Meaning of the term "annuity"

The term annuity contains the Latin word "anno", meaning "year". An annuity in financial mathematics and in the language of finance professionals goes back to this designation.

Ultimately, an annuity is a regular payment that always has the same amount. If a borrower, for example, takes out a loan structured as an annuity, this means that their monthly or annual installments to be paid are always the same amount. The installments consist of an interest portion and a repayment portion. This is explained with a simple example.

Example calculation to illustrate an annuity loan

A borrower takes out a repayment loan as an annuity loan.

The term of the loan in this example is five years, the loan amount is 100,000 Euro, and the interest rate is fixed for the term and set at five percent per year.

The fixed interest period means that the interest rate remains unchanged over the loan term. The initial repayment is also five percent per year. This constellation may not be very common in practice, but it helps to explain the topic. Any fees or other influencing factors are ignored in this example for the sake of explaining the annuity.

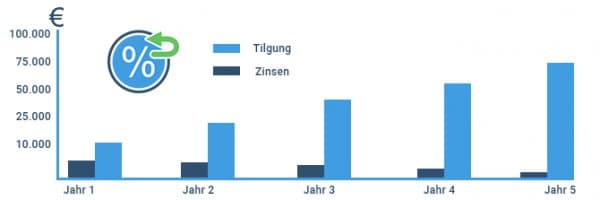

- In the first year of the annuity loan term, the borrower starts with a liability of 100,000 Euro. He pays five percent interest on this and repays the liability with an additional five percent in the first year — in total his annuity payment amounts to ten percent, which he must pay in the first year. These ten percent therefore correspond to 10,000 Euro that the borrower must pay. The interest rate is therefore 5% of the loan, with the interest portion of the paid installment in the first year being 50%.

What is special about an annuity loan is this: The installment of 10,000 Euro, which results from the summed percentage rates of interest and repayment in the first year, defines the amount of the installments that must be paid in the following years. They also amount to 10,000 Euro per year.

- After the first year the borrower has therefore paid 5,000 Euro in interest and has repaid another 5,000 Euro of his loan. He therefore has only outstanding liabilities of 95,000 Euro. Since the second year still falls within the five-year loan term, the borrower must again pay five percent interest to the bank in that year. In this example that means 4,750 Euro in interest becomes due.

However, since the annual installment remains unchanged at 10,000 Euro and the interest has fallen by 250 Euro to 4,750 Euro compared to the previous year, the repayment portion in the second year increases by exactly 250 Euro to then 5,250 Euro. At the end of the second year the borrower has therefore already repaid a total of 10,250 Euro. He therefore still has outstanding liabilities of 89,750 Euro, which he will pay to the bank over time.

The principle for calculating interest and repayment in an annuity loan remains the same in the following years, so the calculation will no longer be shown in such detail below.

- In the third year the borrower pays 4,488 Euro in interest and can accordingly repay 5,512 Euro of his liabilities. The outstanding balance of the borrower at the end of the third year with respect to his bank thus amounts to 84,238 Euro.

- In the fourth year of the term, 4,212 Euro in interest are due, leaving 5,788 Euro for repayment, and his liabilities at the end of the fourth year of the loan term amount to 78,450 Euro.

- The fifth year is also the last year of the loan term. In this year the borrower pays 3,923 Euro in interest and can then make repayments of 6,077 Euro. The outstanding balance at the end of the loan term thus amounts to 72,373 Euro.

Interest and compound-interest effect in annuity

One interesting thing about all these calculated figures and values is this: At the beginning of the term interest and repayment were equally high. During the term of the repayment loan the interest payments decreased continuously, so that more room remained for repayments. In just five years the annual interest payments fell by more than 1,000 Euro compared to the interest charged in the first year of the loan term.

Mathematically, this is also due to an interest and compound-interest effect, which occurs with an annuity loan regardless of the parameters set in the example. In general this can be formulated as follows: With an annuity loan the total sum of interest and repayment that the borrower has to pay within a defined time period (e.g. per year) remains constant. With each monthly installment the ratio of interest payments to repayment payments shifts in favor of repayment.

Annuity loans in practice

Annuity loans are quite common for loans with a long term, for example mortgage loans. They have the advantage that the annual and thus also the monthly burden for the borrower is fixed from the start of the loan term. In times of low interest rates for mortgage financing, it is therefore advisable to take out an annuity loan with a as long a term as possible.

Because interest rates are low, this may leave a larger financial scope for the borrower to set a higher repayment rate and thus a larger repayment portion per monthly installment — the five percent defined in the example is already set very high for a mortgage loan in reality. It is common to repay at least one percent of the initial loan amount per year. If the borrower and the bank agree on a higher repayment rate than this minimum one percent, he can also realize better interest and compound-interest effects over time.

Extra repayments on a loan with annuity

This also applies if the borrower takes out an annuity loan that grants him the right to make extra repayments — in a low-interest phase banks often agree to five percent extra repayments; in times of a higher interest level they may sometimes accept ten percent extra repayments. That means that one can then pay up to ten percent of the initial loan amount per year as additional repayment. This, of course, also reduces the outstanding balance and has an immediate positive effect in the following year, since less interest must be paid and thus a larger amount is available for repayment.