Equity

The term equity is used in various situations. It is particularly important in connection with accounting and the financing of companies. In addition, the word equity is also used when private individuals take out financing for real estate. This article will explain the different meanings of equity in more detail. It will also describe the most important functions of equity and its relationship to other decisive factors.

What is equity?

At first glance equity may seem self-explanatory, as it actually describes the portion of a financing that the borrower covers with their own funds. Nevertheless, a distinction must be made here between the meaning in corporate accounting and the use of the term in construction financing:

1. Equity as an item in a company's balance sheet

In this context the term equity describes the difference between a company's assets and liabilities. It is the only balance sheet item that cannot be measured directly but is determined as a residual figure. Very simplified, a company's balance sheet looks as follows:

Balance sheet of company XY as of 31.12.20xx

| Assets (sources of funds) | Liabilities (uses of funds) |

|---|---|

| Fixed assets (e.g. land, machinery, vehicles, licenses and patents, investments) | Equity (net assets) |

| Current assets (e.g. inventory, receivables, securities, cash) | Debt (e.g. bank loans, trade credit, provisions, other liabilities) |

| Total assets | Total assets |

When preparing the balance sheet, all items except equity can be determined exactly in advance and entered in the balance sheet. Since the totals on both sides of the balance sheet must be equal, equity is the residual between the assets on the asset side and the liabilities (debt) on the other side.

Note: If a company's equity is negative, it is reported on the asset side. In this case the company's debts exceed its assets. For corporations, negative equity normally triggers insolvency due to over-indebtedness.

How does equity arise in a company?

When a company is founded, the shareholders contribute equity in the form of cash contributions or contributions in kind. Contributions in kind can be, for example, real estate or land. The legislator prescribes a certain minimum capital for corporations.

Public limited company (AG): minimum capital €50,000 (§7 Aktiengesetz)

Limited liability company (GmbH): minimum capital €25,000 (§5 GmbH-Gesetz)

In addition, a company has other ways to increase equity:

- Capital increase: More capital is made available by shareholders and investors. This can be achieved either by increasing contributions from existing shareholders or by gaining new shareholders. In many cases existing shareholders of an AG have a pre-emptive right (subscription right) to buy new shares to maintain their stake.

- Retention of profits: Part of the annual surplus is retained and recorded in profit reserves.

- Capitalization of assets: New assets are capitalized. This can occur not only through an asset swap (cash for assets = purchase) but also through a contribution by a shareholder. Furthermore, valuation options can be exercised and self-created intangible assets or low-value assets can be capitalized.

- Revaluation of assets or liabilities: By exercising valuation options, assets may be valued higher or certain types of liabilities lower depending on the situation. This also affects equity.

What components make up equity in companies?

A company's equity in the balance sheet consists of various sub-areas. These components are explained in more detail below:

Subscribed capital

Subscribed capital is the part of equity for which the liability of the shareholders of a corporation is limited. The rules regarding minimum capital at formation apply to equity. In normal cases subscribed capital is formed by shareholders' payments and later capital increases. An increase from company funds is also possible. The term "subscribed capital" is named differently depending on the legal form:

- Registered capital (AG)

- Share capital (GmbH)

- Limited partner capital (KGaA)

- Business deposits (eG)

Capital reserves

Capital reserves are part of the legal reserves and, according to §272 para. 2 HGB, consist only of the following items:

- Premiums from the issuance of equity interests (both shares and bonds, convertible bonds and options)

- Amounts from additional payments by shareholders in return for preferential rights

- Other additional payments by shareholders

Profit reserves

Profit reserves are formed from undistributed annual surpluses and can be divided into the following areas:

- Statutory reserve: Public limited companies and partnerships limited by shares must build up this reserve for the protection of creditors. To this end, 5% of the annual surplus (reduced by prior-year losses) must be transferred to the profit reserve each year until it, together with the capital reserve, amounts to 10% of the registered capital.

- Reserve for "shares in a controlling or majority-owned company": This reserve is the counterpart to the shares on the asset side. If the shares in such a company are sold, the reserve must be released accordingly.

- Statutory reserves: If the articles of association of a public limited company provide for the creation of further reserves, these can be formed.

- Other profit reserves: Residual amounts not covered by the other types of reserves.

Retained earnings

Since profits must not directly affect the subscribed capital of a corporation, retained earnings serve as a variable equity account. If an unused profit is reported, retained earnings ensure that the next fiscal year starts with a profit.

Accumulated loss

This is the counterpart to retained earnings. If an annual loss is not offset by equity or shareholder payments, the accumulated loss can be carried forward to the following year under certain conditions. It may then be offset against profits from subsequent years.

Net profit

Net profit is a residual item of equity that remains after offsetting the annual surplus with retained earnings and accumulated losses, withdrawals, and capital and profit reserves. The net profit is paid out to shareholders or investors as a dividend.

What are the differences between equity and debt?

At first glance, the distinction between equity and debt may seem simple. In practice, however, this is not always easy. There are, however, some characteristics typically associated with the two types of capital:

Equity:

- Repayment can depend on the company's success

- Return depends on the company's performance

- Equity often brings a say in the company's affairs

- In insolvency, equity is used to settle the company's liabilities

Debt:

- Mandatory repayment obligation

- Return is independent of success and agreed in advance

- In insolvency, debt is repaid partially or fully depending on the available insolvency estate

While the distinction is clear in cases of shareholder contributions (equity) and bank loans (debt), there are hybrid cases. Such capital types are called mezzanine capital, which is partly classified as equity and partly as debt. These include:

- Hybrid bonds (very long maturities, subordinated in insolvency)

- Loans from shareholders (technically debt, but subordinated in insolvency)

- Contributions from silent partners (more like debt, though loss participation can be included)

- Subordinated loans (debt but subordinated in insolvency)

- Participation rights (very different depending on the individual case)

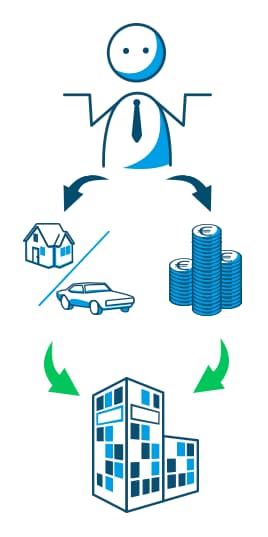

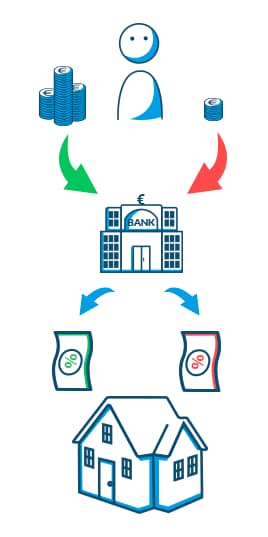

2. Equity in construction financing

The definition of equity in construction financing is much easier to grasp. It simply refers to the borrower's own share of the costs for purchasing or building a property. A simple example illustrates this:

Purchase price of a property = €200,000

Equity = €50,000

Loan amount = €150,000

Equity share = 25%

Equity in construction financing - what to consider?

In construction financing, equity that borrowers can contribute is always one of the important parameters alongside other factors. For laypeople this topic raises many questions, which are answered below:

Why is equity important in construction financing?

Anyone who wants to buy or build a property usually needs construction financing. Because construction loans often involve very large sums and long terms, banks and other lenders require appropriate collateral for granting the loan. This collateral is intended to ensure that the lender does not have to write off the lent money in case of payment difficulties. If this situation occurs, the collateral is realized and the bank recovers a large part of the outstanding amount. The main collateral in construction financing is the property itself. It represents an asset and is secured by a land charge. To illustrate the importance of equity in construction financing, the collateralization process must first be explained in more detail. The current purchase price of a property is the so-called market value. Because this fluctuates and depends on current market conditions, it is not used as the basis for the level of collateral. Instead, banks focus on other measures:

- Lending value (Beleihungswert): The lending value represents the value that can be achieved permanently through a resale of the property, independent of short-term fluctuations. Depending on the case, this is between 75% and 90% of the purchase price and represents the absolute upper limit of the lending.

- Loan-to-value ratio (Beleihungsauslauf): The loan-to-value ratio is a quotient indicating the actual lending in relation to the lending value. The calculation is as follows:

- Loan-to-value ratio = (loan amount + prior charges) / lending value A conventional construction financing normally starts at a loan-to-value ratio of 60–80%. Of course there are also construction financings without equity where 100% and more of the loan-to-value ratio are chosen. These are only possible and interesting in exceptional cases.

Without equity, it may be that construction financing is not possible at all or only on very poor terms.

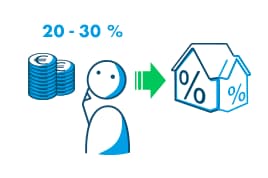

How much equity should you contribute to construction financing?

In general, it can be said that you can never have too much equity for construction financing. A high equity share has several effects:

- Lower interest rates

- Shorter term and lower loan amount

In practice, an equity share of 20–30% of the purchase price has proven to be very reasonable. This allows for favorable interest rates and tailored construction financing.

What counts as equity in construction financing?

Equity in the sense of construction financing primarily consists of cash funds with which borrowers can already pay part of the purchase price. This reduces the loan amount for the property and improves the lending situation. In addition, own labor can also be recognized as equity. This is particularly the case when building a house. Interesting areas for own labor include:

| Own labor | Requirement | Potential savings |

|---|---|---|

| Wallpapering / painting | Although these tasks require some skill, they can be done satisfactorily without professional training. | €3,000 - €4,000 |

| Thermal insulation | Some knowledge is required, but the work can also be carried out by skilled DIYers. | €5,000 - €6,000 |

| Interior door installation | Interior door frames and doors can also be installed by the owner. | €3,000 |

As a rule, banks recognize own labor as equity up to 15% in construction financing. Nevertheless, equity cannot be completely replaced by own labor, but at best supplemented. Own labor also has other disadvantages:

- No warranty from professionals

- No insurance coverage for amateur work

- High time expenditure alongside regular employment

Does the amount of equity affect the interest rate of construction financing?

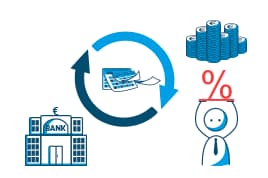

Interest rates for a construction loan depend on numerous factors. Equity, however, is one of the biggest influencing factors on mortgage rates. As explained, the security for a property loan is achieved by the lending on the property. By registering a land charge in the land register, a bank could recover a significant portion of the outstanding amount through foreclosure in the event of borrower default. This leads to the following relationships:

More equity ? Lower lending ? Better collateral for the loan ? Lower default risk for the bank ? Lower interest rates for the construction loan

Banks typically reward a lower default risk with more favorable interest rates. Thus the terms of a financing can often be significantly improved by contributing one's own funds.

Construction financing without equity - is that possible?

Although 20–30% equity is usually considered the basis for property financing, there are special financing options. Construction financing without equity can be divided into two categories:

- 100% financing: The full purchase price of a property is financed by a bank. Incidental costs such as real estate transfer tax, notary fees and broker fees are paid from own funds.

- Full financing: Full financing covers the entire purchase price as well as the incidental costs of acquiring the property.

What requirements must the borrower meet for construction financing without equity?

Since the lending on the property in construction financing without equity considerably exceeds the lending value as an upper limit, it is a very risky financing. For this reason borrowers must meet special requirements to be able to use such a loan:

- Special creditworthiness: While a flawless SCHUFA report is almost a prerequisite, the borrower's scoring value should also be as good as possible.

- High and secure income: Because the loan amount is very high without equity, borrowers must be able to carry high repayment amounts with their income. A certain income security is also very important.

- Location and condition of the property: The desired property should be in an up-and-coming location and in good condition. Otherwise devaluations may occur during the term and the entire financing may be jeopardized.

Do you have to pay a higher interest rate for property financing without equity?

The lack of equity in a full financing is a clear disadvantage in terms of collateral. Higher risk for banks is usually associated with poorer conditions. Thus borrowers must expect a higher interest rate for construction financing without equity.

When is construction financing without equity sensible?

The essential characteristics of construction financing mean that it is by no means affordable or attractive for every borrower:

- Longer term

- Higher loan amount

- Greater debt risk in case of default

This is illustrated by an example:

The purchase of a property for €220,000 is financed once with 30% equity and once completely without equity. The fixed nominal interest rate in the first case is 2.50% and in the second case 4.00%. This results in the following parameters:

| Loan A (30% equity) | Loan B (no equity) | |

|---|---|---|

| Loan amount | €154,000 | €220,000 |

| Fixed nominal interest rate | 2.50% p.a. | 4.00% p.a. |

| Initial repayment | 3% | 3% |

| Monthly payment | €705.83 | €1,283.33 |

| Term | 15 years | 15 years |

| Total interest costs | €43,072 | €95,650 |

| Outstanding balance after 15 years | €70,022 | €84,650 |

| Difference (interest costs) | €52,578 |

Construction financing without equity results in a higher monthly repayment rate, higher interest costs and a higher outstanding balance after the fixed-rate period. Therefore it is only suitable for the following groups:

- Young and high-earning individuals who can afford high repayment rates.

- Civil servants in higher positions with correspondingly high incomes.

- People with invested assets that yield a higher return than the mortgage interest.

Those willing to take a high risk and repay quickly may be well suited for construction financing without equity. However, even small income setbacks can lead to payment difficulties and, due to the lack of equity, a foreclosure may end with proceeds lower than the outstanding debts. Affected parties would lose the property and still have to repay a residual amount to the bank.

Equity - A short conclusion

Equity is an important metric for companies and also in property financing. In the business sense it describes the difference between assets and liabilities on a balance sheet. The equity ratio indicates the share of equity in total capital. In construction financing the principle remains the same, but here it only refers to the share of own funds in the total financing costs. The higher the equity, the easier it is for borrowers to obtain a loan to build or buy a property. In addition, equity also has a favorable effect on the interest rate for a loan.