The Discount Loan

When you buy a product, you usually pay immediately. That's how it normally works. But not always. Companies order goods or services and pay later. Businesses use these payment terms. Whoever grants a due date on an issued invoice is effectively granting credit for that period. There are different ways to do this and different bank loans. The discount loan is one of them.

What is a discount loan?

As with a cheque, a sum to be paid is written on a credit paper. This is called a bill (Wechsel), and it also specifies a particular day on which that amount must be paid.

This credit document is of interest to companies as short-term financing.

The discount loan is also commonly known as a bill (or bill of exchange) credit.

According to business dictionaries, a discount loan refers to a short-term loan in which a credit institution purchases from the borrower a bill that is due at a later date.

Explained with a small example:

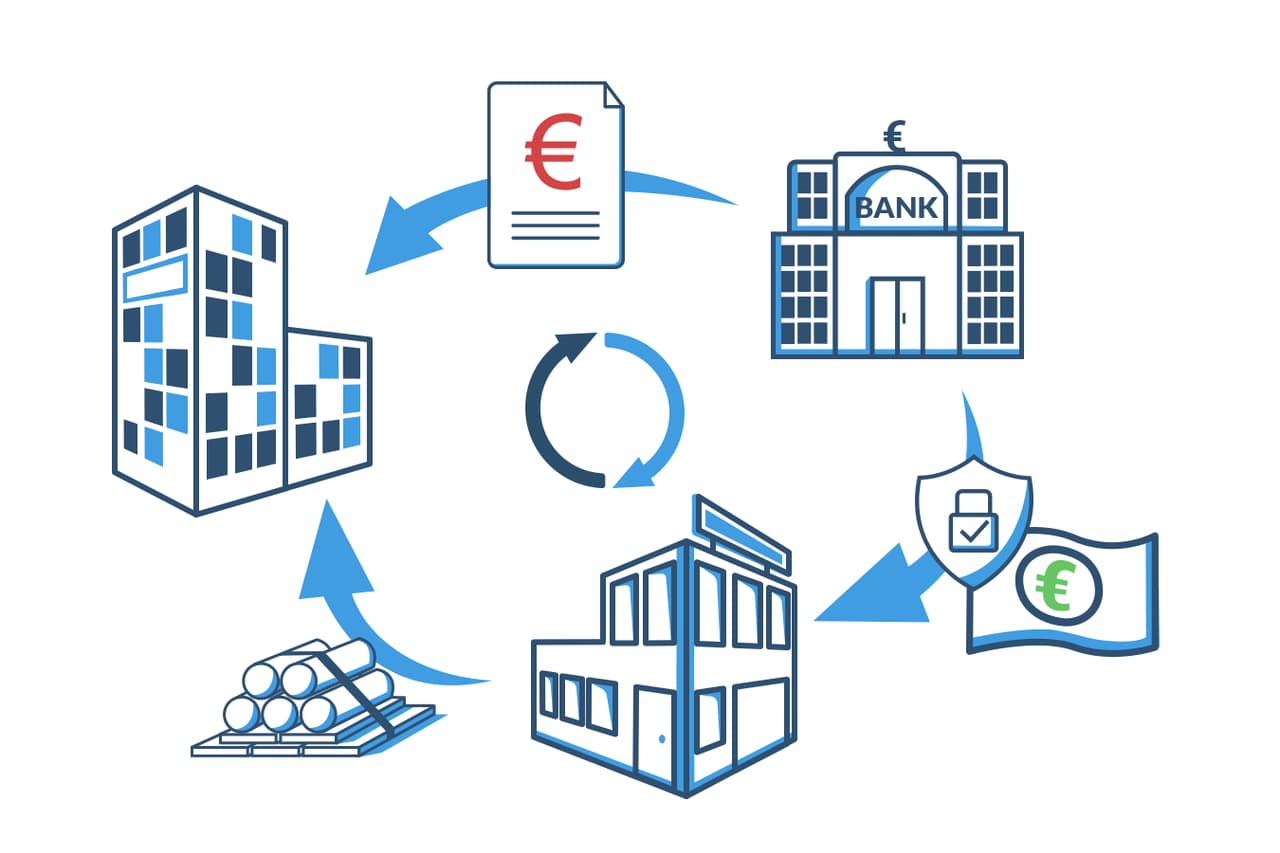

A pet supplies shop orders 20 pallets of cat food from a manufacturer. The shop does not want to pay for the goods immediately but at a later date. The manufacturer agrees if, in return, the shop issues a bill of exchange. The bill states when the manufacturer must pay the shop for the 20 pallets of cat food. The shop can wait until the customer pays. Or it can sell the bill to a bank or credit institution. For receiving the money immediately, the bank charges the shop part of the total amount as interest. In other words, the shop does not receive the full original sum.

The loan the shop obtains from the bank in this way is called a discount loan. The credit institution in turn obtains favourable bank financing from the Bundesbank at the "discount rate".

When the date comes on which the manufacturer of the cat food must pay the invoice, the bill amount becomes due. The cat food producer pays the entire sum to the bank or credit institution.

So: a company (B) supplies its customer (A) with goods or a service. As security that the goods will be paid for at a later date, A issues a bill of exchange that B receives. B passes this bill on to the bank (C) and receives the money immediately, minus the interest the bank charges for lending the funds.

A discount loan is a way to finance something on a short-term basis. Companies often use this form of loan as an alternative to a business loan.

How high are the interest charges a credit institution demands for providing this bank loan? The discount rate is oriented to the current interest level on the money and capital markets. The economic situation of the credit institution is also taken into account. In addition, the quality and number of the submitted bills play a role.

Discount loan - explained briefly

- A discount loan is a loan in which a third party, a bank or credit institution, takes a bill of exchange into payment.

- The bill is a credit paper that states the amount one person A (or a company) must pay to another person B (or a company) at a specific time.

- The bank or credit institution pays the money before that date to person B. For this it charges interest. B therefore does not receive part of the bill amount. The bank then receives the original full amount from person A at the agreed time.

How does a discount loan work?

Credit institutions only grant discount loans to customers who have previously signed a corresponding agreement. This contract sets the so-called discount credit line. It determines the amount, the maximum discount credit volume, for the borrower. This can be used on a revolving basis. That means the two contracting parties set a certain upper limit for an amount that can be repaid and borrowed again within a certain period.

If you want to receive a discount loan, you must consider some points:

The issued bill is a so-called commercial bill (Handelswechsel). Whoever orders goods or receives a service and does not want to pay immediately can issue a bill as security for the delayed payment, the commercial bill. In addition to the commercial bill, there is the financial bill (Finanzwechsel). No goods, products or services are sold here. This bill is similar to a cheque that a borrower can present to a bank and receive money for. The credit institution charges interest for this, the discount.

- The bill must be paid (presented for payment) no later than three months after issuance.

- The issuer and the recipient of the bill must be creditworthy.

- All formalities must be correctly fulfilled.

- The bill must be payable "at a banking place". That means a location where a branch of the Bundesbank exists.

The discount loan is a loan between the one who needs credit and the credit institution. The bank pays the bill amount to the borrower, minus interest and fees. It then waits until the one who must settle the bill pays the money. Or it passes the bill on to the Deutsche Bundesbank. It sells it. In this way the bank obtains the value of the bill in advance. Until 1999 banks could also resell the bill to the European Central Bank. Since then the European Central Bank no longer rediscouns bills.

Who is a discount loan suitable for?

The discount loan for companies

Companies like to use the discount loan to bridge liquidity shortfalls. These often occur when invoices, for example for ordered goods, are due while it is clear that services rendered or delivered goods will only be paid for later. The bill credit is suitable to resolve this discrepancy. It enables companies to pay their own debts or outstanding invoices on time.

The discount loan for freelancers & self-employed

Most self-employed people and freelancers know what it means when a customer does not pay on time. This can easily trigger a cycle in which you yourself cannot pay your invoices on time. The discount loan helps to give these customers leeway and thus remain solvent. In addition, banks grant loans to the self-employed much less often than to others. The discount loan, because of the security provided by the bill, offers a way to borrow money short-term. Since the parties involved are personally liable, the bank is very confident it will get its money back. Therefore it often approves this loan more easily and quickly.

Advantages & disadvantages of a discount loan

What are the advantages of a discount loan?

Do you need money quickly? Are invoices due but the necessary funds are currently lacking? Which entrepreneur does not know this: a shortfall can appear very quickly. A customer fails to pay an invoice on time and you yourself find it difficult to pay your own invoices punctually. To obtain money quickly and at short notice, the discount loan is suitable. Since the bill represents considerable security for credit institutions, this loan is granted easily and quickly. The bill participants are fully and personally liable. That means the bank can be confident it will get its money back. In addition, lenders have little effort with the discount loan. The formalities are usually handled quickly. Credit institutions themselves obtain favourable bank loans from the Bundesbank at the discount rate. Therefore the interest charged for the loan is not as high as for other loans. Discount loans are not registered with Schufa. So they are inexpensive for anyone who wants to finance a certain amount in the short term but does not want an additional entry in Schufa for a later loan. For example, because a larger bank loan is already planned for which a positive Schufa score is important.

Advantages of the discount loan - short and sweet:

- inexpensive loan for companies

- high flexibility

- quick access to funds

- low administrative effort for banks

- high security for banks, therefore easier approval

- no entry in Schufa

What are the disadvantages of the discount loan?

It is legally prescribed which elements a bill must contain: the document must include the word "bill" (Wechsel). It is followed by a clear description, rather an instruction, that a certain sum of money is to be paid by one person to another at a fixed time. The names must be stated. It is determined where the bill is to be paid. When was the bill issued? By whom was the bill issued? And where was the bill issued? These details are also required. Banks place great importance on compliance with all formalities. Missing information easily leads to the discount loan not being approved. In addition, each bill must be approved anew. It is not enough to have concluded a corresponding contract with the bank. However, such a contract is a prerequisite for the discount loan to be permitted at all. Some lenders charge high fees for processing.

Important to know: Both parties involved—the issuer and the bill holder—are fully and personally liable. On the agreed due date the money must be repaid. Typically the maximum time is three months until the bill must be presented for payment. If the bill is still outstanding on the due date, the bank can also recover the money from the customer.

Disadvantages of the discount loan - short and sweet

- complex handling

- each new bill must be approved by the bank

- high, immediate liability if not paid on the due date

- sometimes high mark-ups and fees at some credit institutions

- a corresponding contract with the bank must be concluded in advance

What costs arise from a discount loan?

A discount loan is a very inexpensive loan. Interest and fees for the loan amount are covered by part of the claim.

Have seller and buyer agreed that the purchased goods will be paid not in cash but by bill of exchange? Excellent. The buyer usually bears the cost of the bill. This is taken into account in the price and accordingly added to the original amount.

The discount—the difference amount—is calculated based on the term. It concerns the period between the day the bill is issued and the day it becomes due. How many days are granted until the issued amount is due on the due date? Most often this is 90 days, i.e. three months. The month is calculated as 30 days for the purpose of calculation. A bill can only be presented for payment on a working day. Therefore the interest period can be a little longer than the stated date.

Interest is calculated using the commercial interest formula. The discount is scaled up from the repayment amount of the loan. As a result, the effective interest rate can be higher than for a loan that is calculated annually. Since the terms are short, however, this is not decisive.

An example to explain:

A crafts company had its website redesigned by an advertising agency. For services and software, the crafts company issues a bill of exchange for €15,000. The discount amounts to €225. The calculation was made using the commercial interest formula, 6% discount and a 90-day term. So interest of €225 is charged. The bank receives this.

The effective interest rate of the loan of €14,775 is, however, 6.09% after the general interest formula. Calculated with €225 interest over a period of three months.

Effectively the interest is therefore slightly higher. Nonetheless the discount loan is very inexpensive. Compared, for example, with an overdraft facility (disposition credit), it is definitely about 2% lower. There, 8% interest is still the lower rate that banks charge for overdrawing an account. Usually the interest rate is rather 12% and more.

Also important to know:

- Every bill is taxable.

- Banks can charge fees for submitting a bill.

- If a bill is issued so that it is not payable at a banking place or not payable at a bank, an additional fee is charged.

What alternatives are there to the discount loan?

Sometimes everything happens at once: four invoices arrive in the post, but only one of the eight outstanding claims has been settled. The discount loan then offers a chance as a short-term loan to still be able to pay your own invoices even if money is missing. Are there alternative bank loans to the discount loan?

One option is to overdraw the current account. The overdraft facility (Dispokredit) or also the current account credit (Kontokorrentkredit) provides short-term financial leeway. The bank grants the account holder a certain credit line up to which the account may be overdrawn. The loan does not have to be approved anew each time. It is available at any time. That means a certain amount is set that can be drawn up to this maximum. This allows more money to be withdrawn or transfers to be made than the actual balance on the account. How high the granted overdraft limit is depends on the account holder's monthly net income. In general it is around three times the net income. For business accounts this is also called a working capital or seasonal loan (Betriebsmittel- or Saisonkredit). The interest charged by a credit institution for the short-term loan is high. They are typically at least 8 percent, usually more at 12-14 percent. An overdraft can thus cover very short-term cash shortages. If money is needed for a longer period, other bank loans are cheaper.

The Lombard loan is also an alternative to the discount loan. With the Lombard loan, the bank receives collateral for lending money short-term. This serves as security for repayment. These can be items as well as bank deposits or securities. Here, credit institutions like to differentiate: for goods the borrower gets at most 2/3 of the value of the item. For securities it is 3/4 of the value. The collateral transfers to the lender's possession. To redeem it, the borrowed sum together with fees and interest must be repaid at a set date. If this does not happen, the collateral becomes the property of the bank. Sometimes the Lombard loan can also be extended. Further fees and interest then apply.

Acceptance credit and discount loan - where is the difference?

The discount loan and the acceptance credit are very similar. And yet they differ in one essential point. With the discount loan the issuer of the bill and the bill holder are liable. With the acceptance credit the bank steps in as the one who issues the bill and is also liable for it—just like the bill holder.

This means for example: A chain of gift shops can buy inexpensive Christmas decorations for €40,000 at short notice. But it is only early September. The company will be able to resell the goods at the earliest in eight weeks. The company therefore uses a bill with the bank. This bill specifies the sum to be repaid and the date on which the amount is due—here in the example in eight weeks. The bank accepts the bill; it guarantees for the company. For this the credit institution charges a fee or commission. It is usually 1–3 percent of the sum per year. The gift shop chain passes the bill on to the supplier of the Christmas decorations. Because the bank is liable, the supplier can be very sure that he will receive his money in eight weeks. When the bill is due, the supplier turns to the bank to obtain payment for the goods, and only at that time does any money flow to any account. And the credit institution turns to its customer, for whom the bill was issued.

With an acceptance credit, the bill transaction therefore takes place between the bank and the customer, not between customer and supplier or manufacturer. That is the essential difference to the discount loan. There too, bank, company and its customer are involved. But the bill is issued by the customer, accepted by the company and then handed over to a credit institution, which in effect advances the amount on the bill.

How did the discount loan come about? - The history of the discount loan

Borrowing money quickly and cheaply—with the discount loan this was easy until the end of the last century. Banks liked to grant this form of loan. Why was that? They sold the bills to the Bundesbank and could thus refinance the lent money, i.e. retrieve it. And at the favourable discount rate.

The Bundesbank also controlled how much money was available to banks for lending. It thus regulated the possibility for banks to increase their own liquidity and grant loans to companies and private individuals. The set discount rate played an important role in this. Until 1999 the discount rate was the lowest key interest rate to which many things were oriented.

Until the end of the 1970s the discount business was the decisive way for banks to obtain funds. From the mid-1980s, however, it lost importance. The discount loan was used less. This is explained by the cost- and personnel-intensive effort. Securities repurchase transactions (Wertpapierpensionsgeschäfte) took the place of the discount business. The Lombard rate as a deduction for pledged securities displaced the discount rate as the significant interest rate. When political decisions on money supply were transferred to the European Central Bank (ECB), the Deutsche Bundesbank's discount business—the purchase of bills at the discount rate—lost even more importance. Banks therefore grant the discount loan rather rarely today.