Guarantee

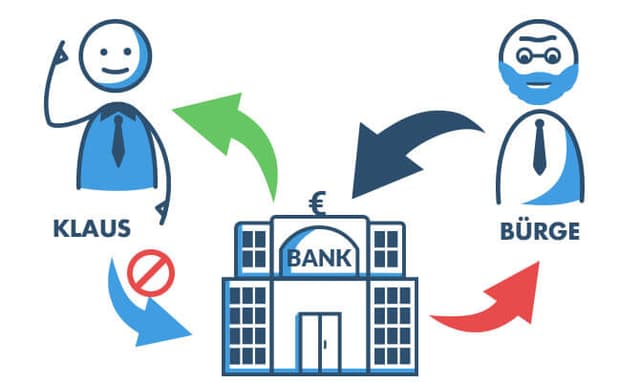

Finally nothing stands in the way of buying the car. The new vehicle has been chosen and configured with all sorts of special equipment. Now it is only a matter of shaping the leasing contract appropriately so you can soon drive to customer appointments with the smart vehicle. The conversation with the advisor goes well. The financial conditions fit. The down payment is reasonable and the monthly leasing payments are manageable. Then almost everything would be settled. But then collateral for the vehicle loan comes up. If you are self-employed, your chances are very poor. Often neither a home nor other bank balances and assets help. With self-employed people, the lender wants to play it safe. The risk that the loan will not be repaid is often considered too high. If you can name a guarantor, however, the loan is practically in your pocket.

What is a guarantee?

To take out a loan, you need collateral. Whether this is sufficient is always decided by the bank on a case-by-case basis. Collateral can be, for example, fixed-term deposit accounts. It can also be proof of income if you are employed. Lenders also like to take real estate as security so they can be sure they will get their money back. Sometimes these securities are not enough for the lender. If, for example, you have just started a company or work freelance, it is considerably harder to borrow money. With employees, the bank can in the worst case have the salary garnished. If the borrower can no longer pay, part of the wages is immediately used to repay the loan. This option is not available for self-employed people, for example. People who need money are often forced to name a guarantor. The guarantor undertakes to repay and cover the costs of the loan if the actual borrower can no longer do so themselves.

Who has which role and which duties in a guarantee is regulated in Section 765 of the German Civil Code (BGB). The guarantee is therefore also referred to as a BGB-guarantee.

A person "guarantees" that another person will fulfil the obligations of their contract. This person is called the guarantor. The guarantor guarantees that the borrower or debtor, who for example borrows money, will repay that money. Anyone who wants to rent an apartment may also have to name a guarantor. If it is foreseeable that the future tenant might have trouble paying the monthly rent, a landlord may require a guarantee declaration. Guarantors help debtors when creditworthiness according to the Schufa report is not the best. With the help of a guarantor, they can often still rent an apartment or borrow the necessary sum.

For a guarantee it is not enough for the guarantor to give a verbal promise that the contract will be fulfilled. In the event, the guarantor steps in in place of the borrower. He is liable with his entire assets and may have to pay the monthly installments. He thus steps in as debtor in place of the principal debtor.

What is a guarantor? Who can guarantee?

In a classic Western there is often a figure who helps ensure that a pursued person faces his pursuer and thus his fate. This comparison can be applied well to a guarantor. He ensures that pursuer and avenger meet. Otherwise, the "guarantor" would also be held accountable.

The guarantor is therefore a person who vouches for the credibility of another person. He agrees to be jointly liable with the debtor so that the latter can meet his obligations. That is, that he repays the borrowed money. If he cannot, the guarantor steps in and must repay the debt and any interest. The only prerequisite a guarantor must meet is being of legal age. A guarantee can also be split among several people. So not only a single guarantor can stand in for someone, but also several people.

How is a guarantee structured?

A guarantee is a unilateral contract. The guarantor has obligations towards the lender (the creditor). From this contract, however, he does not derive any rights. This is in contrast to the loan agreement, in which the bank (creditor) provides a customer (debtor) with money for a certain period. For providing the loan amount, the bank receives interest. In addition, the lent money is returned at the agreed time. In the loan contract both sides therefore have rights and obligations.

The guarantee agreement must always be recorded in writing. What is the amount of the guarantee? What kind of main debt is it? Who is the creditor? The written guarantee declaration must, for example, state these and generally all essential characteristics of the guarantee.

A corresponding document that exists only online or as an email would not be binding and therefore invalid. There is one exception: an authorized merchant (Vollkaufmann) can under certain circumstances give an oral guarantee if the guarantee is part of a commercial transaction for them. For non-merchants a guarantee can be one of immediate enforceability (selbstschuldnerisch), for a merchant every guarantee is considered immediate. This means he has no right to the defense of prior enforcement (Einrede der Vorausklage). That in turn means that a guarantor can refuse payments to the bank as long as enforcement against the principal debtor has not been exhausted. For a guarantee that is of immediate enforceability this option is not available.

Form of the guarantee - in brief:

- Guarantee declaration must be in writing

- Guarantee declaration must list all essential characteristics

- Oral guarantee possible for an authorized merchant under certain conditions

What is a "guarantee on first demand"?

The guarantee on first demand represents a special form of guarantee. While the legal framework for guarantees is laid down in the BGB, there is no statutory regulation for the "guarantee on first demand". It has evolved and established itself through the contractual freedom of the debtor. Guarantee on first demand means that the guarantor waives the defense of prior enforcement (Einrede der Vorausklage). That means he can be called upon immediately by the creditor. He must therefore pay immediately when demanded. However, the creditor must prove that his claims are justified. Otherwise, the guarantor has the option to reclaim the paid money via a restitution process. For the lender, this form of guarantee has the advantage that he receives money in the shortest possible time. As with an immediately enforceable (selbstschuldnerische) guarantee with waiver of defenses, the guarantee on first demand is also more disadvantageous for the guarantor, because he must pay immediately. There is no assessment of whether the principal debtor may still raise funds to service the loan.

Types of guarantee - Which different types of guarantee exist?

Now it has happened: the friend or partner for whom you guaranteed with your signature can no longer pay the rent. When do I have to step in and take over the monthly payments? Are there certain deadlines or conditions for that? Yes, there are. Guarantees can take various forms. Each form brings different obligations, rights and duties. Generally, guarantees can be distinguished between the guarantee against default (Ausfallbürgschaft) and the immediately enforceable (selbstschuldnerische) guarantee. Often one also hears of global guarantees, joint guarantees and maximum amount guarantees. Some also distinguish ordinary guarantees, co-guarantees and time-limited guarantees. At first glance there are quite a few types of guarantee. Who can keep track of all these? Let's try here to give an overview of the different types of guarantees.

The guarantee against default (Ausfallbürgschaft)

"Look before you bind yourself." This saying applies not only to those willing to marry but also to financial matters. Trust is the foundation of everything. Whoever guarantees, trusts. How can a guarantor still be reasonably sure that he will not lose all his assets because he signed a guarantee declaration and then has to step in for a friend or partner who has become unable to pay?

The safest variant for a guarantor is the guarantee against default. It is the legally usual form of guarantee. It is also called the "ordinary guarantee". (§ 765 BGB)

Don't worry: the creditor may not immediately approach the guarantor if his debtor suddenly stops paying the installments. A guarantor must only step in and pay when all possibilities to obtain the money from the principal debtor have been pursued and exhausted.

What must the creditor do? He must sue to enforce his claims. He must litigate against the debtor until enforcement measures (Zwangsvollstreckung) are reached. Only if these do not bring back the money can he turn to the guarantor. Only at that point does the guarantor step in.

However, it is sufficient if enforcement has been reached; it does not have to have been executed. If the creditor can prove that he has initiated all steps and all other securities have already been realised, then he may turn to the guarantor.

In case of the principal debtor’s own fault for the loss incurred - for example if the principal debtor admits it is his fault that he can no longer pay - the guarantor does not have to be liable.

When do guarantee banks step in?

What happens if the installments are no longer paid? Does the creditor (the lending institution) have to bear the losses? Must the bank accept the lent money as a loss? If a customer can no longer meet his loan obligations and all other securities have been used to make payments, and if all of that no longer helps, a guarantee bank takes over the guarantee against default. In this case it is referred to as a modified guarantee against default. The lender receives its money. The principal debtor must then pay the guarantee bank. The debt relationship transfers to the guarantee bank in such a case.

Modified guarantee against default

When is the time at which someone truly can no longer pay? When does default occur? In the so-called modified guarantee against default, this can already be defined in advance.

If payment is still missing three months after the loan is due, the creditor waits three months before taking further steps to recover the money. As a reference point, lenders also like to set the moment when formal insolvency proceedings are opened against the principal debtor.

The modified guarantee against default is, for example, common when cities and municipalities act as guarantors, i.e. with public corporations. The same applies to guarantee banks and credit guarantee associations.

In all cases: first all other securities are checked and used to settle the debts. If someone owns a house or flat, i.e. real estate, they must reckon with foreclosure. Machines and vehicles are also sold under compulsion to cover the costs. If the debts are thereby settled? Great. Is a remaining amount outstanding? Then the guarantee against default must pay this sum.

The immediately enforceable guarantee (Selbstschuldnerische Bürgschaft)

Is the principal debtor still able to pay? But he has missed one or two or three installments? Then the lender can also demand these amounts from the guarantor.

In an immediately enforceable guarantee the debtor and guarantor are equally liable. It does not matter whether the principal debtor could in principle still pay the installments. The guarantor must then claim his money from the debtor.

Is an immediately enforceable guarantee safer? For the creditor side this form of guarantee means greater security. For the guarantor, however, the immediately enforceable guarantee carries more risks.

Difference between the immediately enforceable guarantee and the ordinary guarantee

If you are asked to pay, you should stay calm. Are the payment demands really justified? First it should be checked whether all options of the borrower to still pay the owed amounts have really been exhausted. The guarantor can, for example, have a court clarify whether the principal debtor still has assets that could be used to settle the debts. Only when all legal remedies have been exhausted must the guarantor make his contribution.

Legally this is called the "Einrede der Vorausklage" (defense of prior enforcement). This is possible with the ordinary guarantee. It is not possible with the immediately enforceable guarantee. The latter forces the guarantor to act immediately if the principal debtor is insolvent. There is no delay. If the guarantor refuses payment in the event, the creditor can apply for enforcement.

However, the guarantee contract must explicitly state the waiver of the objection. The contract must contain a corresponding clause. The whole thing must be recorded in writing. Because, as with the ordinary guarantee: an oral agreement is not legally binding and therefore invalid.

Where is the immediately enforceable guarantee used?

If the creditor doubts that his principal debtor can really pay regularly and reliably, if he must expect not to get his money back, and if the risk of default that a bank or credit institution anticipates is very high, it will insist on an immediately enforceable guarantee. Which loan agreements does this affect? In principle a lender can secure almost any loan this way.

Rental guarantee - When may a landlord demand a guarantor?

The immediately enforceable guarantee is often used in the context of a rental guarantee. Landlords increasingly secure themselves with this form of guarantee so that the rent is paid on time. This is the case when the landlord assumes that the prospective tenant’s financial situation may not be sufficient to pay the rent regularly and on time. Students, for example, usually do not have a fixed income. If a student or several students want to rent an apartment, the immediately enforceable guarantee protects the landlord against default of the monthly rent. As a rule, the parents of the tenants are involved as guarantors.

What is the difference between a guarantee and a co-signature on the rental contract?

Rental guarantee or second signature on the rental contract? Beware if a landlord insists that the guarantor also signs the lease. The guarantor is only responsible for ensuring that the rent is paid punctually and regularly. Someone who signs the rental agreement, however, is also responsible for all the tenant's obligations. In addition, that person must also sign a termination if the actual tenant wants to move out. Only if both tenants sign the termination is it effective.

Maximum amount guarantee (Höchstbetragsbürgschaft)

To limit liability in an immediately enforceable guarantee, a guarantor can set a maximum amount in the contract. This is the amount for which he is liable at most. If this clause exists, it is called a maximum amount guarantee. In some general terms and conditions this amount includes, besides the claims and accrued interest, also commissions and other costs. Anyone considering guaranteeing should be aware of this or ask about it before signing the guarantee contract.

Time-limited guarantee

"Until death do us part..." What applies in marriage may also apply to guarantees in some cases. A guarantor can, however, limit his willingness to be liable in time. Then a deadline or date is recorded in the guarantee contract. The guarantor is only liable until that date if the principal debtor defaults. After that, no longer. Once this period has expired, the guarantor can no longer be held liable for the obligations of the original borrower. A "time-limited guarantee" is also meant when a guarantor only covers debts of the borrower that arise within the period defined in the contract.

Partial guarantee - one guarantor or several guarantors?

It does not always have to be a single guarantor. Anyone who wants to spread the responsibility among several people can do so. A guarantee contract can also name several people. Co-guarantors are liable in equal shares for the default of the borrower. Or an immediately enforceable guarantee is allocated proportionally to individual persons. In this case the share of the guarantee must be exactly assigned to the individual persons and specified in the contract.

Liability in an immediately enforceable guarantee

Is a guarantor responsible for all debts of the original contracting party or borrower? The concerns are great. Whoever agrees to a guarantee is liable with his entire assets. Must he stand for all debts that the debtor/tenant/borrower has accumulated? Don’t worry, this is not the case. Yes, as guarantor you are liable with your assets, including your private assets. And no, you are not responsible for all debts of the contracting partner. The immediately enforceable guarantee only applies to a concrete contractual object. For example, in a rental guarantee this is the monthly rent. For a loan it covers the loan amount and the interest for its provision.

Immediately enforceable guarantee with waiver of defenses

Occasionally there is an agreement in an immediately enforceable guarantee contract in which the right to raise defenses is waived. This is the strictest form of guarantee. Banks and lenders particularly like to protect themselves with this form. It means that a guarantor must, in any case, be liable. Normally the debtor is entitled to certain "defenses."

Defenses of the guarantor are, for example, agreements that the guarantee only applies under certain conditions. Only when these conditions occur is he liable for the debt. Forbearance, statute of limitations or the right to withhold a sum are, for example, points the principal debtor can assert against the creditor. The guarantor can also raise these defenses.

The defense of prior enforcement (Einrede der Vorausklage) is excluded from the outset with the immediately enforceable guarantee. A guarantor therefore cannot insist that the creditor first use all possibilities to make the principal debtor pay.

If the principal debtor is insolvent and there is an immediately enforceable guarantee with waiver of defenses, then the guarantor must step in immediately.

What does "accessoriness" (Akzessorietät) mean?

Accessoriness means: one right exists prior to another and a subsidiary right depends on the existence of a principal right. Applied to a guarantee it means:

The obligation arising from a guarantee depends on the claim it is meant to secure. The guarantor is therefore only obliged as long as the principal debtor repays the loan.

If the guarantor has stepped in for the principal debtor, i.e. has fulfilled his obligation to the creditor and has paid the required installments and settled the loan, then the guarantor acquires the claims that the creditor previously had against the debtor. They pass to the guarantor. Do other accessory securities such as a mortgage or lien exist? These also transfer from the creditor to the guarantor.

Non-accessory securities such as assignments of claims (Sicherungsabtretungen) or transfer of title by way of security (Sicherungsübereignung) are not automatically transferred by the original creditor to the guarantor. However, the guarantor can demand this.

What to consider with a guarantee

Is a guarantee registered with Schufa?

Anyone who plans to take out a loan in the foreseeable future needs a good rating with the German credit bureau (Schufa). Only then is a person considered creditworthy. Certain entries worsen this scoring value. This happens without the person necessarily noticing it. An invoice was not paid? A reminder was overlooked and the account was garnished? These incidents are included in the credit assessment. Guarantees are also included in the calculation of one’s Schufa score. This applies even though the guarantor is not the borrower. It can quickly turn into a disadvantage. If the guarantor himself wants to apply for a loan, the bank checks with Schufa. Depending on the overall financial environment, the lender may reject the application. A guarantee is a contingent liability. Schufa treats it like a loan because the bank bears a risk. If the principal debtor can no longer pay the installments, the guarantor must step in and cover the repayments and interest for the loan.

When are guarantees not lawful? When is a guarantee considered immoral (sittenwidrig)?

The rules for a guarantee are laid down in the German Civil Code (BGB). If the principal debtor and guarantor are, for example, related or married, a guarantee can under certain conditions be considered immoral. This is the case if the borrower’s loan would be too great a financial burden for the guarantor and the guarantor would be financially overwhelmed.

Guarantee overburdens the guarantor’s financial means

Whoever is married is jointly liable? Banks can propose one spouse as guarantor when granting a loan. This co-liability variant is legally acceptable if the spouse can actually repay the debt. This applies especially when one spouse guarantees a loan that brings them no benefit. If within five years the guarantor cannot repay a quarter of the guaranteed sum, for example because they have no own income, then this guarantee is immoral. It must be realistically possible for the guarantor to pay the installments and interest. Therefore, a reputable lender always checks the guarantor’s financial circumstances.

Downplaying the consequences of liability of the guarantee

"Oh, that's just a formality. You won't have to make the payments anyway. It's no big deal." If someone is persuaded to give a guarantee with words like these, the guarantee is being downplayed. The person who is to co-liable for a friend or partner is being deceived. If a guarantee comes about in this way, it is ineffective. However, in the event that the guarantor is later required to step in and pay, the guarantor must prove that he was told something false when the contract was concluded.

How can I get out of a guarantee? When does a guarantee expire?

Whoever signs a contract also bears responsibility. This applies, of course, to a guarantee contract. A loan guarantee runs until the principal debtor has repaid his loan.

Are there ways for a guarantee to end before expiry?

A guarantee ends when …

- the debt is repaid. This is the case when the loan has been fully repaid, including interest for its provision.

- the obligations and debts of the original borrower are taken over by another person. The guarantee does not automatically pass to this new principal debtor.

- the principal debtor dies and the main debt passes as an inheritance to the guarantor.

- the contract provides that the guarantor can terminate it under certain conditions. An example would be if the financial and asset situation of the principal debtor has significantly deteriorated.

- the guarantee contract grants a right of revocation and the guarantor makes use of it.

- the guarantee was agreed from the outset for a specific period and this is fixed in the contract.

- the creditor waives his right.

Is a guarantee inherited?

"That has nothing to do with me? My father signed this guarantee, not me. And he has died." What sounds logical and understandable is unfortunately not so simple under the law. Whoever assumes that the guarantee ends with the death of the guarantor is mistaken. Guarantee contracts are inherited - with all agreements and obligations. If the contract allows it, an heir can terminate it. If the terms and obligations of the guarantee are unreasonable for the new guarantor, there is usually also the possibility to terminate the guarantee contract.

Guarantee banks

What is a guarantee bank?

Especially founders and future entrepreneurs know: getting a loan to start a business is extremely difficult. Many banks do not want to take the risk of failure that a business start-up inevitably involves. This is particularly true when there is no collateral. A business idea can be unique and exceptional; it does not help. Start-ups are not simply lent money. Yet sufficient start-up capital forms the basis for launching a business. Guarantee banks help in this case.

Young start-ups that can show hardly any collateral and little capital are given the opportunity by guarantee banks to bring their company to market.

Guarantee banks are organized privately. These development banks are supported by the state and aim to help the self-employed, freelancers and commercial enterprises with credit or equity financing. Usually each federal state has its own guarantee bank.

Lenders must secure themselves when providing loans. If collateral is missing, a guarantee bank helps. If it grants a guarantee, a bank regards this as full collateral. Guarantee banks in turn receive counter-guarantees from the federal government and the states. Every federal state has its own guarantee bank.

Guarantee with the guarantee bank

The loan security via the guarantee bank is applied for by the lending institution. First it is checked whether the founder’s project can be promoted at all. The business plan of the future company must be submitted for this.

How high is the guarantee at the guarantee bank?

Does the guarantee bank secure the entire requested loan amount? No. A guarantee bank limits liability for entrepreneurial risk to 70 to a maximum of 80 percent of the investment volume. The remaining 20 percent of the risk is borne by the lending institution itself.

When are guarantees from the guarantee bank possible?

The beginning is always the hardest. Therefore the guarantee bank supports founders. But what happens when a young company expands? When it wants to bring an exceptional business idea to market? Can the project be promoted? For this the guidelines under consideration of the EU aid principles (SME criteria) must be checked. If these are met? Excellent, in this case the guarantee bank can also step in as security. Guarantees can be applied for repeatedly until the maximum total amount of one million euros is reached. No more is possible. If the ideas and proposals are not eligible for support, the guarantee bank does not provide the loan guarantee. Is the company to be restructured? Or an existing loan to be refinanced? In both cases the guarantee bank does not act as a security provider.

Guarantee without bank (BoB)

Sometimes things do not gel with your own bank. The views differ too much. You can't come to an agreement and the loan is not granted.

Founders then look for alternative ways to obtain the required loan for the start-up. One option is to apply to a guarantee bank without involving the house bank. The program "Guarantee without bank" (Bürgschaft ohne Bank, BoB) was developed for this purpose. Here prospective entrepreneurs can contact one of the state guarantee banks directly, provided it participates in the BoB program. Most guarantee banks in Germany offer the program. If a guarantee bank is convinced that a start-up idea has a chance of success, it provides the corresponding security. With the guarantee commitment of the guarantee bank, founders find it easier to get a bank as a financing partner. This also applies to prospective lawyers, doctors, engineers, tax consultants or coaches and trainers, i.e. self-employed and freelancers.

Guarantee banks want to promote the SME sector. Therefore existing companies also have the opportunity to obtain a guarantee from the guarantee bank.

If they meet the following conditions:

- It is a small or medium-sized enterprise, freelancer or self-employed person.

- Existing debts are not higher than 500,000 euros.

- The company is profitable; revenue and earnings are sufficient.

- Positive equity is present.

- The credit requirement is between 50,000 and 500,000 euros.

The idea, its strategy and the planned measures are examined. If the start-up receives certification and the guarantee, it can present itself more confidently in negotiations with lenders due to this security. As a rule, companies then receive the desired loan approval relatively quickly.

Can the guarantee bank guarantee any type of loan or credit?

Whether loan guarantee or securing a subsidized loan, whether overdraft or leasing financing - the guarantee bank can provide a guarantee for this.

Alternatives to a guarantee

Are there alternatives to a guarantee?

In general lenders find other existing securities such as fixed-term deposit accounts, savings or real estate insufficient to grant a loan. As an alternative and for security only the guarantee may remain. On the other hand, a guarantee within the family and between spouses is always difficult. It is usually only approved if certain prerequisites are met. Are there other possibilities to obtain a loan?

It is conceivable to apply for a loan with two people. It does not matter what relationship the borrower has to the second person. Who with whom? Are the people married, friends or nothing of the sort? It is up to the applicant alone with whom they want to take out a joint loan.

If you take out a loan together with one or more other persons, you of course save costs. Often the loan interest rates are then lower. This applies particularly when the interest rate depends on creditworthiness and one of the borrowers has a very good ability to pay. Thus it is also possible for consumers with lower income to take out a loan without naming a guarantor.

What if one borrower suddenly cannot pay? Then the bank can access the other contractual partner and obtain the installment there. Both borrowers are therefore equally obliged to repay the debt. Each borrower is responsible for the other because the bank can turn to the other in the event of default.

The express guarantee

What is an express guarantee?

Sometimes it has to be quick. Very quick. And even quicker. Too many customers have not yet paid their invoices recently? But the claims keep running. Employees' salaries need to be paid. Sometimes you simply need money quickly. Often these are not even large amounts. And it is precisely these that banks sometimes find hardest to provide. Small and medium-sized enterprises know this. With the express guarantee the chance that lenders will grant a short-term loan increases.

Here, too, certain criteria must be met for the express guarantee to be possible:

- Company has existed for at least three years

- Positive equity in the presented annual financial statement

- Capacity to service debt is given

- Positive profit and loss account (at least 1 EUR profit)

- No negative information about the company at the house bank

Fast and simple approval

Simple conditions, high transparency and extremely fast approval - these are the differences between the express guarantee and the classic guarantee or the guarantee without bank. In addition, the guarantee is only rarely rejected. If the specified conditions are met, the guarantee bank checks the credit index at Creditreform. If the required documents are complete at the guarantee bank, it takes one to a maximum of three days for the guarantee bank's commitment for the express guarantee to be received by the applicant.

However, there are exceptions. Not every company and especially not from every industry can apply for the express guarantee.

Excluded, for example, are founders. Here the guarantee bank needs significantly more information that must be examined in more detail. Companies currently in financial difficulties will also not benefit from the express guarantee.

The intended use of the loan is decisive for the express guarantee. If a loan is to be used to restructure the company, to refinance existing loans or to finance losses, that is excluded from the outset. These purposes are generally excluded by guarantee banks. An exception applies if vehicles for a transport company (road transport) are to be purchased or leased. Companies in agriculture, fisheries and aquaculture do not receive an express guarantee.

Since the amounts for express guarantees are relatively limited compared to the classic guarantee, banks waive business plans and statements by associations or chambers. However, the managing shareholder is liable up to the amount of the loan. If there are several shareholders the liability is distributed accordingly. In addition, the guarantee bank requires a term life insurance policy covering the loan amount.

Advantages of the express guarantee

Anyone who wants to be competitive — and above all stay competitive — usually needs money. Sometimes quickly. Growth and innovation are decisive. For large companies this is no problem; for small and medium-sized enterprises it often is. The express guarantee helps existing companies, freelancers and the self-employed to obtain smaller loans more quickly. With a guarantee bank commitment, house banks more readily grant these companies a loan.

The express guarantee offers:

- transparent criteria

- quick approval (usually within 24 hours)

- online-based, standardized and automated processing

- waiver of business plans and expert statements from chambers and associations

- transfer to the classic house bank procedure if no approval is possible

Guarantees and insolvency

What happens if the principal debtor becomes insolvent?

Sometimes it happens faster than you think: too many unpaid invoices, too many obligations, too little turnover or income. To get out of the debt trap all that is often left is insolvency. Does this affect the principal debtor? After the onset of insolvency, debtor and guarantor are jointly and severally liable towards the creditor. Each person is therefore responsible for the entire loan amount.

Does the principal debtor slip into personal insolvency? The consumer insolvency procedure sets the rules here: the debtor is discharged of debts after six years. Claims that are not satisfied until then lapse. The guarantor, however, remains liable even after the six years. The creditor can also conclude an out-of-court settlement within the insolvency proceedings. Under certain conditions that are met, the loan agreement is terminated. In that case the guarantor is no longer responsible. A creditor cannot hold the guarantor accountable for the loss suffered.

What happens if the guarantor files for insolvency?

Can a creditor assert claims from the guarantee if the guarantor is insolvent? To what extent can he possibly obtain an amount from the insolvency proceedings?

Whether a creditor can still claim his money depends on whether the guarantor …

- is liable as a guarantor against default (Ausfallbürge),

- has signed an immediately enforceable guarantee,

- can raise the defense of prior enforcement (Einrede der Vorausklage).

As a guarantor against default he is not liable simultaneously with the principal debtor, but after him. The creditor must first address the principal debtor. Only then can he try to recover his money from the guarantor. This is, however, only possible up to the amount of the shortfall. The same applies if the guarantor can raise the defense of prior enforcement.

With the immediately enforceable guarantee, however, it is possible for the creditor to register his claims against the guarantor in the guarantor's insolvency. If the insolvent person is granted residual debt discharge? Then claims from the guarantee also lapse.