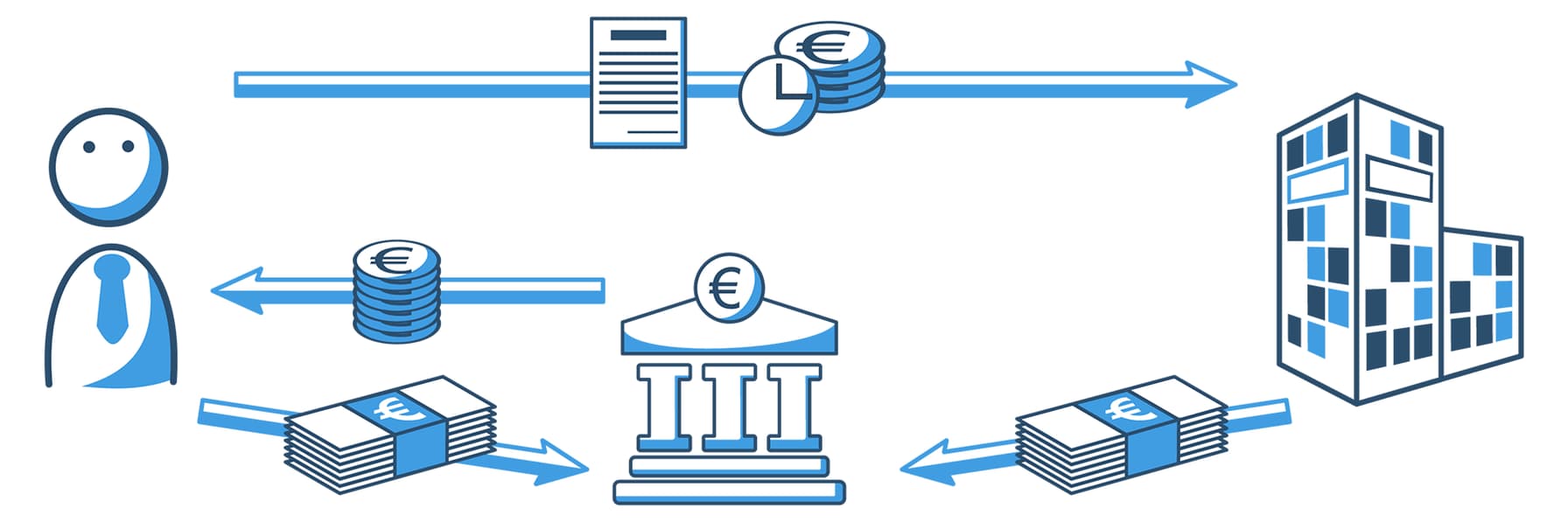

Civil-servant credit and civil-servant loan represent two different financing options. They are similar but differ in structure. So what is what? The term civil-servant credit is not protected. It is simply the sum a credit institution lends to a civil servant. A credit for civil servants — a personal loan or installment loan made available exclusively to this professional group. They receive it on particularly favorable terms. Features such as high loan amounts, long terms of up to 20 years, and fixed, low monthly installments can be found with both civil-servant credit and civil-servant loan. Unlike the civil-servant credit, a civil-servant loan is linked to a pension insurance or a whole life insurance policy. Monthly installments and interest for a civil-servant credit are paid directly to the lender. With a civil-servant loan the borrower pays the repayment installments to the insurance. Only at the end of the entire term does the lender receive the full loan amount back, whereas interest for the provision of the money is due immediately.

The civil-servant credit is thus a special form of the personal installment loan. The civil-servant loan combines loan and insurance and thereby forms its own payment model.

Civil servants can therefore choose whether to take out a civil-servant credit or a civil-servant loan depending on their needs and wishes. Thanks to the link with pension insurance or whole life insurance, those who opt for a civil-servant loan automatically provide protection for themselves and their families. In the event of illness or death, the costs are covered. That is not the case with a civil-servant credit. However, as with any other installment loan, a residual debt insurance can be taken out additionally. It covers payments in case of inability to work, need for long-term care, or death.

How does the civil-servant loan work?

The key is: the loan is combined with a life or pension insurance.

The monthly premiums for this protection are paid by the borrower directly to the insurer. The loan amount itself is repayment-free during the term. And what about the interest? With installment loans interest often increases over the term, which is not what you expect at the start of payments. In this case it does not. Interest remains low until the borrowed sum is repaid. Civil servants or public-sector employees pay the due interest directly to the lender. Only at the end of the entire term is the loan repaid by the accumulated whole life insurance. With the monthly fixed repayment amounts the life insurance is funded. For the loan itself, initially only interest is due.

Did someone unexpectedly inherit money or receive a gift? Then use it to repay the civil-servant loan. Special repayments reduce the outstanding balance. The sum that has to be repaid in full at the end is therefore lower.

If the insurance yields higher-than-expected returns, is there a surplus? Yes, that is possible. Of course the debtor receives this paid into their account at the end of the loan term.

But what happens if someone unexpectedly cannot work anymore? You slip on a slippery floor at work, break your ankle and are out of the job. In serious cases it can take longer than expected if the fracture is more complicated than initially thought. Nobody is immune to accidents or to illnesses that last weeks or months. The longer the loan term, the higher the risk that the borrower will be unable to work before the loan is repaid. This can happen because the job can no longer be performed or, in the worst case, because the borrower dies. An occupational disability insurance and a term life insurance help in such situations. They take over payments in an emergency. The family is thus protected from financial disaster.

Be cautious with offers for civil-servant loans that are supposed to run ten years (120 months) and do not include life insurance. The term “civil-servant loan” is not protected. Any ordinary installment loan can therefore be offered to a civil servant under this name. Reputable lenders, however, link the loan term to the term of the whole life insurance for a correct civil-servant loan. That is how the customer is best protected.

How much money can I borrow with a civil-servant loan?

The amount of the loan depends on the net income of the civil servant. The higher the income, the higher the possible loan amount. As a rule, the loans granted equal 20–25 times the net income. Don’t need such a high loan amount? With a civil-servant loan you can of course also borrow a smaller amount. It always depends on the individual case. Be sure to get detailed advice from the lender of your choice.

Advantages of the civil-servant loan

The civil-servant loan is structured for 12–20 years. This period is required because insurers have a minimum term of twelve years. Consumers can thereby repay larger loan amounts over the long term with low installments. It is also possible to reduce the final repayment amount through special payments. These special repayments reduce the current interest burden because the loan sum decreases. The monthly burden on borrowers is thus reduced. In addition, a larger sum can be paid out from the life insurance at the end of the loan term.

Advantages of the civil-servant loan in brief:

- The loan amount is freely selectable.

- Installments remain low.

- Interest is low for the entire loan term.

- The loan can be repaid in the short or long term.

- Special repayments are possible.

- A term life insurance protects the family.

Who receives the civil-servant loan? Which professional groups benefit from the favorable civil-servant credits?

The name says it: a civil-servant loan is generally granted to civil servants. It is a specified sum that a credit institution lends to civil servants for a certain time. Specific conditions are set for this. This usually applies to civil servants for life — but there are exceptions. In some cases other variants and other professional groups can take advantage of this special loan.

The civil-servant status can be conferred as revocable, on probation, for a fixed term, or for life.

Civil servants for life can include:

- Police officers

- Teachers

- Judicial officers

- Postal civil servants

- Professors

- Academics

- Pensioners

Career soldiers and judges are not civil servants. Their remuneration and benefits are, however, aligned to those of civil servants.

Revocable, on probation, fixed-term or for life — when does which civil-servant status apply?

The civil-servant status is granted by the state and recorded with a certificate. Does working for a state employer make you a civil servant for life immediately? Of course not. Those undergoing training in the lower, middle, upper, or higher service are civil servants on a revocable basis. For teachers this applies, for example, during the trainee teacher period. After the state exam, one becomes a civil servant on probation. Police commissioners are also civil servants on a revocable basis until they have passed their state exam.

As with employees, civil servants also have a probationary period. This usually lasts three years. It can be shortened or extended by the employer. Once the probationary period is over, one receives the status “civil servant for life.”

Civil servants for life are fortunate. They can hardly be dismissed. Their job is secure for life. That means they receive their salary every month until the end of their life. Such security is usually not found in the private sector.

The same applies to public-sector employees who have been employed for more than five years. Their jobs are also secure for the rest of their lives. After these five years they can no longer be dismissed. These employees are referred to in administrative jargon as “non-terminable public-sector employees.”

Non-terminable public-sector employees

Who exactly is employed in the public service? Who are the employers? Primarily, public-service employees work for the federal government, the federal states, municipalities and communities. Foundations and public institutions are also considered employers. Public broadcasters such as ARD, ZDF and the so-called regional third programmes are part of the public service. Those working in schools, state-run kindergartens or welfare associations can also apply for a civil-servant loan under the given conditions. The same applies to non-terminable employees at public utilities and transport companies — buses and trains — provided they are not privately operated. Also included are: chambers of commerce and industry, public housing companies, the German Pension Insurance, chambers of crafts, professional associations, associations of statutory health insurance physicians and the Federal Agency for Technical Relief (Technisches Hilfswerk), for example.

A civil-servant loan is therefore granted to those who hold the status of civil servant for life and to “non-terminable public-sector employees.”

Those who are civil servants on a revocable basis or on probation should still inquire about a corresponding loan. Exceptions confirm the rule. Sometimes these civil servants are also granted a civil-servant loan. It depends on the individual situation. They should not hesitate to ask about the special conditions of civil-servant loans and civil-servant credit.

Things are more difficult for “civil servants for a fixed term.” Honorary mayors, district administrators, or deputy officials are, for example, positions that only last a few years. Whether and when this group can apply for a civil-servant loan depends on the individual case.

Why do civil servants receive such favorable loans?

Everything costs money. Borrowing money also costs. You have to pay interest on a certain loan amount. What determines the amount of this fee? Everyone has probably heard: nominal interest rate (Sollzins) and annual percentage rate (effective annual interest rate).

What are nominal interest rate and effective annual interest rate? How do the two rates differ?

The nominal interest rate indicates the amount of interest to be paid for an installment loan. It is calculated individually for each loan. Various conditions feed into the calculation of the nominal rate. How is the general interest level currently on the credit market? How solvent is the borrower? How good is his creditworthiness? The personal Schufa score is considered, among other factors. How high is the risk that the loan cannot be repaid? How large is the loan amount and how long will it take to repay the installment loan? All of this determines the interest rate for a civil-servant loan as well. In addition, banks and other lenders include certain fees in the interest. These can be processing fees. Sometimes account management costs are charged. The result is the effective annual interest rate. It shows what the loan really costs per year.

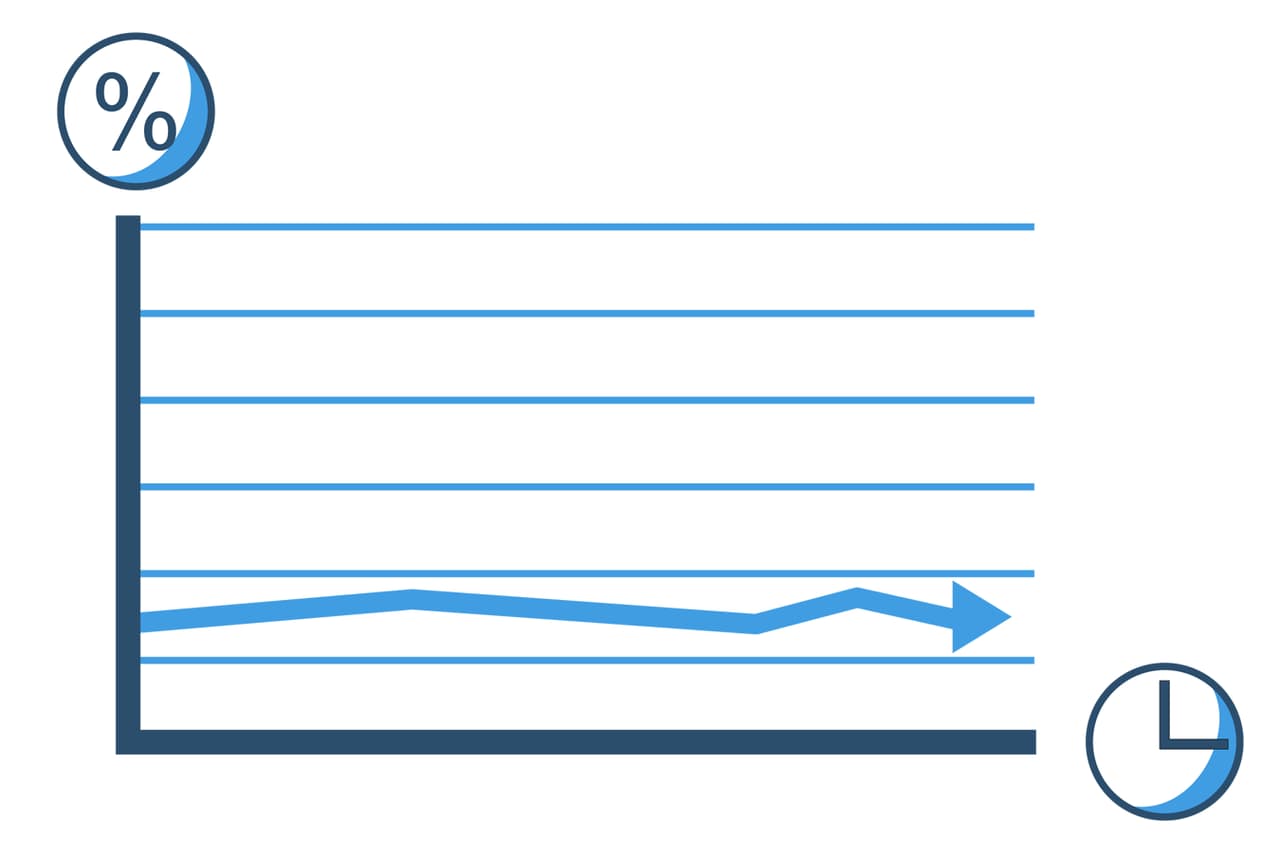

Interest rate for the civil-servant loan

The interest rate for a civil-servant loan is very stable and low over the long term. Why is that? Because the risk to banks that the loan cannot be repaid is very low for civil servants. For other loans, the probability that someone will lose their job is factored in. This aspect is almost entirely eliminated for civil-servant loans. Moreover, civil servants are generally very solvent because of their regular, stable income. Loans can be serviced with lower monthly amounts over a long period. Lenders can be confident that borrowers will meet their payment obligations and that installments will not suddenly stop. The risk of loan default for banks and other lenders is therefore minimal. They pass on the lower risk and costs in the form of favorable interest rates to the borrower.

What requirements apply to a civil-servant loan?

This time the new car can be a bit sportier. Have you already chosen one? The wide, white sandy beach is calling for the well-deserved holiday? Before applying for the civil-servant credit to fulfill these dreams, you should check whether all requirements are actually met.

Anyone who wants to borrow money must be of legal age and have a regular income. That is a basic prerequisite for borrowers. To be precise, you must not be too young or too old to benefit from a civil-servant loan. That means: be over 18 but under 60 years old as a borrower. Contracts with the lender and the insurance usually run for more than ten years. Providers want to ensure that payments will be made during this period. The risk of default increases with age. And you must be healthy. Insurers sometimes require a health check or a certificate from a doctor. It is usually also necessary to live in Germany — i.e., to be registered with your primary residence in Germany. Another requirement for approval of a civil-servant loan is to have a checking account. The current account is necessary so that the loan amount can be transferred once the loan is approved. Monthly repayment installments are also debited from this account.

In addition, the status “civil servant for life” or “non-terminable public-sector employee” is a prerequisite for a civil-servant loan. The applicant should already hold this status when applying, as it is decisive for approval of the civil-servant loan.

Negative Schufa entries make it difficult for the applicant. Has a loan already been terminated? Is there an affidavit of means? Is there ongoing insolvency or has a procedure been initiated? Has the salary already been garnished? All these cases negatively affect the personal Schufa score. The information from Schufa — or another scoring agency — is usually always included in the approval decision for a loan.

Are there already loans outstanding? Existing financings must be checked and may need to be repaid first with the new civil-servant loan. Is there already an assignment of wages for another loan? For a civil-servant loan, a first-ranking assignment of wages is necessary. Wage and salary assignments are securities for lenders. Parts of income can be garnished directly if the borrower does not meet payment obligations punctually and regularly. Are existing loans secured in this way? Then they must be settled before a civil-servant loan can be taken out. Exceptions confirm the rule here as well. Purpose-bound financings such as mortgage loans, i.e., building financing and car loans, as well as vehicle leasing contracts, remain in place.

Is a possible official misconduct being checked or has it been? A disciplinary procedure also makes it almost impossible to obtain a civil-servant credit.

Furthermore, the amount of the monthly installments must be designed so that, in the worst case, this amount can be garnished. The installment amount should therefore not exceed 15 percent of gross salary.

Requirements for civil-servant loans in brief:

- Legal age

- regular income

- younger than 60 years

- positive Schufa score

- civil servant for life or non-terminable public-sector employee

- no prior wage assignments

- no garnishments

- no disciplinary proceedings

- health check

What securities are necessary for a civil-servant loan or a civil-servant credit?

Civil servants are considered trustworthy because of their position and status. Nevertheless, lending banks must secure themselves against sudden non-payment. Even with a civil-servant loan, it is extensively checked whether the loan can be repaid. A query is therefore usually made to the Schutzgemeinschaft für allgemeine Kreditsicherung (Schufa). For other loans a guarantor may have to be named or the car title transferred to the bank. That is not necessary with a civil-servant credit. The life insurance taken out and an assignment of wages function as security here. The lender receives the rights and claims of the life insurance up to the amount of the loan. If the job changes, this must be reported to the lender immediately and the new employer must be named.

Which documents are required to process the loan application?

To apply for a civil-servant credit you don’t need much. A copy of the latest payslip must be attached to the loan application. If married, include the spouse’s most recent payslip as well. In addition, the civil-servant status “civil servant for life” must be evidenced by the appointment certificate or a copy of it. “Non-terminable public-sector employees” also need proof of this status. And of course the loan application should not be forgotten. Then the loan inquiry and the review of whether a loan will be approved can begin.

What is the maximum amount I can receive with a civil-servant loan?

Everyone secures themselves. The advantage for lenders with a civil-servant credit is that the usual default risks largely disappear for civil servants. The job is not at risk. The employer does not go bankrupt. Even in case of illness the relatively low installments can usually still be paid. The worst-case risk can additionally be insured with a term life insurance. Therefore banks and lenders grant higher loan amounts with a civil-servant credit than with other loan types. They still need to secure themselves, though. In the case of a civil-servant loan, a loan amount equal to 20–25 times the net income is generally granted. So if someone receives €2,000 net per month from their employer, they can borrow up to €50,000. Someone with €3,000 net per month can request a loan of €75,000. What the money is used for is entirely up to the borrower.

What can a civil-servant loan be used for?

My house, my car, my horse — a civil-servant loan makes all of that possible. A new apartment set? A swimming pond in the garden? A wedding with 200 guests? No matter what the money is needed for or desired for, the purpose can be completely free with a civil-servant loan. Isn’t that always the case with a loan? No, that depends entirely on the loan type. There are also purpose-bound personal loans. That is the case with car loans or real estate purchases. The car serves as collateral for banks, as does the house or apartment. Lenders therefore often offer more favorable conditions for these loans than for an ordinary installment loan. The downside is obvious: the money cannot be used flexibly. If you suddenly need a specific sum for something else, it is not available through the car or mortgage loan.

New car or dream holiday

The dream holiday to the Caribbean has been booked for weeks. White beaches, warming sun, clear water — after a lot of stress in recent months, pure relaxation is deserved. The whole family should have the best weeks of the year. And then the car breaks down unexpectedly. Now the repair bill threatens to ruin the vacation plans.

Sometimes everything just happens at once. These are things you couldn’t have planned in advance. Suddenly the roof is leaking. There’s actually a worm — literally — in the rafters. Rotten boards and sawdust traces indicate woodworms have made themselves comfortable in the roof. Or cracks appear in the supporting beams? Suddenly the holiday might be in jeopardy. Or not. If you borrow money via a civil-servant loan, you can decide completely freely what it is used for. No holiday planned? But a new car is okay? For civil servants financing via a civil-servant credit is a low-interest alternative to a car loan. Whether you want a new car or a used one, a car loan can also be taken out in the form of a civil-servant loan.

Debt consolidation — get rid of expensive interest with a civil-servant loan

If you have taken out multiple loans, you may sometimes find after a while that it’s hard to keep track of everything. Why are monthly payments suddenly higher than expected? Have the interest rates risen again? With a civil-servant credit you can get your finances in order. The magic word is debt consolidation. Why pay more than necessary? If a new loan offers better conditions than an existing loan with high interest, it makes sense to repay the old financing before the agreed term ends. One loan takes over the functions of another — but with better conditions. Because a civil-servant loan is not tied to a specific use, it is well suited for debt consolidation. There are two options: the borrower opts for a lower monthly installment, which gives financial leeway. Or they keep the installment level the same, which shortens the term and lets the loan be repaid faster.

Personal loan or civil-servant credit?

Anyone who wants to build a private house knows that architects, structural engineers and developers don’t work for pocket money. Not everyone has the necessary cash for a new car lying around. A new apartment needs furnishing? Then you suddenly need more money. For all of this and much more you can apply for a personal loan. The borrowed loan amount is repaid in monthly installments. Interest is charged for the provision. So what is the difference to a civil-servant credit? A civil-servant loan is also a form of personal loan. It is granted to private individuals for purchases, with the special case that these people are employed in the civil service — i.e., civil servants for life or non-terminable public-sector employees.

The clearest difference between a normal installment loan for a private person and a civil-servant credit is the restricted group of people who receive these loans. The personal loan also differs from the civil-servant credit through special conditions such as higher loan amounts, longer terms and lower installments and interest rates.

Schufa report for civil-servant loans

Is a Schufa report necessary for a civil-servant loan?

Who hasn’t lent a book and not gotten it back? That’s always annoying. If you lend something you want to be sure you get it back. That applies even more when it’s about money. Lenders want to be sure they will get their money back. Banks must also check whether a loan can be repaid.

The advantage in the private sector is: you usually know the person you lend something to and you expect them to handle it carefully. Lenders do not have such information. Personal loans are not approved without a report from the Schutzgemeinschaft für allgemeine Kreditsicherung (Schufa). Although a civil-servant loan is relatively secure due to the civil-servant status, the status alone does not say how the person handles borrowed money. That is why lenders also query the Schufa score for a civil-servant loan. The Schufa report provides a picture of the applicant’s creditworthiness. But it is only one of several pieces of information used to decide on the grant of a loan.

The Schutzgemeinschaft für allgemeine Kreditsicherung is a private credit bureau. It collects, stores and evaluates data on the payment behavior of private individuals and companies. Schufa receives information, for example, when a leasing contract is concluded. Are purchases paid in installments? The purchase of a smartphone and the conclusion of a new mobile phone contract are also recorded at Schufa. Entries from electricity providers, online retailers and insurers are listed as well. Lenders access this information when they want to know whether the person applying for a loan can repay it. Have loans always been repaid reliably? Were installments paid on time? Were invoices and leasing rates always paid? All of this influences the personal score. The higher this value, the better the creditworthiness. The easier it is to get a loan approved. The Schufa score is calculated from Schufa entries, statistical surveys and industry-specific experience.

Can I get a civil-servant credit with a negative Schufa?

Life sometimes doesn’t go as planned. Sometimes everything gets on top of you. Bills pile up — reminders too. Suddenly the postman hands over an enforcement order. One or two late payments don’t lower the Schufa score much. Enforcement orders that become legally effective do. That significantly reduces the borrower’s creditworthiness. If you merely want to gather information and submit inquiries to various providers, you’ll also notice: that’s bad, it lowers the score. It’s better to compare conditions only. This does not negatively affect creditworthiness.

Is the Schufa score negative? Don’t worry. The Schufa report is only one criterion used for approval of the civil-servant loan. It is not the only one. Decisions are always made on a case-by-case basis. Lenders look at the borrower’s entire financial situation. What are the reasons for the poor score? How large is the requested loan? How did the poor score come about?

Additional securities that can be presented — such as a life insurance policy or ownership of a house or apartment — have a positive effect. Then lenders often permit financing despite a negative Schufa entry. Important: anyone who has had problems making monthly payments reliably should clarify and resolve the reasons for that beforehand. Because monthly repayment amounts for a civil-servant loan must also be paid on time. If not, a new Schufa entry may result.

Is there a civil-servant credit without Schufa?

Prejudices form quickly and can persist for years. “Loans without Schufa are dubious. They only come from loan sharks with very high interest rates.” If that sounds familiar, you can rest easy. Those times are long gone. Civil-servant credits without Schufa are now common practice and accepted. Even for a civil-servant loan it is carefully checked whether it can be repaid. For that we already query Schufa. But what about a loan without Schufa? Yes — for a loan without Schufa the approved loan is not registered with Schufa. Why is that good? A poor Schufa score can arise quicker than you think. Were leasing installments not paid? Overdrawn checking accounts? A missed phone bill? It happens fast. And the Schufa score can deteriorate significantly. The good thing is: these entries are deleted after a certain period. Every new personal loan prolongs this entry. A loan that is not recorded with Schufa helps the account recover. That is important, for example, if a house construction or purchase is planned and a higher loan amount is needed. By contrast, small loans without Schufa are common and easy to obtain for civil servants for life and non-terminable public-sector employees. Foreign banks find sufficient security in the job stability. Such a small loan is therefore not recorded at Schufa. In addition, Swiss and Liechtenstein lenders refrain from querying Schufa. They approve loan amounts quickly and unbureaucratically.

A civil-servant credit without Schufa therefore helps the Schufa account to recover.

Where does the money for the civil-servant credit without Schufa come from?

For loans without a Schufa entry, Maxda works with foreign banks. Banks in Switzerland and Liechtenstein do not have to follow German guidelines. For civil servants this means: they do not need a guarantor, collateral or the spouse’s signature. Why? Swiss banks are satisfied that civil servants have a secure and usually good income. As written proof they usually require the last three payslips. The civil-servant credit without Schufa is popular when you suddenly and unexpectedly need money in the short term. Lenders and intermediaries act quickly. From application to disbursement it can take only a few days. Then the money is in the applicant’s account. However, interest rates for loans without Schufa are often somewhat higher than for loans where the Schufa score information was obtained. Overall, civil-servant credit and civil-servant loan remain very affordable financing options for this professional group due to their special conditions.

The civil-servant loan as a loan without Schufa from Maxda

The satisfaction of our customers is our capital. We don’t want customers to feel bound by repayments and constrained until the end of the term. Especially not with a civil-servant loan. Variable special repayments can of course be made free of charge. If you are on sick leave longer than expected and temporarily receive less money, simply talk to us. We always find a way and a solution. Together with our customers.

How is repayment handled with a civil-servant loan?

With a civil-servant loan an agreed amount is debited monthly from the account. This is split into two parts: the repayment installment goes to the insurer to fund the whole life insurance. The interest, which results from the loan amount and other conditions, is paid to the lender. These remain the same for the agreed repayment period.

If, for example, you suddenly win the lottery or inherit money, you can improve the loan conditions with special repayments or repay the personal loan early. The surplus in the life insurance would then be paid out to the borrower at the end of the loan term.

When will I receive the loan approval?

If you plan to build a house or acquire property, you can foresee in the long term that you will need money. If something intervenes that throws your finances out of balance, you need quick support. We process inquiries quickly. We check complete documents that are legible and correctly filled in online within 2–4 days. An offer is then prepared. If the borrower reviews and returns it promptly, the loan amount is transferred to the account in a very short time.

What do I need to do to apply for a civil-servant loan without Schufa?

The Maxda civil-servant loan is very easy to apply for online. Just click on Loan Inquiry on the homepage or go to this page: https://www.maxda.de/anfrage. Fill in the online form. Click submit and it’s off. We check the information and which offer from our domestic and foreign banking partners is best. What happens next? We send the civil-servant loan offer to the borrower for review. If everything fits, the application can be submitted immediately afterward. Processing takes a few days so that money for an approved loan without Schufa can be on its way to the customer shortly after approval. zurückzuführen ist.