What is a mortgage loan?

A mortgage loan is a financial product used in the context of property financing. The loan uses the registration of a land charge on a property or plot of land as security for the provision of funds. In addition, building rights or land rights can be provided as collateral.

Key points in brief:

- A mortgage loan is always granted in connection with property financing.

- The loan is secured by a property or a plot of land.

- Mortgage loans are granted by banks and insurance companies.

Definition: Loan

A loan can involve the temporary transfer of the right to use money or goods. The contractual terms are individually agreed for each loan. Colloquially, a loan is also referred to as credit.

Mortgage loan terms

What projects are suitable for a mortgage loan?

A mortgage loan is always used in connection with real estate and land rights. However, this does not automatically mean that the loan is exclusively suitable for property financing. Although financing the purchase or construction of a property is the most common reason for using a mortgage loan, it is also relevant for other purposes:

- Extension or conversion of existing properties

- Debt restructuring (refinancing)

- Retirement planning

Loan amount

How large can a mortgage loan be?

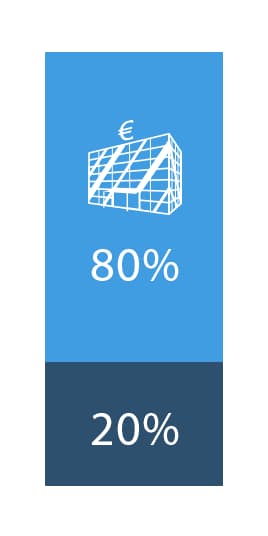

There is no legal upper limit on the actual amount of a mortgage loan. However, there are legal provisions regarding the composition of the financing. A mortgage loan is generally offered in two financing portions. It can cover 60% or 80% of the total financing sum for building or buying a house. This means that at least 20% of the costs must be provided as equity or through other forms of credit.

Full financing for property financing

More and more banks offer the option of using full financing for a mortgage. This is usually associated with extremely unfavorable terms. It is advisable to avoid this expensive form of property financing and instead save sufficient capital for the construction or purchase of a house.

Up to what amount is a mortgage loan sensible?

Small loan amounts should, if possible, not be covered by a mortgage loan. In the event of default, the bank can exercise its right to sell the property and cover the outstanding debt from the sale proceeds. A classic consumer loan cannot easily be used to attack real estate. This can only be implemented in the context of personal bankruptcy. Accordingly, mortgages are only sensible for financing large capital amounts.

Who can get a mortgage loan?

Any person of legal age and with legal capacity can use a mortgage loan. Depending on individual circumstances, the conditions such as costs and term vary. Since the mortgage loan is always granted in connection with a property or a plot of land, ownership of these is required.

Who offers mortgage loans?

A classic mortgage loan used to be offered exclusively by banks. Nowadays, it is also possible to conclude this property financing through insurance companies. The offers do not differ substantially from those of banks. Individual terms and costs determine whether the contract is the right choice for one’s own property financing.

What requirements must be met for a mortgage loan?

The actual requirements for the borrower are determined by the lending institution. There are no detailed statutory requirements. Nevertheless, loan agreements are structured very similarly and often have overlapping requirements:

- Legal age and legal capacity

- Stable income from permanent employment

- Clean credit check

Specific conditions may require permanent employment of more than 12 months. Existing financial obligations must of course be taken into account. Negative SCHUFA entries impair the credit score and worsen the prospects of mortgage approval.

Tip: If the application for a mortgage loan is rejected on the first attempt, it is worth seeking a personal discussion with the financial institution. Bank advisors are able, in special cases, to draft tailored contracts that take the individual financial situation into account.

What should you pay attention to when taking out a mortgage loan?

There are many mortgage offers. Consumers can choose from different models offered by numerous providers. Finding the best offer is not always easy. The cost factor is crucial. For this, it is important to understand how the costs of a mortgage loan are composed.

Costs of a mortgage loan

The basic costs consist of the loan amount and the agreed mortgage interest. In addition, there are fees to consider. For a concrete comparison, the annual percentage rate (APR) must be available. This includes all costs. The nominal interest rate only states the repayment amount and the agreed interest rate. The concrete costs for the mortgage loan also depend on the loan conditions:

- Term

- Loan amount

- Special repayment clause

A good mortgage loan is structured in a consumer-friendly way. Ideally, the contract specifies whether special repayments are possible. A special repayment allows the borrower to reduce the outstanding balance by making a one-time capital payment. The contract states how often and in what amount such a repayment is possible without incurring prepayment penalties.

Definition: Prepayment penalties

If special repayments are not contractually regulated, such a payment incurs extra costs. They can be seen as a kind of penalty payment. An early repaid loan reduces the bank’s interest income, which yields less profit. As compensation, a prepayment penalty is claimed.

How are the interest rates for the mortgage loan determined?

Banks and other financial institutions base the setting of mortgage interest rates on the so-called base interest rate. The base rate is set by a central financial body. For the greater Europe region, this is the European Central Bank. Depending on the region’s economic situation, the rate is raised or lowered. In weak economic times, the rate is low. The European Central Bank thus relieves banks, which rely on the central bank’s terms for their business.

The resulting financial relief for financial institutions is passed on by the banks to consumers. This gives a larger number of consumers access to financing of all kinds. This stimulates purchasing behavior, which ultimately boosts the overall economy. The base rate is thus determined by the central bank and is very similar across individual banks. The actual interest rate is then adjusted to the individual circumstances of the mortgage loan.

Consumers can also choose between fixed-rate mortgages and variable interest rate mortgages. A fixed-rate mortgage fixes a specific interest rate for a defined period. During this period, the lender does not adjust the interest rate. If the current base rate is low, you secure favorable conditions for a long time. The fixed rate is usually set slightly above the current market rate.

A mortgage loan with a variable rate is regularly adjusted by the bank to market conditions. If the base rate increases, higher costs are incurred for repayments. With a falling base rate, the monthly payments decrease. Most banks offer a maximum and minimum interest rate that will not be exceeded or fallen below regardless of market conditions. Mortgage loans taken out when the base rate is high often benefit from falling rates in the future.

Advantages and disadvantages of mortgage loans

A mortgage loan is unquestionably the first choice for property financing. The advantage is that there are countless offers. Large banks provide excellent terms for every consumer. Since the loan uses the property as collateral, granting is often relatively uncomplicated. The high security reduces the risk for banks and insurance companies. During low-interest periods, a mortgage loan is an inexpensive form of property financing. Flexible contracts are also advantageous in the long term. Accommodating providers rely on consumer-friendly conditions for special repayments or refinancing.

Nevertheless, a mortgage is not always the best option. If there are already financial obligations on the property, the costs are very high. Extending the contract term drives up interest costs. Short contract terms come with high monthly interest. A mortgage loan cannot be used for full financing without down payment — special cases are associated with very high costs.

Advantages of the mortgage loan at a glance:

- Easy loan approval due to high security for the bank

- Flexible contract conditions

- Special repayments possible

Disadvantages of the mortgage loan at a glance:

- Suitable for a maximum of 80% of property financing

- Long term increases total costs

Repayment and termination of mortgage loans

When selecting the appropriate mortgage loan, the conditions for repayments and terminations are important. We have already explained the area of special repayments. But what about terminating a mortgage loan?

Early repayment of a mortgage is not uncommon. The reasons vary widely:

- Unexpected capital from business success or inheritance

- Strong fluctuations in the financial market justify refinancing

- Sale of the property

Depending on the type of mortgage loan, different conditions apply. It is important to be well informed about the various cases before signing the contract.

What should be considered for early repayment of a mortgage loan?

A complete payoff of the mortgage is always associated with additional costs. If a special repayment is agreed, it is credited toward the full settlement. The capital sum remaining determines the amount of the prepayment penalty. The bank must allow the borrower the possibility to terminate the contract at any time. The exception is fixed-rate contracts. These contracts cannot easily be terminated within the first ten years. Beyond that, however, there are no problems; this applies even if the fixed rate is agreed for more than ten years.

Special right of termination

As with all contracts, mortgages also include a special right of termination. It applies, for example, if the borrower dies. To be protected against this risk, mortgages offer the option of providing additional collateral in the form of term life insurance or residual debt insurance.

A special right of termination also applies to the sale of the property. The consumer does not have to disclose the reasons for the sale.

Refinancing of mortgage loans

Does refinancing a mortgage loan make sense?

Refinancing is a frequently mentioned topic — yet few know the details. Refinancing pays off an existing mortgage loan. The required capital comes from a new mortgage loan. If the ongoing costs for the mortgage are very high, refinancing achieves significant savings. The total cost of the loan is reduced with better interest conditions. If the mortgage was taken out during a period of high interest rates, a lower base rate brings real savings potential. Refinancing reduces the APR and thus the monthly installments.

Mortgage loan: refinance or reserve interest rates?

Refinancing a mortgage loan is not the only option available to property owners. A loan with a fixed rate needs a new financing model after the fixed-rate period ends. If current interest rates are low, the consumer can reserve the interest rates for the follow-up financing. The prerequisite is that the loan expires within 42 months. If the low interest rate is reserved, the loan continues immediately under the new contract terms.

The interest reservation is not tied to the house bank. Customers should obtain several offers. The longer the rates are fixed in advance, the higher the extra costs—because banks charge for this service. Compared to refinancing, the option can be cheaper. Especially when the costs for early termination are very high.

Types of mortgage loans

Can mortgage loans and building savings loans be combined?

Another form of mortgage financing is a so-called combined loan. This combines the features of a mortgage loan with a building savings loan. The repayment of the mortgage loan is covered by the payout amount from the building savings loan. This sounds logical at first glance. Consumers pay the monthly costs for the financial products separately. Only the interest costs are due for the mortgage loan. The installment payments are paid into the building savings contract. Once the building savings contract matures, it repays the outstanding amounts of the mortgage.

This offer should be treated with caution. Although a building savings contract may entice with low monthly payments, the repayment period is extended enormously compared to a classic mortgage. As a result, interest costs for the mortgage increase and the overall financing becomes more expensive.

Mortgage loan - secured with residual debt insurance?

An alternative to life insurance is residual debt insurance. It applies in conjunction with the mortgage loan. Borrowers can choose from various insurance options:

- Accident insurance

- Life insurance

- Unemployment insurance

- Insurance in case of divorce

- Critical illness insurance

- Disability insurance

Policies are subject to strict payout conditions. In addition, there are waiting and qualifying periods. The payout duration in the event of involuntary unemployment is only 18 months.

When is residual debt insurance sensible?

Residual debt insurance incurs relatively high costs. Compared to a classic life or accident insurance, this type of insurance is rarely worthwhile. In exceptional cases it is required for credit security. It is also suitable for borrowers who need a quick contract conclusion but cannot provide existing collateral in the form of insurance policies.

Mortgage loans compared with other credit types

A mortgage loan is in many cases the best form of property financing. However, other options are also available to consumers. Which is best in an individual case depends greatly on personal circumstances and requirements. When choosing financing, it should always be ensured that there is sufficient financial leeway. If the monthly burden is calculated too high, a financial bottleneck can quickly occur.

Mortgage loan from the bank or pre-financing through a building society?

The building savings loan is not only available to consumers in combination with mortgages. Building savings contracts are a classic form of property financing. The principle behind them pools savers and borrowers into a fund to enable favorable loan interest rates.

At the start of the building savings loan, a basic savings balance is accumulated. Once the contractually agreed savings amount is reached, a loan is offered on favorable terms. If there is not enough capital in the communal fund at the agreed maturity date, the payout can be delayed. If there is no building savings contract at the start of property financing, immediate building savings loans are available. The required amount is available immediately and is paid off later by the maturity payout from the building savings contract. In this case, the interest rates are based on the current market level. This building savings loan is interest-only. The loan is therefore serviced exclusively with the agreed loan interest. At the same time, payments are made into the building savings contract. Compared to a mortgage loan, this form of pre-financing is usually more expensive.

Why choose a mortgage loan and not a classic consumer loan?

For high loan amounts, financial institutions work with collateral. In the event of the borrower’s inability to pay, this collateral covers outstanding payments. This prevents the bank from making a loss. A classic consumer loan does without such collateral. If the customer becomes unable to pay, the bank only has recourse within the framework of personal bankruptcy to recover outstanding amounts. These are then distributed proportionally to various creditors — in the worst case, the bank makes a loss. For small and medium capital amounts, this is not a problem for banks. High sums required for property financing must, however, be secured with collateral.

Mortgage loan or life insurance?

Property financing can be a combination of a classic mortgage loan and a life insurance policy. During the term of the life insurance, only interest costs are incurred. The loan covered by this is repaid at the end of the term with the lump-sum payout from the life insurance. Generally, this model offers few advantages, but it can be an interesting option in individual cases. Existing life insurance policies are an interesting repayment component. However, consumers should carefully calculate in advance whether the model is worthwhile.

If the life insurance generates a higher return after deducting all costs than is required to service the loan interest, builders can comfortably opt for this solution. Certain conditions favor this scenario:

- The insurance has a contract term of at least 12 years.

- The policy was concluded before 31.12.2004.

- The payout is offered as a lump sum.

- Contributions were paid for a period longer than five years.

In the past, this model was very popular because tax obligations did not apply to payouts from the insurance policy. A law change came into force at the beginning of 2005 that largely removed these advantages.

Partial financing via a life insurance policy is also referred to as a bullet loan. The term bullet loan is also used in connection with the assignment of private pension insurances, building savings contracts, or investment funds. In any case, the repayment is due only at the end of the contract term.